MNI EUROPEAN OPEN: US-China Officials To Meet Next Week

EXECUTIVE SUMMARY

- BULLARD INTERVIEWED BY BESSENT FOR FED CHAIR JOB - MNI

- LAGARDE DECLARES DISINFLATION OVER - MNI ECB WATCH

- BESSENT, CHINESE VICE PREMIER TO MEET IN MADRID NEXT WEEK ON TRADE, TIKTOK - RTRS

- US, JAPAN AGREE ON CLOSE CONTACT ON FX, POLICY - MNI BRIEF

- BOJ SEPT TANKAN TO SHOW KEY SENTIMENT RISES - MNI

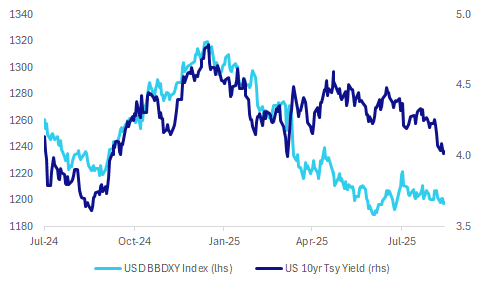

Fig 1: USD BBDXY & US 10yr Tsy Trends

Source: Bloomberg Finance L.P/MNI

UK

TECH (BBG): “ The leaders of OpenAI and Nvidia Corp. plan to pledge support for billions of dollars in UK data center investments when they head to the country next week at the same time as President Donald Trump, according to people with knowledge of the matter.”

EU

ECB (MNI ECB WATCH): The European Central Bank as expected held interest rate for a second consecutive meeting at 2% on Thursday, with President Christine Lagarde saying that the disinflationary process is now over and that risks to economic growth are more balanced.

ECB (BBG): "There’s currently no need for the European Central Bank to lower interest rates further to deliver stable inflation, according to Governing Council member Christodoulos Patsalides."

ECB (MNI INTERVIEW): The ECB should do nothing to ease the rise in French bond yields even if the market situation worsens further, the ECB’s former director general of market operations Francesco Papadia told MNI.

FRANCE (MNI BRIEF): Speaking at the ECB's latest post-policy decision press conference, Lagarde said "I’m not commenting on any particular country, but suffice to say we always monitor market developments and euro area sovereign bonds are orderly and are functioning smoothly with liquidity.”

RUSSIA (BBG): "President Donald Trump said incursions by Russian drones into Polish airspace could have been a “mistake,” but also expressed his frustration with an incident that has alarmed Warsaw and other NATO allies."

US

FED (MNI): Federal Reserve Bank of St. Louis President James Bullard told MNI he was interviewed for the position of Fed chair Wednesday, and made the case to Treasury Secretary Scott Bessent that his deep experience serving on the FOMC for 15 years has prepared him well to lead the central bank

FED (MNI INTERVIEW): The Federal Reserve is on track to lower interest rates by a full percentage point over the next six months, starting with three 25 basis point cuts at each of this year's remaining meetings, as tariff continue to have only muted effects on inflation and a fairly static labor market persists, former St. Louis Fed President James Bullard and a contender to become the next Fed chair, told MNI.

DATA (MNI BRIEF): U.S. CPI inflation picked up in August as Wall Street expected, while initial claims for unemployment benefits jumped to their highest since 2021 for the week ended Saturday, adding to concerns of stagflation. Futures traders are pricing in 28 bps of cuts this month and 76 bps through year end. The FOMC is expected to deliver a quarter-point rate cut next week.

US/CHINA (WAPO): “A rush of high-level diplomacy between United States and Chinese officials this week has stoked expectations that President Donald Trump will meet Chinese leader Xi Jinping as soon as next month, amid festering tensions over trade and defense.”

US/CHINA (RTRS): “U.S. Treasury Secretary Scott Bessent plans to meet with Chinese Vice Premier He Lifeng and other senior officials next week in Madrid to continue their discussions on trade, economic and national security issues, the Treasury said on Thursday.”

OTHER

JAPAN (MNI BRIEF): Japan’s Ministry of Finance and the U.S. Treasury said Friday they will continue close consultations on macroeconomic and foreign exchange issues, according to a joint statement released by the MOF.

JAPAN (MNI): Economists predict the Bank of Japan’s September Tankan survey will show a modest improvement in benchmark business sentiment from three months ago, with capital investment plans by major firms for fiscal 2025 likely to remain solid.

