MNI US MARKETS ANALYSIS - ECB, US CPI Should Shape Session

Highlights:

- US CPI should shape the tone of Fed rate cut in September

- ECB decision watched carefully for views on neutral rates and domestic demand

- Treasuries rangebound, but yields net lower since PPI

US TSYS: Back To Little Changed Ahead Of CPI, Claims and 30Y Supply

- Treasuries have pared earlier mild losses to leave them near unchanged on the day in light volumes ahead of an important docket including CPI, jobless claims and 30Y supply.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Sep2025_50a5f503bd.pdf

- Yesterday's 10-year auction was clearly strong, including a 1.4bp trade through, but not a blowout according to our Relative Strength Indicator metric. Reaction to it was contained whilst CPI looms large but the 30Y auction could be a better test of duration demand.

- Cash yields are between 0-0.5bp lower on the day.

- TYZ5 trades at 113-15+ (-03) with narrow ranges of 113-12 to 113-16 overnight, on very thin cumulative volumes of 185k.

- A bull cycle remains in play, with resistance at 113-21+ (Sep 5 high) before 113-26+ (Fibo proj). Support meanwhile is seen at 112-28+ (Sep 5 low) before 112-18 (20-day EMA).

- Data: CPI Aug (0830ET), Jobless claims (0830ET), Household chg in net worth Q2 (1200ET), Federal budget balance Aug (1400ET)

- Coupon issuance: US Tsy $22B 30Y Bond auction re-open - 912810UM8 (1300ET)

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1130ET)

- Politics: Trump attends September 11th Observance Event (0845ET, with travel pool), Trump departs the White House en route to NY (1600ET, open press)

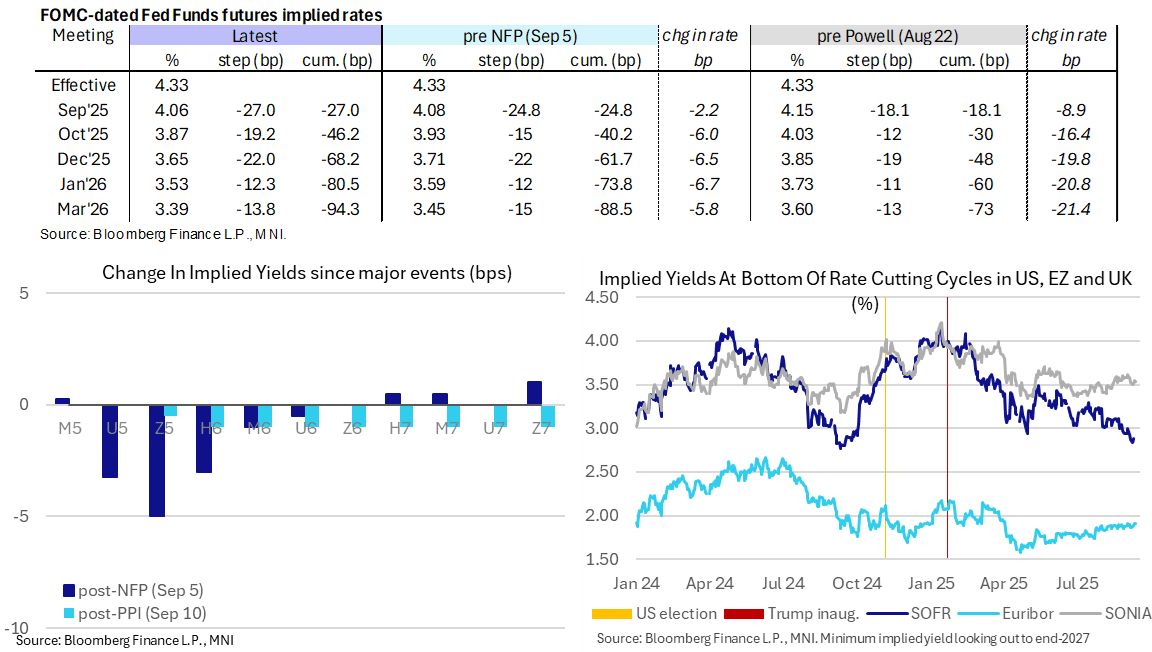

STIR: A Little Off Recent Dovish Extremes Ahead Of US CPI

- Fed Funds implied rates hold the mid-week tilt off dovish extremes seen following a weak NFP report but are still firmly dovish ahead of today’s CPI report.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Sep2025_50a5f503bd.pdf

- Cumulative cuts from 4.33% effective: 27bp for Sep 17, 46bp Oct, 68bp Dec, 80.5bp Jan and 94.5bp Mar.

