MNI US MARKETS ANALYSIS - Trump Announcement in Focus

Highlights:

- Treasury curve modestly bear steeper ahead of 10y supply

- Markets look ahead to Trump announcement; topics could include Fed/BLS nominees, Russia sanctions, both or neither

- GBP stable despite UK facing tougher fiscal picture in Autumn

US TSYS: Modest Bear Steepening, 10Y Supply And Trump Deliberations In Focus

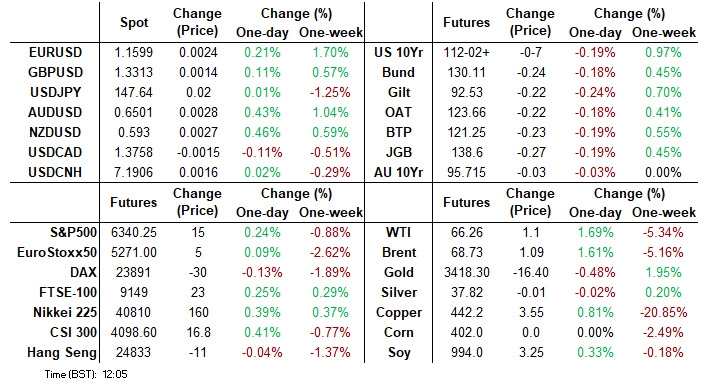

- Treasuries are cheaper and steeper with similar moves seen in EGBs. It’s a quiet docket ahead, with likely added attention on 10Y supply at 1300ET.

- WTI futures are +1.7% whilst S&P 500 futures are +0.2% having halved earlier gains (along with fixed income moving off lows).

- President Trump is set to make an announcement from the Oval Office at 1630ET according to Roll Call, topic unknown. He yesterday said he will decide on Fed Governor Kugler’s replacement by the end of the week, which could rule that out, but potential topics include a decision on Russian secondary sanctions or the appointee of new BLS commissioner.

- Cash yields are 0.6-3.2bp higher, with increases led by 30s.

- The steepening sees only a partial retracement of Mon/Tue flattening away from Friday’s post-payrolls steeps. 5s30s have seen the more pronounced moves, currently at 102.5bp (+2bp) having hit joint ytd highs of circa 108.5bps with Monday’s Asia open.

- TYU5 trades at 112-02+ (-07), close to session lows of 112-00 on another overnight with subdued cumulative volumes of 230k.

- It pulls back further from what is now latest resistance at 112-15+ from the Aug4/5 overnight high (after which lies 112-23, May 1 high)). Support is some way lower at 110-19+ (Jul 24 low).

- Data: MBA mortgage applications (0700ET)

- Fedspeak: Cook & Collins (1400ET), Daly (1610ET, incl text) – see STIR bullet

- Coupon issuance: US Tsy $42B 10Y Note auction - 91282CNT4 (1300ET). Last months’ 10Y saw a small 0.3bp stop along with mixed internals including bid-to-cover rising from 2.52 to 2.61 but indirect take retreating from 70.6% to 65.4%.

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

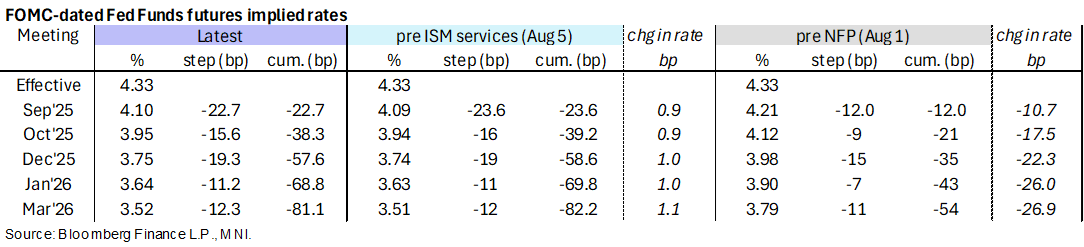

STIR: Slightly Less Dovish, More Post-FOMC (and NFP) Fedspeak Later

- Fed Funds implied rates are up to 1.5bp higher for meetings out to Mar 2026, hovering close to their highest since the Friday’s NFP and ISM mfg reports had been digested but still holding a strong dovish shift on net.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 38.5bp Oct, 57.5bp Dec, 69bp Jan and 81bp Mar.

- The SOFR implied terminal yield of 3.055% (SFRH7, +2.5bp) continues its slow rise off Monday’s lowest close since late April, but still broadly prices five cuts from current levels.