CANADA (MNI BRIEF): Canadian Prime Minister Mark Carney on Thursday left an oil pipeline off his list of projects to be fast-tracked for final approval over the next two years, at a time when its political backers in Alberta have failed to find a private investor to build one.

CANADA (MNI INTERVIEW): The Bank of Canada is bound to cut its policy rate next Wednesday and at one of two other remaining meetings this year after compelling evidence of weakness in the job market and the broader economy that will pull down elevated inflation, former finance department economist Dominique Lapointe told MNI.

BRAZIL (BBG): " Brazil’s Supreme Court sentenced Jair Bolsonaro to 27 years and three months in prison for plotting a coup after his 2022 election defeat, making him the first former president convicted of such a crime in a nation long scarred by successful and failed power grabs."

CHINA

MEXICO (BBG): "China urged Mexico to “think twice” before levying tariffs, a warning that could signal Beijing’s willingness to retaliate over a move it sees as giving into demands from the US."

REFORMS (STATE COUNCIL): China will pilot market-oriented reform in 10 regions, including Beijing, Chengdu and the Greater Bay Area, focusing on the allocation of technology, land, human resources, data, capital and environmental resources, the State Council announced.

TECH (BBG): "Alibaba Group Holding Ltd.’s stock gained the most in about two weeks after the company initiated a series of moves intended to shore up its place in China’s AI development boom."

MNI: PBOC Net Injects CNY41.7 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY230 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY41.7 billion after offsetting maturities of CNY188.3 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4319% at 09:48 am local time from the close of 1.4813% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Thursday, compared with the close of 48 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1019 Fri; -0.96% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1019 on Friday, compared with 7.1034 set on Thursday. The fixing was estimated at 7.1069 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND AUG BUSINESSNZ MANUFACTURING PMI 49.9; PRIOR 52.8

NEW ZEALAND AUG CARD SPENDING RETAIL M/M 0.7%; PRIOR 0.2%

NEW ZEALAND AUG CARD SPENDING TOTAL M/M 0.4%; PRIOR 0.6%

JAPAN JUL F IP Y/Y -0.4%; PRIOR -0.9%

JAPAN JUL CAPACITY UTILIZATION M/M -1.1%; PRIOR -1.8%

MARKETS

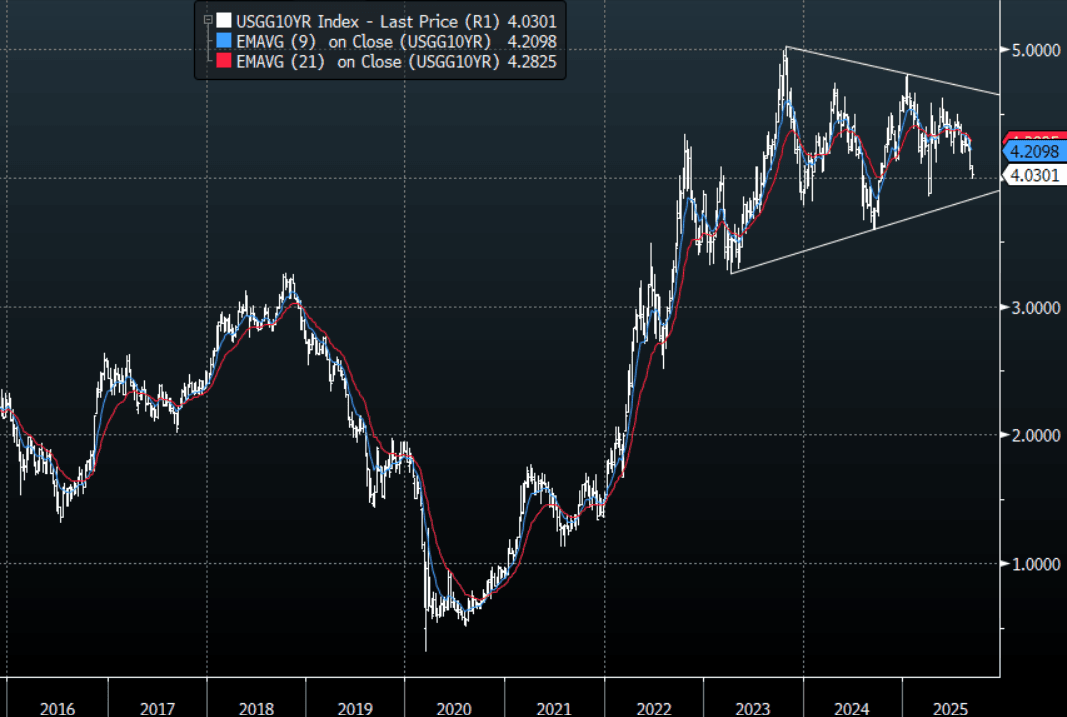

US TSYS: Asia Wrap - Yields Slightly Higher In A Quiet Friday Session

The TYZ5 range has been 113-15+ to 113-18 during the Asia-Pacific session. It last changed hands at 113-16, down 0-05 from the previous close.

