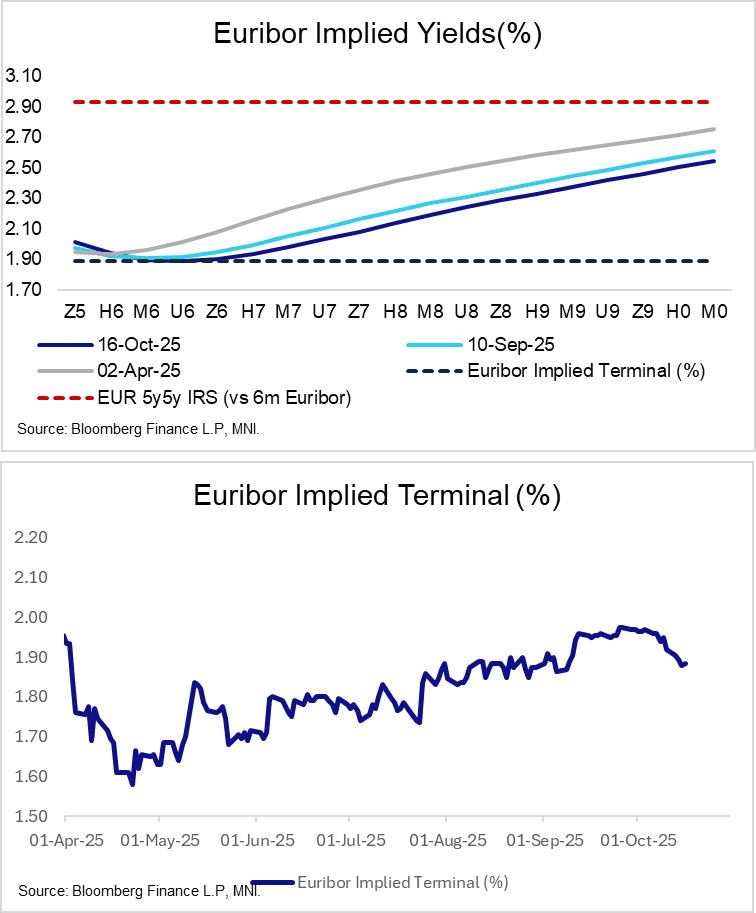

STIR: Euribor Implied Terminal May Struggle To Push Through 1.90% Without Data

The Euribor implied terminal rate may struggle to push meaningfully below 1.90% in the absence of fresh data catalysts. ECB speakers are unlikely to deviate materially from their prior stances, and near-term French political risks have eased from recent extremes with PM Lecornu likely to survive today’s no-confidence votes.

- The terminal rate is now indicated by the U6 contract (previously M6), currently at 1.89%.

- Across the strip, futures are little changed versus yesterday’s settlement levels.

- ECB-dated OIS price ~17.5bps of easing through September 2026. While risks still tilt towards another rate cut this cycle, Governing Council members will need to be convinced by incoming data to justify such a move. Focus remains on the flash PMI, GDP and inflation reports towards the end of this month.

- Today’s regional calendar sees Eurozone August merchandise trade data released. ECB’s Wunsch, Lane and Lagarde are scheduled to speak from the IMF/World Bank meetings in DC.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: EU Bank outright Put buyer

SX7E (17th Oct) 170p, bought for 0.15 in 10.7k.

CROSS ASSET: Bank stocks lead Europe lower

- The German Bund is testing through the initial resistance of 128.84, as mentioned by MNI, the sudden sell off in European Equities has been supportive.

- The Move in Equities is Bank led and especially Italian Banks, after earlier report from Bloomberg that Italy is working on a plan to raise €1.5bn from lenders in 2027.

- The Banking Index (SX7E) is down over 1% at 1.12%.

- Next level to watch in Bund is at the 129.13 gap.

STIR: Another ECB Cut Will Need To Be Motivated By Data

Marginal changes in EUR STIRs this morning, with ECB-dated OIS pricing ~10.5bps of easing through July 2026. For another ECB cut to be delivered, it will need to be motivated by incoming data. That leaves most regional focus on next week’s September flash PMIs and the September flash inflation round at the end of the month. In the meantime, spillover from this week’s central bank decisions will be eyed.

- Euribor futures are little changed through the blues, with light support stemming from the latest uptick in core EGBs.

- This morning, Kazaks provided a view that we think is consistent with the median Governing Council member. While he does not see a reason to lower rates at this stage, he is open to the idea of another cut if justified by the data. This contrasts with those on the more dovish end of the spectrum (e.g. Villeroy) and also hawks (e.g. Schnabel).

- Today’s regional calendar includes the German September ZEW survey and July Eurozone industrial production – these shouldn’t be market movers.

- ECB’s Escriva is scheduled at 0900BST.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Oct-25 | 1.919 | -0.7 |

| Dec-25 | 1.889 | -3.7 |

| Feb-26 | 1.875 | -5.1 |

| Mar-26 | 1.833 | -9.3 |

| Apr-26 | 1.827 | -9.9 |

| Jun-26 | 1.819 | -10.7 |

| Jul-26 | 1.820 | -10.6 |

| Sep-26 | 1.832 | -9.5 |

| Source: MNI/Bloomberg Finance L.P. | ||