- Today sees a particularly thin data docket although there is a continuation of post-FOMC and NFP Fedspeak later on. Bostic and Hammack took a measured tone on Friday, Daly a little more dovish on Monday.

- 1400ET – Gov. Cook (permanent voter) and Collins (’25 voter) in a panel event (no text). We last heard from Cook back in early June when she warned the Fed must be open to all possibilities regarding rates including explicit mention of rate hikes. Collins pushed an “actively patient” approach to monetary policy as remaining appropriate when last speaking in mid-July.

- 1610ET – Daly (non-voter) speaks at Anchorage Economic Summit (text + Q&A). She told Reuters late Monday that she still sees two rate cuts this year as “an appropriate amount of recalibration”. “We of course could do fewer than two if inflation picks up and spills over or if the labor market springs back”. However, “I think the more likely thing is that we might have to do more than two...we also should be prepared in my judgment to do more if the labor market looks to be entering that period of weakness and we still haven’t seen spillovers to inflation”

- Trump yesterday on deliberations over Gov. Kugler’s board position: “I’ll be making that decision before the end of the week. We’ll either decide on one for permanence or the four-month period — the term. You know, there’s a term of about a number of months.”

US TSY FUTURES: Long Setting In WN Most Prominent In Tuesday's Twist Flattening

OI data points to a mix of net short setting (TU, FV & TY), long cover (UXY & US) and long setting (WN) as the curve twist flattened on Tuesday.

- The most meaningful DV01 equivalent adjustment came via the net long setting seen in WN futures.

| 05-Aug-25 | 04-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,560,934 | 4,547,259 | +13,675 | +502,420 |

FV | 7,016,171 | 6,991,294 | +24,877 | +1,063,492 |

TY | 5,095,136 | 5,075,175 | +19,961 | +1,318,823 |

UXY | 2,457,644 | 2,460,220 | -2,576 | -225,941 |

US | 1,746,314 | 1,749,121 | -2,807 | -393,710 |

WN | 1,977,746 | 1,955,238 | +22,508 | +4,126,392 |

|

| Total | +75,638 | +6,391,475 |

SOFR: Mix Of Net Short Setting & Long Cover Seen In Futures On Tuesday

OI data points to net short setting dominating in the front 11 contracts as SOFR futures ticked lower on Tuesday.

- Net long cover then came to the fore in the in 3 of the 5 contracts across SFRH8-H9.

| 05-Aug-25 | 04-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,234,845 | 1,229,935 | +4,910 | Whites | +55,484 |

SFRU5 | 1,272,724 | 1,269,936 | +2,788 | Reds | +30,310 |

SFRZ5 | 1,372,135 | 1,343,145 | +28,990 | Greens | +54,019 |

SFRH6 | 1,070,063 | 1,051,267 | +18,796 | Blues | -217 |

SFRM6 | 886,489 | 874,869 | +11,620 |

|

|

SFRU6 | 853,616 | 853,482 | +134 |

|

|

SFRZ6 | 952,570 | 947,636 | +4,934 |

|

|

SFRH7 | 723,610 | 709,988 | +13,622 |

|

|

SFRM7 | 778,933 | 733,863 | +45,070 |

|

|

SFRU7 | 576,162 | 571,992 | +4,170 |

|

|

SFRZ7 | 512,749 | 504,762 | +7,987 |

|

|

SFRH8 | 332,777 | 335,985 | -3,208 |

|

|

SFRM8 | 273,201 | 272,504 | +697 |

|

|

SFRU8 | 206,936 | 208,967 | -2,031 |

|

|

SFRZ8 | 215,554 | 212,056 | +3,498 |

|

|

SFRH9 | 150,083 | 152,464 | -2,381 |

|

|

SECURITY: Witkoff Meeting w/Putin Underway Ahead Of Trump Ceasefire Deadline 1/2

A meeting between US President Donald Trump’s Middle East envoy, Steve Witkoff, and Russian President Vladimir Putin is underway in Russia, per Interfax. The meeting comes ahead of Trump’s Friday deadline for Russia to reach a ceasefire with Ukraine or face new penalties. Measures could include fresh sanctions on Russia's economy and secondary tariffs on countries that buy Russian oil and gas.

- Speaking at the White House yesterday, Trump appeared to downplay the scope of potential secondary tariffs: "I never said a percentage, but we'll be doing quite a bit of that. We'll see what happens over the next fairly short period of time... We have a meeting with Russia tomorrow… We’ll make that determination at that time..."