- SOFR futures are broadly 1.5 ticks lower overnight in contracts out to late 2027.

- The SOFR implied terminal yield of 2.89% is off Monday’s 2.84%, which marked one of the lowest closes of the cycle, but still points to ~145bp of cuts ahead.

- We estimated the median analyst estimates core CPI at 0.32% M/M and don’t think there will have been a notable change in this figure since yesterday’s PPI data.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

US TSY FUTURES: Net Long Setting Dominated On Wednesday

OI data points to a mixture of net long setting (TU, FV, TY, UXY & WN) and short cover (US) during Wednesday’s uptick in futures, with the former dominating in net DV01 terms.

| 10-Sep-25 | 09-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,485,007 | 4,484,877 | +130 | +4,547 |

FV | 6,841,858 | 6,789,454 | +52,404 | +2,339,054 |

TY | 5,288,290 | 5,264,095 | +24,195 | +1,601,613 |

UXY | 2,374,168 | 2,365,244 | +8,924 | +791,024 |

US | 1,818,326 | 1,828,101 | -9,775 | -1,399,915 |

WN | 2,026,591 | 2,021,086 | +5,505 | +1,034,134 |

|

| Total | +81,383 | +4,370,457 |

SOFR: Net Long Setting Most Prominent In Futures On Wednesday

OI data points to net long setting being more prominent than instances of net short cover during Wednesday’s uptick in SOFR futures, with the whites and greens seeing the largest swings in net pack terms (positioning was essentially flat in the reds in net pack terms).

| 10-Sep-25 | 09-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,206,059 | 1,225,455 | -19,396 | Whites | +56,496 |

SFRU5 | 1,437,840 | 1,419,962 | +17,878 | Reds | -416 |

SFRZ5 | 1,669,251 | 1,631,123 | +38,128 | Greens | +44,838 |

SFRH6 | 1,208,359 | 1,188,473 | +19,886 | Blues | +5,535 |

SFRM6 | 1,003,677 | 1,002,607 | +1,070 |

|

|

SFRU6 | 877,881 | 882,951 | -5,070 |

|

|

SFRZ6 | 1,008,248 | 1,003,442 | +4,806 |

|

|

SFRH7 | 704,328 | 705,550 | -1,222 |

|

|

SFRM7 | 841,769 | 838,404 | +3,365 |

|

|

SFRU7 | 682,400 | 669,554 | +12,846 |

|

|

SFRZ7 | 669,270 | 647,243 | +22,027 |

|

|

SFRH8 | 447,244 | 440,644 | +6,600 |

|

|

SFRM8 | 359,017 | 356,851 | +2,166 |

|

|

SFRU8 | 257,772 | 258,032 | -260 |

|

|

SFRZ8 | 261,554 | 266,534 | -4,980 |

|

|

SFRH9 | 184,657 | 176,048 | +8,609 |

|

|

EUROPE ISSUANCE UPDATE:

UK gilt tender results

- 05:00 ET tender: GBP1bln of the 4.25% Jun-32 Gilt. Avg yield 4.206% (bid-to-cover 3.72x, tail 0.2bp).

- Decent short 7-year tender. No huge wider impact.

- 06:30 ET tender: GBP1.25bln of the 0.50% Jan-29 Gilt. Avg yield 3.841% (bid-to-cover 3.86x, tail 0.1bp).

- Another decent tender with the LAP (lowest accepted price) above the pre-auction mid-price with a tight tail of 0.1bp and bid-to-cover of 3.86x.

- Again, no real wider impact on gilt futures here.

Ireland auction results:

- E1bln of the 2.60% Oct-34 IGB. Avg yield 2.876% (bid-to-cover 1.58x).

- E500mln of the 3.00% Oct-43 Green IGB. Avg yield 3.428% (bid-to-cover 1.88x).

Italy auction results:

- E3.25bln of the 2.35% Jan-29 BTP. Avg yield 2.44% (bid-to-cover 1.59x).

- E1.5bln of the 4.00% Nov-30 BTP. Avg yield 2.76% (bid-to-cover 1.80x).

