SECURITY: Witkoff Meeting w/Putin Underway Ahead Of Trump Ceasefire Deadline 2/2

Aug-06 2025 09:10

Should Trump pursue secondary tariffs, they would likely fall primarily on India, with Trump saying yesterday he’d “very substantially” raise tariffs on Indian exports to the US over the next 24 hours to punish New Delhi for buying Russian oil.

- An air truce may be in the best interest of both parties. In July, Russia fired 6,443 drones and missiles into Ukraine, a new monthly record. However, Ukraine has also had success with a long-range strike strategy. President Volodymyr Zelenskyy touted on X this morning “the effectiveness of our long-range strikes on Russian military machine and war economy.”

- The Twelve-Day War between Iran and Israel revealed critical shortages in missile interceptor stocks that are likely mirrored in both the Russian and Ukrainian armouries. An air truce could offer a short-term reprieve for both Moscow and Kyiv to replenish stocks, while also providing space for additional technical meetings to lay the groundwork for a first wartime leader-level meeting, a request made by Zelenskyy on Aug 1.

- The Kremlin said yesterday that a Putin-Zelenskyy meeting could take place “after the necessary work is done at the expert level and the necessary distance has been covered.” A Kremlin spokesperson noted that this work “has not yet been done.”

- Trump has teed up a special “announcement” at the White House at 16:30 ET 21:30 BST. The announcement could relate to his decision on Russia sanctions or unrelated decisions on Fed/BLS nominees or the DOJ’s ‘Russiagate’ investigation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: USD Bounce Has Major Pairs Testing Key Levels

Jul-07 2025 09:05

- The USD's bounce Monday is providing some relief for the USD Index, which now sits 1% above last week's cycle lows to put the currency on a surer footing. As a result, the major pairs are seeing pressure toward the the post-NFP lows - with EUR/USD and GBP/USD challenging 1.1718 and 1.3586 respectively.

- Rates markets are endorsing USD gains here: the US curve is steeper as the global long-end continues to underperform. This backdrop, allied with any deterioration in trade relations between the US and the RoW remains a key market focus, particularly with the fluidity around Trump's approach to tariffs and the suite of reciprocal trade tariff deadlines looming over markets this summer.

- A correction lower through 1.3563 would be consequential for GBP/USD, and raise the likelihood of a test on the 50-dma support in the near-term. This level has held well and helped define the rally over the course of 2025 - crossing at 1.3477 today. In trend terms, we note that the 50-dma now trades with the largest % premium over the 200-dma since the bounce off lows in 2009. The premium currently sits at ~4.2% vs. the 2009 peak of ~8.2%, mid-Global Financial Crisis.

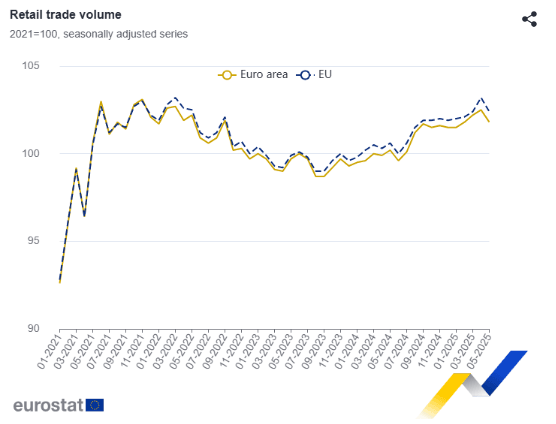

MNI: EUROZONE MAY RETAIL SALES -0.7% M/M, +1.8% Y/Y

Jul-07 2025 09:00

- MNI: EUROZONE MAY RETAIL SALES -0.7% M/M, +1.8% Y/Y

EUROZONE DATA: May Retails Sales Weak As Expected, Non-Food & Fuel Carry Y/Y

Jul-07 2025 09:00

Eurozone (real) retail sales were overall broadly in line with (weak) expectations in May on a sequential comparison, at -0.7% M/M (-0.6% M/M cons; +0.3% April, revised from +0.1%).

- Across sectors, all main categories fell: Food, drinks, tobacco -0.7% M/M, non-food products (except automotive fuel) -0.6%, automotive fuel -1.3% - neither of the categories has exhibited a clear directional trend YTD.

- Also across countries, May weakness appears quite broad-based, with Spain the strongest out of the "big 4" EZ countries at a mere 0.2% M/M.

- The overall Y/Y print was 1.8% in May, a bit firmer than consensus of 1.4% (2.7% Apr, revised from 2.3%). Across categories, previous trends prevail here: Non-food products and auto fuel tend to fare better than the food, drinks, tobacco category.

- Consumer confidence gives a rather weak outlook for retail sales in the Eurozone: "Consumer confidence remained broadly stable [on a, we would say, weak level of -14.8]. Although consumers were notably less pessimistic about the future general economic situation in their respective country, their intentions to make major purchases over the next 12 months dropped. Additionally, their perceptions of both their household’s past and expected financial situation deteriorated somewhat", the European Commission commented on the latest respective release.

- A June McKinsey study found that inflation remains consumers' main concern in the EU, although this has decreased compared with last year.