- Trump said on July 15: "We're going to be doing secondary tariffs if we don't have a deal... It's very simple. And they'll be at 100%." The 100% number was itself a step down from a punitive 500% secondary tariff proposed by bipartisan legislation in the Senate. The Senate since parked the bill, giving Trump unilateral control over any sanctions.

- Ahead of today’s meeting, Bloomberg reported that the Kremlin is weighing up proposing an “air truce” as a concession to head off sanctions. While an air truce is unlikely to lead to a durable ceasefire, it could provide an off-ramp for Trump to claim a win without backing down from his threat (inviting more TACO accusations) or pursuing secondary tariffs that could derail delicate trade talks with China.

SECURITY: Witkoff Meeting w/Putin Underway Ahead Of Trump Ceasefire Deadline 2/2

Should Trump pursue secondary tariffs, they would likely fall primarily on India, with Trump saying yesterday he’d “very substantially” raise tariffs on Indian exports to the US over the next 24 hours to punish New Delhi for buying Russian oil.

- An air truce may be in the best interest of both parties. In July, Russia fired 6,443 drones and missiles into Ukraine, a new monthly record. However, Ukraine has also had success with a long-range strike strategy. President Volodymyr Zelenskyy touted on X this morning “the effectiveness of our long-range strikes on Russian military machine and war economy.”

- The Twelve-Day War between Iran and Israel revealed critical shortages in missile interceptor stocks that are likely mirrored in both the Russian and Ukrainian armouries. An air truce could offer a short-term reprieve for both Moscow and Kyiv to replenish stocks, while also providing space for additional technical meetings to lay the groundwork for a first wartime leader-level meeting, a request made by Zelenskyy on Aug 1.

- The Kremlin said yesterday that a Putin-Zelenskyy meeting could take place “after the necessary work is done at the expert level and the necessary distance has been covered.” A Kremlin spokesperson noted that this work “has not yet been done.”

- Trump has teed up a special “announcement” at the White House at 16:30 ET 21:30 BST. The announcement could relate to his decision on Russia sanctions or unrelated decisions on Fed/BLS nominees or the DOJ’s ‘Russiagate’ investigation.

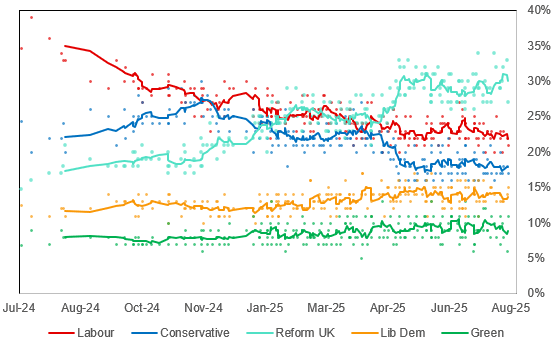

UK: Gov't Faces Stark Choice On Tax Hikes Amid Slumping Support

The government is walking an increasingly difficult political tightrope as it faces a bleak fiscal outlook while also attempting to shore up its public support. As noted earlier (see 'STIR: Under 50bp Of Cuts Priced Through Dec, NIESR Note Fiscal Issues', 07:44BST), the National Institute of Economic and Social Research (NIESR) think tank published a report on 6 August outlining the significant fiscal shortfall Chancellor of the Exchequer Rachel Reeves faces ahead of the autumn Budget. The NIESR exec summary notes: "The Government is not on track to meet its ‘stability rule’, with our forecast suggesting a current deficit of £41.2 billion in the fiscal year 2029-30. Substantial adjustments in the Autumn Budget will be needed if the Chancellor is to remain compliant with her fiscal rules."

- NIESR Deputy Director for Macroeconomics Stephen Millard told the BBC, "If [Reeves] wants to raise £40bn then I think one of the big taxes [VAT, employee National Insurance or income tax] is going to have to be raised. If she does that, then it will break the Labour promise about raising taxes on working people."

- Support for the governing centre-left Labour party has slumped since the July 2024 election (see chart below). The right-wing populist Reform UK of Nigel Farage has surged into first place in opinion polls, with its numbers (enough to potentially provide it a Commons majority in 2029) proving 'stickier' than many pundits anticipated.

- With Reform UK benefiting from significant public anger at Labour's handling of immigration and crime, breaking its manifesto promises on tax could further damage the gov'ts standing ahead of elections to the Scottish and Welsh parliaments and English local councils in 2026.

