US TSYS: Back To Little Changed Ahead Of CPI, Claims and 30Y Supply

Sep-11 10:46

- Treasuries have pared earlier mild losses to leave them near unchanged on the day in light volumes ahead of an important docket including CPI, jobless claims and 30Y supply.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Sep2025_50a5f503bd.pdf

- Yesterday's 10-year auction was clearly strong, including a 1.4bp trade through, but not a blowout according to our Relative Strength Indicator metric. Reaction to it was contained whilst CPI looms large but the 30Y auction could be a better test of duration demand.

- Cash yields are between 0-0.5bp lower on the day.

- TYZ5 trades at 113-15+ (-03) with narrow ranges of 113-12 to 113-16 overnight, on very thin cumulative volumes of 185k.

- A bull cycle remains in play, with resistance at 113-21+ (Sep 5 high) before 113-26+ (Fibo proj). Support meanwhile is seen at 112-28+ (Sep 5 low) before 112-18 (20-day EMA).

- Data: CPI Aug (0830ET), Jobless claims (0830ET), Household chg in net worth Q2 (1200ET), Federal budget balance Aug (1400ET)

- Coupon issuance: US Tsy $22B 30Y Bond auction re-open - 912810UM8 (1300ET)

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1130ET)

- Politics: Trump attends September 11th Observance Event (0845ET, with travel pool), Trump departs the White House en route to NY (1600ET, open press)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Aug12 NY cut 1000ET (Source DTCC)

Aug-12 10:45

- EUR/USD: $1.1500(E1.5bln), $1.1535-50(E1.2bln), $1.1650(E1.1bln)

- USD/JPY: Y147.30-50($1.6bln)

- AUD/USD: $0.6560-75(A$1.5bln)

- USD/CAD: C$1.3785($664mln)

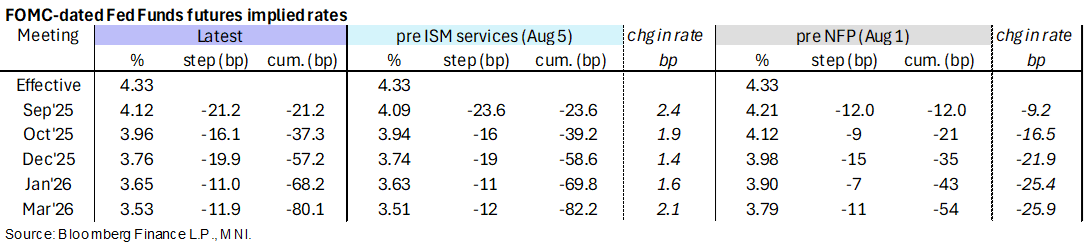

STIR: 21bp Fed Cut Seen Next Month Ahead Of CPI, Fedspeak To Follow

Aug-12 10:39

- Fed Funds implied rates have nudged a little higher for September (21bp cut priced, close to least since the Aug 1 NFP report) but are otherwise unchanged on the day ahead of CPI.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Aug2025_2fe4cdf4a1.pdf

- Cumulative cuts from 4.33% effective: 21bp Sep, 37.5bp Oct, 57bp Dec, 68bp Jan and 80.5bp Mar.

- The SOFR implied yield of 3.12% (SFRH7) is 1.5bp higher on the day having last closed higher prior to the July payrolls report on Aug 1.

- Today’s Fedspeak comes after US CPI:

- 1000ET – Barkin (non-voter) speaks at Health Management Academy (text + Q&A – no livestream). He last spoke on Jul 15, noting the most recent inflation data revealed some growing price pressures, and that more were on the way, with suppliers trying to pass on cost pressures to consumers who may not be able to absorb more price increases.

- 1030ET – Schmid (’25 voter, hawk) speaks on mon pol and economic outlook (text + Q&A). Previously one of the most hawkish members on the FOMC, he last spoke on Jun 25 saying he was watching data for signs of broad-based price increases. He also wanted to replace core inflation with a gauge that includes food.

LOOK AHEAD: July CPI Report and Fedspeak

Aug-12 10:30

US Data/Speaker Calendar (prior, estimate). All times ET

- 08/12 0830 CPI MoM (0.3%, 0.2%), Core CPI MoM (0.2%, 0.3%)

- 08/12 0830 CPI YoY (2.7%, 2.8%), Core CPI YoY (2.9%, 3.0%)

- 08/12 0830 Real av earnings YoY (1.0%, --)

- 08/12 1000 Barkin on economy (text + Q&A)

- 08/12 1030 Schmid on mon pol and economy (text + Q&A)

- 08/12 1130 US Tsy to sell $85B 6-W bills

- 08/12 1300 White House Press Sec. Leavitt Briefing

- 08/12 1400 Federal budget balance ($27.0b, -$239.2b)

- Source: Bloomberg Finance L.P., Roll Call, MNI