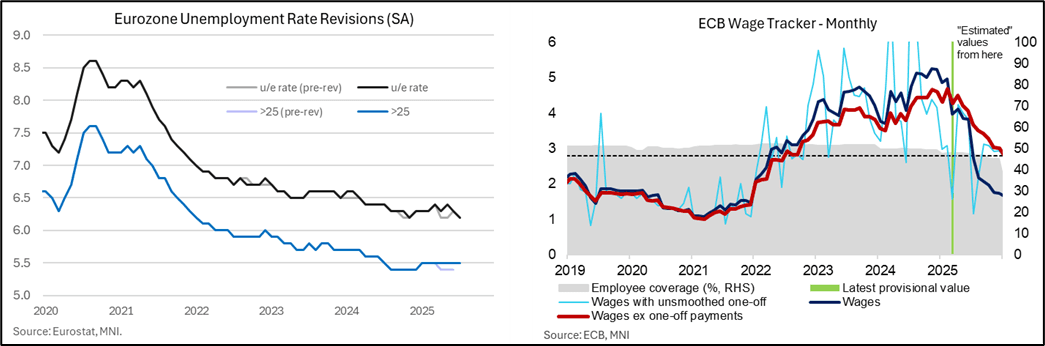

ECB: Macro Since Last ECB: Labour - U/E Rate At Series Lows After More Revisions

- The Eurozone unemployment rate printed at 6.2% in July as expected, a joint series low, but revisions have again altered recent trends. The data have quite often been revised and June saw a fairly typical 0.1pp upward revision to 6.3%, although the +0.2pp to 6.4% in May was more surprising.

- It leaves a trend of recent improvement but with question marks over the data. What had been seen as three months at joint cycle lows of 6.2% through Apr-Jun, tying with 6.2% in Oct-Nov 2024, Eurostat now estimate a latest pattern of 6.3% in Apr, 6.4% in May, 6.3% in Jun and 6.2% in July, tying with 6.2% only in Nov 2024.

- ECB’s Lagarde has pointed to these at-the-time historically low unemployment rates when citing the health of the labour market in recent meetings. Outright employment growth remains subdued however, with just 0.1% Q/Q and 0.6% Y/Y in Q2.

- As for inflationary pressures stemming from the labour market, Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB's 2.9% projection made in June, seemingly driven by the smaller-than-expected deceleration in total compensation per employee growth (3.9% Y/Y vs 4.0% prior, 3.4% ECB).

- While a declaration in ULC growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- ULC growth may have moderated at a steadier pace than the ECB forecast but its forward looking wage tracker released earlier in the inter-meeting process points to a continued decline in negotiated wage growth. Now with estimates out to 1Q26, it eyes wage growth excluding one-off payments at 2.6% Y/Y in 1Q26 after 3.1% in 4Q25. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

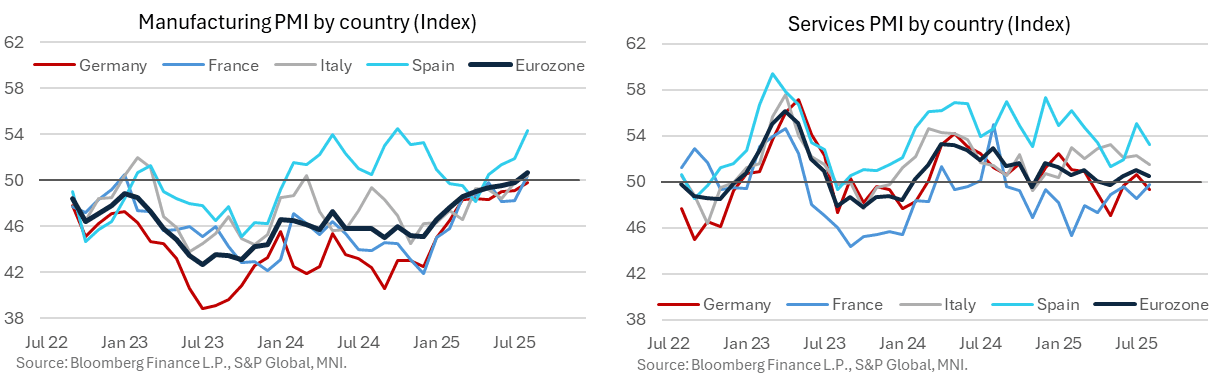

ECB: Macro Since Last ECB: Growth - Mfg PMIs Finally In Positive Territory [2/2]

- As for soft indicators, the August PMIs were mixed by sector relative to July with manufacturing continuing to improve but services unwinding the previous month’s improvement.

- It saw the composite PMI increase 0.1pt to 51.0 for its joint highest since May 2024. Within that, the manufacturing survey increased for an eighth consecutive month to a 38-month high, even if that’s only just back into expansionary territory at 50.7.

- Nevertheless, that’s still showing some relative resilience compared to potential scenarios envisaged under aggressive US trade policy. Press release: “While the pace of expansion ticked up to a one-year high, it remained sluggish overall. The service sector held back overall growth, with output rising only marginally. Nevertheless, for the first time since May 2024, private sector firms reported greater volumes of incoming new work and employment growth was its quickest in 14 months”.

