STIR: A Little Off Recent Dovish Extremes Ahead Of US CPI

Sep-11 10:19

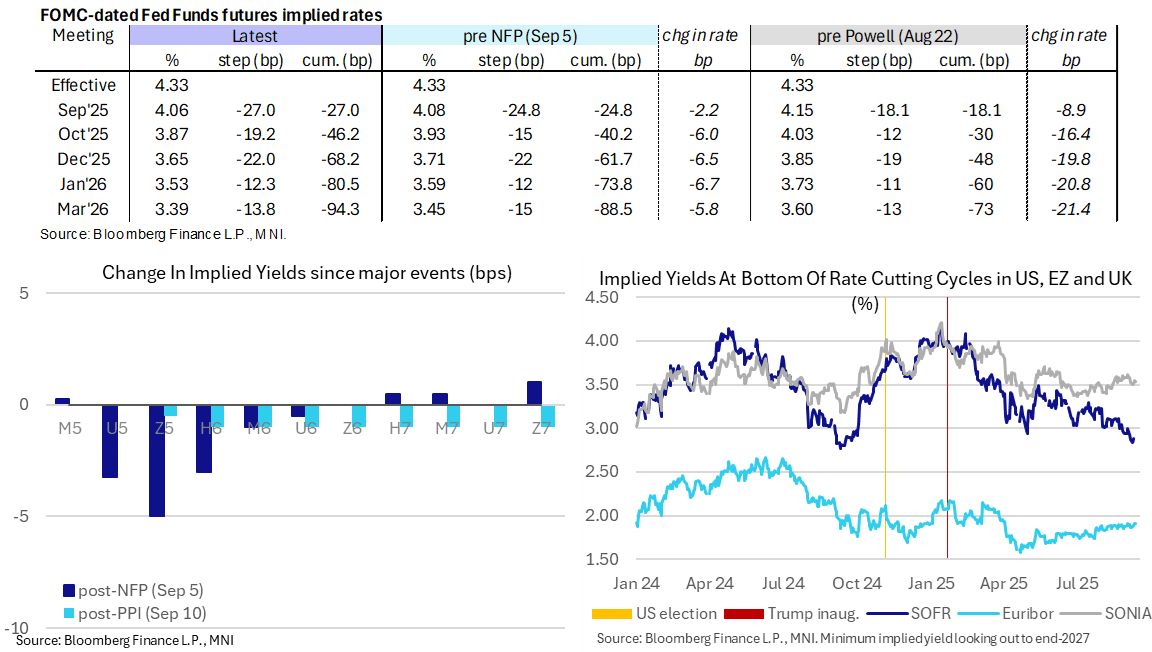

- Fed Funds implied rates hold the mid-week tilt off dovish extremes seen following a weak NFP report but are still firmly dovish ahead of today’s CPI report.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Sep2025_50a5f503bd.pdf

- Cumulative cuts from 4.33% effective: 27bp for Sep 17, 46bp Oct, 68bp Dec, 80.5bp Jan and 94.5bp Mar.

- SOFR futures are broadly 1.5 ticks lower overnight in contracts out to late 2027.

- The SOFR implied terminal yield of 2.89% is off Monday’s 2.84%, which marked one of the lowest closes of the cycle, but still points to ~145bp of cuts ahead.

- We estimated the median analyst estimates core CPI at 0.32% M/M and don’t think there will have been a notable change in this figure since yesterday’s PPI data.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Bank large Call Option trade

Aug-12 10:19

SX7E (19th Dec) 230c, bought for 11.95 in 17.6k.

EQUITIES: The EU Tech Index is through the August low

Aug-12 10:15

- The Tech index (SX8P) is the worst performer, down 1.8%, and is now through the August low, but not much spillovers into the US Nasdaq.

- As mentioned on the European Open, while President Trump announced further delay in Tariffs against China for another 90 days, earlier headline that China was urging companies to avoid NVIDIA H20 Chips, is helping keep some pressure in Tech.

- Next support in SX8P comes at 777.00.

UK DATA: MNI UK Labour Market Review: August 2025 Release

Aug-12 10:07

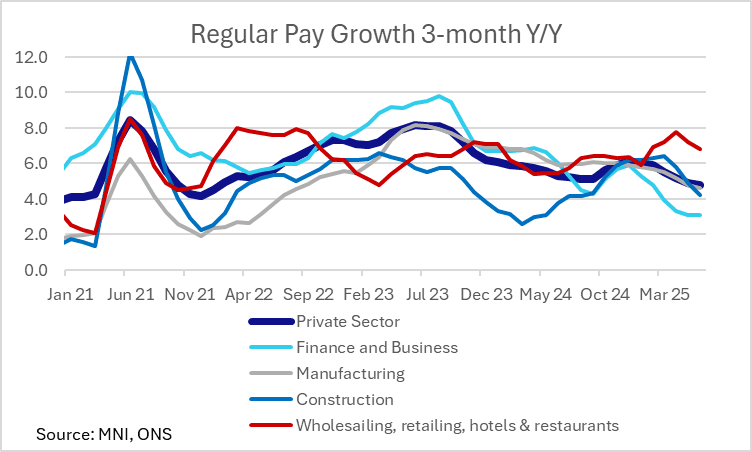

- The August UK labour market release was on balance stronger-than-expected, with 3m/3m employment growth surprising to the upside and the unemployment rate holding steady despite some risks of a one tenth increase.

- However, private sector regular pay data remains consistent with the idea that wage growth is slowing. Meanwhile, data such as vacancies, RTI-PAY payrolls and other labour market metrics/surveys point to more subdued developments than the headline LFS figures suggest.

- We have argued that a continually softening labour market is a necessity for another quarterly cut in November. The August release was worth a modest hawkish reaction in BOE implied pricing, but there’s still far too much data (on both inflation and the labour market) to come before excluding a November cut. OIS markets currently price ~11bps of easing through that meeting.