- The US 2-year yield is trading around 3.542%.

- The US 10-year yield has edged higher trading around 4.03%, up 0.01 from its close.

- 10-Year Yields continued to test lower as inflation data this week proved to hold no smoking gun. The first buy-zone is now back towards the 4.15/4.20% area. Having reached the first target towards the 4.00% zone I expect some supply around this area initially. A sustained break through here and the focus will then turn towards the 3.80% area.

- Mohamed A. El-Erian on X: “With the US CPI numbers matching the consensus forecasts, the main market mover this morning is jobless claims, which came in far higher than expected. The overall signal from this week’s data is clear—and one I’ve stressed for some time, now increasingly echoed by others: inflation may still sit above the Fed’s target, but the greater risk to the economy lies in the pace and severity of labor market weakening.”

- Robin Brooks on X: “It really is starting to look like the tariff inflation shock is over. Categories in the CPI most impacted by China tariffs - like furniture (lhs) and recreational goods (rhs) - saw price spikes peak in June and then fade. August inflation in these categories is near zero…”

- RenMac on X: “Core goods CPI less cars rose just 0.13% in August, or 1.6% SAAR, the weakest pace in several months. This lends support to the notion that tariffs largely are a one-time shock to the price level. Less pressure in August from household furnishings and recreation commodities.”

- Data/Events: U. of Mich. Sentiment

Fig 1: 10-Year US Yield Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Weaker & Hovering Near Session Lows

JGB futures are weaker, -14 compared to settlement levels, and hovering near session lows.

- Joint Statement On FX Looks To Maintain Status Quo - USD/JPY Steady: Headlines have crossed following US and Japan issuing a joint statement on FX. At face value, the headlines from the statement on FX look to largely reaffirm what both sides already broadly agree to on FX markets. FX markets should be market determined and that manipulating exchange rates for competitive purposes should be avoided. Domestic policies on monetary and fiscal policy should also not be geared towards driving FX rates.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session.

- Cash JGBs are 1bp cheaper to 2bps richer across benchmarks, with the curve flatter. The benchmark 10-year yield is 0.9bp higher at 1.59% versus the cycle high of 1.649%.

- Swap rates are flat to 2bps higher. Swap spreads are wider.

- On Monday, the local calendar will be closed.

AUSSIE BONDS: Trading At Cheaps With The Curve Flatter

ACGBs (YM -3.5 & XM flat) have bear-flattened with both contracts at/or near session cheaps.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session.

- MNI INTERVIEW: Wages To Limit RBA Easing - Ex Research Chief. Trimmed-mean inflation is likely to remain near the top of the Reserve Bank of Australia's 2-3% target if wages outpace its assumptions despite its recent productivity downgrade, the RBA's former head of research told MNI, noting this would limit the degree of further easing.

- Cash ACGBs are flat to 2bps cheaper with the 3/10 curve flatter and the AU-US 10-year yield differential at +20bps.

- The bills strip is -1 to -4 across contracts, with a steepening bias. Red contracts are some 8-9bps cheaper than the session's best levels.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 10% probability, with a cumulative 28bps of easing priced by year-end.

- Today, the local calendar was empty.

- Next week, the local calendar will be empty on Monday ahead of an RBA Hunter Fire-Side Chat on Tuesday.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Bull-Flattener To Close Out Week

NZGBs closed showing a modest bull-flattener, with benchmark yields flat to 2bps lower.

- August card spending trends were mixed relative to the July pace. Retail spending rose 0.7%m/m, versus 0.2% in July. Total spending was up 0.4%, versus a 0.6%m/m gain in July. In terms of the detail, the main drag came from vehicle spending, down 0.9%m/m (after a 5.6% gain in July). Fuel spending was also weaker, off 0.1%m/m. Apparel, durables and consumables spending was all up in m/m terms, to leave core retail spending up 0.9%m/m.