FOREX: USD Firmer into CPI, EUR Rangebound Pre-ECB

- The USD trades frirner against most others in G10 Thursday, helping keep most major pairs pinned to the post-PPI lows. GBP/USD is softer, putting the rate through yesterday's 1.3513 low, exposing 1.3468 - the 50-day EMA - as interim support. Newsflow has been few and far between after a busy start to the session Wednesday - with rumbling geopolitical risk still a fringe concern for now.

- JPY is the session's underperformer. The confirmation of Sanae Takaichi as in the running to replace Ishiba as LDP party head helped usher in some JPY weakness. Her outspoken pro-easing views have worked against the currency as they did during previous leadership races, keeping USD/JPY pinned higher toward the week's best levels. Resistance in the pair crosses at 148.06 initially, and into 148.47.

- The ECB rate decision takes focus going forward, at which markets expect no change in the policy rate set, with focus instead on the press conference with ECB's Lagarde. Her communication on the board's views of the neutral rate will be key - and in particular any insight into the strength of Eurozone domestic demand - which could prove decisive in any future decision to push rates into expansionary territory.

- Outside of the ECB, US CPI will be carefully watched. Into the print, overnight USD vols are generally contained - meaning markets see little chance of a market-moving print beyond what we saw in the reaction to soft PPI yesterday. Consensus looks for CPI to pickup on a headline Y/Y basis to 2.9%, but holding steady for the ex-food and energy metric.

ZAR: Market Scratching Head Over ZAR funding, as Curve Hits New Low

No let-up in the softness of the front-end of the ZAR swaps curve, meaning funding is falling again: one-week rates have dropped to new lows of 6.1 points, while overnight rates have dropped to 5.2 points, the lowest in over two years.

- There remains no clear fundamental driver for the soft demand here, although market speculation around coupon payments from local bonds, one-way market positioning and cash market mismatches are doing the rounds - but as is often the case in this corner of the market there's very little indication on the sustainability of such a pull lower in funding.

- The market mechanics here are very different to the other liquidity episode in EM FX we had this year in Hong Kong - in which HKMA intervention and a more isolated market exerted a greater influence - which adds to the uncertainty over what could be the catalyst for a recovery in short-end rates for ZAR.

- Sell-side reiterated their preference for ZAR (and HUF) longs in August on a carry basis. Goldman Sachs wrote just a few weeks ago that ZAR is among their preferred carry longs, and is among the most undervalued relative to peers, and set to benefit from forecasted CNY strength.

GLOBAL: MNI Tech Trend Monitor - Highlighting Key Longer-Term Trends:

https://emedia.marketnews.com/marketnewsintl/MNITechTrendMonitor.pdf

We introduce the MNI Tech Trend Monitor - This document highlights a selection of key longer-term trends that we have identified in markets that could be reaching inflection points, trend reversals/extensions or technically significant levels.

Covering:

- UK Gilt 10y Yield

- UK Gilt 30y Yield

- ICE USD Index

- Europe Banking Stock Index (SX7E)

COMMODITIES: Short-Term Gains for WTI Futures Considered Corrective

- The trend condition in WTI futures is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle and continues to trade closer to its recent highs. The yellow metal has traded to a fresh all-time high again this week. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3474.7, the 20-day EMA.

EQUITIES: Bull Cycle in E-Mini S&P Remains Intact, Sights on $6600 Handle Next

- A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5368.81, the 50-day EMA. A clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development. A stronger reversal would open 5445.00, the Aug 26 high.

- A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high on Wednesday, breaching the Sep 5 high of 6541.75. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on the 6600.00 handle next. Initial support to watch is 6469.93, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 11/09/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 11/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 11/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 11/09/2025 | 1230/0830 | * | Household debt-to-income | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1245/1445 | ECB Press Conference | ||

| 11/09/2025 | 1415/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 11/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 11/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/09/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 11/09/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/09/2025 | 0430/1330 | ** | Industrial Production | |

| 12/09/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 12/09/2025 | 0600/0700 | ** | Trade Balance | |

| 12/09/2025 | 0600/0700 | ** | Index of Services | |

| 12/09/2025 | 0600/0700 | ** | Index of Production | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0645/0845 | *** | HICP (f) | |

| 12/09/2025 | 0700/0900 | *** | HICP (f) | |

| 12/09/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/09/2025 | 0900/1100 | Labour Market Quarterly Statistics | ||

| 12/09/2025 | - | *** | Money Supply | |

| 12/09/2025 | - | *** | New Loans | |

| 12/09/2025 | - | *** | Social Financing | |

| 12/09/2025 | 1230/0830 | * | Building Permits | |

| 12/09/2025 | 1400/1000 | * | Services Revenues | |

| 12/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 12/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 12/09/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |