ECB: Macro Since Last ECB: Labour - U/E Rate At Series Lows After More Revisions

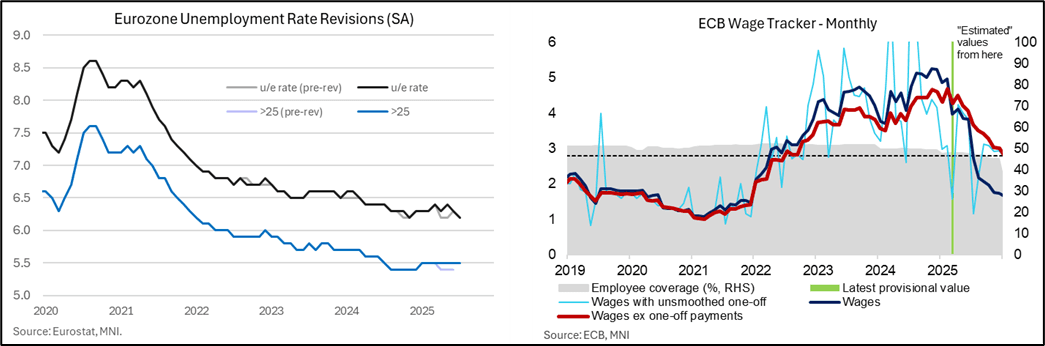

- The Eurozone unemployment rate printed at 6.2% in July as expected, a joint series low, but revisions have again altered recent trends. The data have quite often been revised and June saw a fairly typical 0.1pp upward revision to 6.3%, although the +0.2pp to 6.4% in May was more surprising.

- It leaves a trend of recent improvement but with question marks over the data. What had been seen as three months at joint cycle lows of 6.2% through Apr-Jun, tying with 6.2% in Oct-Nov 2024, Eurostat now estimate a latest pattern of 6.3% in Apr, 6.4% in May, 6.3% in Jun and 6.2% in July, tying with 6.2% only in Nov 2024.

- ECB’s Lagarde has pointed to these at-the-time historically low unemployment rates when citing the health of the labour market in recent meetings. Outright employment growth remains subdued however, with just 0.1% Q/Q and 0.6% Y/Y in Q2.

- As for inflationary pressures stemming from the labour market, Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB's 2.9% projection made in June, seemingly driven by the smaller-than-expected deceleration in total compensation per employee growth (3.9% Y/Y vs 4.0% prior, 3.4% ECB).

- While a declaration in ULC growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- ULC growth may have moderated at a steadier pace than the ECB forecast but its forward looking wage tracker released earlier in the inter-meeting process points to a continued decline in negotiated wage growth. Now with estimates out to 1Q26, it eyes wage growth excluding one-off payments at 2.6% Y/Y in 1Q26 after 3.1% in 4Q25. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Returns Lower, But Support Out of Reach

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8781 2.236 pro of the Mar 3 - 11 - 28 price swing

- RES 1: 0.8735/8769 High Aug 3 / High Jul 27 and the bull trigger

- PRICE: 0.8652 @ 15:29 BST Aug 11

- SUP 1: 0.8611 Low Jul 31

- SUP 2: 0.8597 50-day EMA

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8508 Low Jun 27

EUR/GBP corrected lower Thursday on the BoE rate decision, which sent prices through the weekly low. Despite the intraday weakness, support to watch remains out of reach for now at the 0.8611 50-day EMA. A clear break of it would strengthen a bear threat. More broadly, the trend set-up is bullish. Moving average studies remain in a bull-mode position highlighting a clear uptrend. Key resistance and the bull trigger is at 0.8769, the Jul 27 high.

OPTIONS: Limited Trade To Open Week, With Sonia Upside Faded Pre-Labour Data

Monday's Europe bond/rate options flow included:

- SFIH6 96.70 calls 3.5K given at 5

US OUTLOOK/OPINION: Analyst Expectations For Sequential Drivers In July CPI

Core CPI sequential drivers in July are expected to come from used cars increasing modestly after a weak run plus travel-related services with lodging away from home pausing after declining and airfares increasing after broadly pausing.

- Lodging away from home (+ve): Seen broadly unchanged on the month after a heavy -2.9% M/M in June that subtracted -0.05pps from core CPI.

- Used cars (+ve): There’s a reasonable range of estimates for used car prices in July, from -0.5% to +0.7% but they all are stronger than the -0.7 M/M seen in June. The average estimate is 0.24% M/M after four months averaging -0.6% M/M.

- Airfares* (+ve): Seen rising 1.5% M/M after -0.1% in June following a period of prolonged, large declines with an average -3.7% M/M through Feb-May. The range of views of -0.4% to 2.5% is one of the narrower in recent months.

- Apparel (neutral to small +ve): Median of 0.5%/average 0.44% having accelerated to 0.43% M/M in June from a surprisingly soft -0.4% M/M in May.

- Vehicle insurance* (neutral to small +ve): Once again only three estimates this month with a decent range of -0.1% to 0.6% M/M. The average of 0.2% M/M would be a slight acceleration from the 0.1% in June but it’s a category that can swing from month to month with a sizeable 3.5% weight in core CPI.

- Rents (neutral): Owners’ equivalent rent (OER) seen dipping to an average 0.28% (range 0.25-0.30) after 0.30% in June, but with primary rents firming to an average 0.26% (range 0.22-0.34) after 0.23%.

- Non-core: Food (small -ve): Food price inflation is seen easing to 0.25% M/M in July after 0.33% M/M. Food away from home has continued a robust run recently, with 0.40% M/M in June and a 1H25 average of 0.36% (feeding into core PCE but not CPI). Food at home meanwhile has seen two months averaging 0.27%.

- Energy (-ve): Energy prices are seen falling circa -0.6% M/M after a 0.95% increase in May, driven by a more than 2% M/M decline in seasonally adjusted gasoline prices.