- In y/y terms, total spending was -0.5%, but the continues the modest improvement seen in the series from recent lows (we were at -3.2%y/y back in April). Core retail spend was up 2.4%y/y (from 1.9% prior), so further evidence of a modest pick up in spending momentum.

- Swap rates also closed with rates flat to 2bps lower.

- RBNZ dated OIS pricing closed slightly softer across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

- Next week, the local calendar will see the Performance Services Index on Monday, Food Prices on Tuesday, Current Account Balance on Wednesday and Q2 GDP on Thursday.

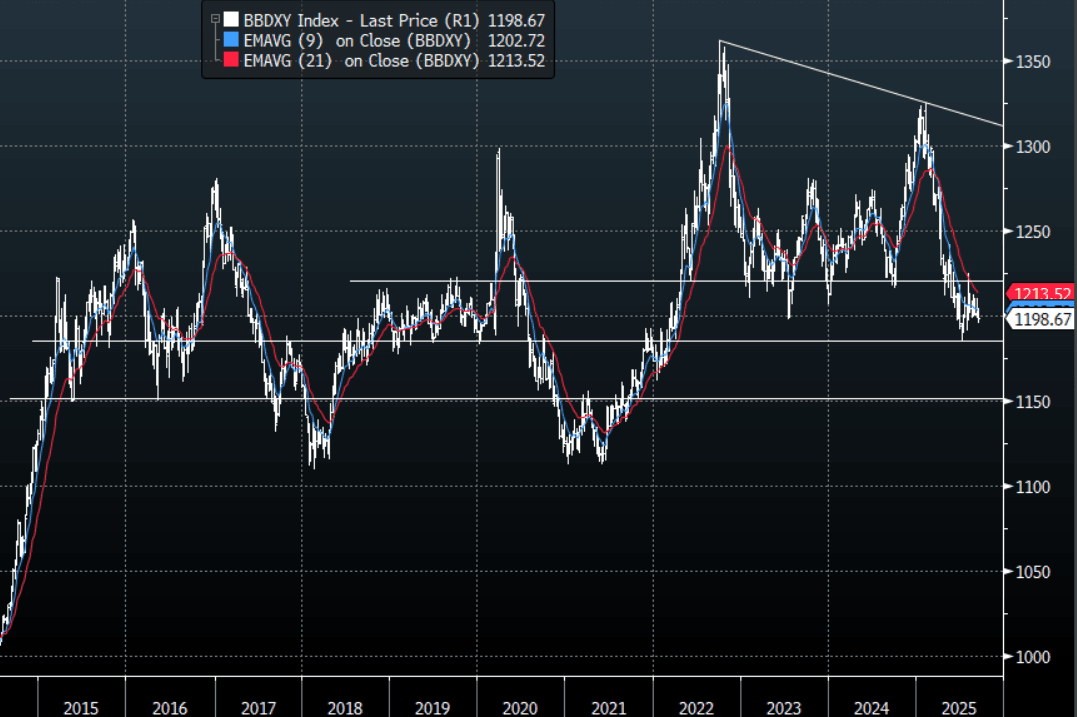

FOREX: Asia FX Wrap - BBDXY Pressing Support Heading Into The Weekend

The BBDXY has had a range of 1197.34 - 1198.76 in the Asia-Pac session; it is currently trading around 1198, +0.10%. The USD traded tried to push higher into the CPI data with the market suspecting a higher print, the benign outcome saw it very quickly reverse and we opened back below 1200 again this morning. A sustained break below 1197/1195 is needed to regain the momentum lower to retest the year's lows towards 1180 where demand should return initially. A break sub 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken.

- EUR/USD - Asian range 1.1723 - 1.1741, Asia is currently trading 1.1725. The pair bounced strongly overnight, helped by a combination of the US CPI and Lagarde . EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3554 - 1.3581, Asia is currently dealing around 1.3555. The pair is back in the middle of its recent 1.3350-1.3650 range, but price action suggests it may be looking to retest the range highs.