- Betting market data from Smarkets shows a 66.3% implied probability that PM Sir Keir Starmer is out of office by 2029, the year of the next general election. A poor set of results for Labour in 2026, engendered in part by tax hikes, could see Starmer's odds of political survival drop further. Deputy PM Angela Rayner, sitting further to the left of Starmer, is seen as the bookmakers' favourite to be the next Labour leader.

Chart 1. General Election Opinion Polling, % and 6-Poll Moving Average

Source: YouGov, More in Common, Opinium, Techne, Find Out Now, Freshwater Strategy, BMG, Survation, Lord Ashcroft Polling, Focaldata, JL Partners, Whitestone Insight, Deltapoll, Stonehaven, We Think, MNI

EUR: Volume Spike Tips EUR/USD Through Post-NFP High

EUR edges to the best levels of the day into the NY crossover, with a sizeable upturn in EUR futures volumes at 1107BST/0607ET the likely driver. No notable newsflow or headlines crossing to trigger the move, and cross-market prices also relatively subdued.

- Just shy of $200mln notional traded on the initial EUR rally - helping push EUR/USD spot now through the 1.1600 handle for a new weekly high. Break of resistance into the post-NFP high at 1.1597 also helping here - and spot now within range of a sizeable option expiry (€1.1bln) rolling off at 1.1600 today.

- This tips EUR/JPY to new daily highs - but progress above 171.85 is needed before the late July highs can come into play.

HONG KONG: HKMA Intervenes Against on Weak-Side of Band

"HKMA BUYS HK$ 8.439 BLN AS HONG KONG DOLLAR HITS WEAK END OF TRADING RANGE" - Reuters

- Extends the spell of intervention this week and will further reduce the aggregate balance (which is now less than half that seen at the year's peak in May). Persistent HKD pressure comes as the carry trade dynamics remain highly favourable: overnight and one-week HKD swap rates remain heavily supressed (0.27% and 0.28% respectively) which is limiting the advance in HIBOR (1m has failed to rise materially above 1%) and, in turn, keeping long USD/HKD a favourable carry trade.

OPTIONS: Expiries for Aug06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-10(E1.6bln), $1.1550-65(E1.4bln), $1.1600(E1.1bln

- USD/JPY: Y147.00($1.3bln), Y152.00($1.0bln)

- GBP/USD: $1.3250(Gbp650mln)

EQUITIES: Stock Futures Point to Higher Open Wednesday

- US Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. This puts price well clear of support at the 20-day EMA, at 6325.25, signalling scope for a deeper retracement.

- The trend condition in Eurostoxx 50 futures faltered Friday, with short-term weakness resulting in a break of the bear trigger. Having shown below 5194.00, the Jun 23 low, the April 30 hi/lo range at 5078-5138 becomes the area of downside interest.

COMMODITIES: Gold Consolidating at Higher Levels

- Gold benefited from the soft NFP print on Friday, returning prices toward the top-end of the recent range. This supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact.

- WTI futures fell for a fourth consecutive session into the Tuesday close, keeping S/T momentum pointed lower. Support to watch remains the 50-day EMA, at $65.48 - a level pierced yesterday. A clear break would expose $58.17, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 06/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 06/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 06/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 06/08/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 06/08/2025 | 1800/1400 | Boston Fed's Susan Collins | ||

| 06/08/2025 | 1800/1400 | Fed Governor Lisa Cook | ||

| 06/08/2025 | 1910/1510 | San Francisco Fed's Mary Daly | ||

| 07/08/2025 | 0130/1130 | ** | Trade Balance | |

| 07/08/2025 | 0600/0800 | ** | Trade Balance | |

| 07/08/2025 | 0600/0800 | ** | Industrial Production | |

| 07/08/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/08/2025 | 0645/0845 | * | Foreign Trade | |

| 07/08/2025 | 0700/0900 | ** | Unemployment | |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1130/1230 | BOE Press Conference | ||

| 07/08/2025 | - | *** | Trade | |

| 07/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 07/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 07/08/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 07/08/2025 | 1300/1400 | BOE Decision Maker Panel Data | ||

| 07/08/2025 | 1400/1000 | * | Ivey PMI | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 07/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 07/08/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 07/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 07/08/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 07/08/2025 | 1900/1500 | * | Consumer Credit | |

| 07/08/2025 | 1900/1500 | *** | Mexico Interest Rate |