- USD/CNH - Asian range 7.1142 - 7.1196, the USD/CNY fix printed 7.1019, Asia is currently dealing around 7.1200. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.01%, Gold $3655, US 10-Year 4.032%, BBDXY 1198, Crude Oil $61.86

- Data/Events : Germany CPI, France CPI, Spain CPI, Italy Unemployment Rate Quarterly

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

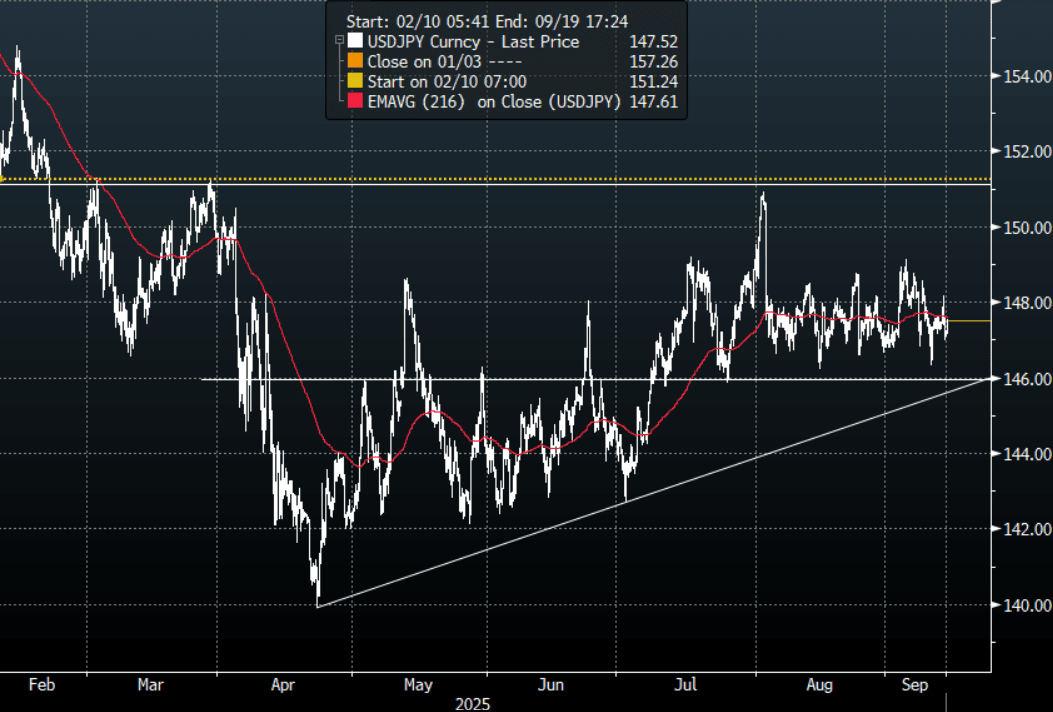

JPY: Asia Wrap - USD/JPY Continues To Hold Above Support

The USD/JPY range has been 147.12 - 147.53 in the Asia-Pac session, it is currently trading around 147.50, +0.20%. USD/JPY tried to push higher into the CPI with the market suspecting a higher print, the benign outcome saw it very quickly reverse and we opened this morning back towards 147.00 again. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so they will be hoping this support remains intact. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- Joint Statement On FX Looks To Maintain Status Quo - USD/JPY Steady: Headlines have crossed following US and Japan issuing a joint statement on FX. At face value, the headlines from the statement on FX look to largely reaffirm what both sides already broadly agree to on FX markets. FX markets should be market determined and that manipulating exchange rates for competitive purposes should be avoided. Domestic policies on monetary and fiscal policy should also not be geared towards driving FX rates.

- Samantha LaDuc on X: “Toyota can absorb the ¥1 trillion ($6.8 billion) cost of a 15% automobile tariff and make profits [it estimates ¥3 trillion ($20.4 billion) in earnings after the tariffs—rk]. However, few companies are as resilient as Toyota. According to a 2024 Cabinet Office survey of 587 large listed Japanese manufacturing exporters, the 40 most competitive companies expected to be able to record profits [on their exports] even if the yen rose to ¥101. However, the 127 least competitive companies [22% of these listed firms] would need the yen to weaken to the ¥146-152 range to be able to compete and maintain a profit.” Richard Katz Nikkei.”

- "JAPAN TRADE MINISTRY: TO RESTRICT EXPORTS TO ADDITIONAL ENTITIES, INCLUDING 6 IN CHINA, 2 IN TURKEY, 1 IN UAE, AS PART OF SANCTIONS AGAINST RUSSIA'S INVASION OF UKRAINE - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.07b), 147.40($1.6b).Upcoming Close Strikes : 146.00($1.41b Sept 16), 150.00($1.49b Sept 16) - BBG.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

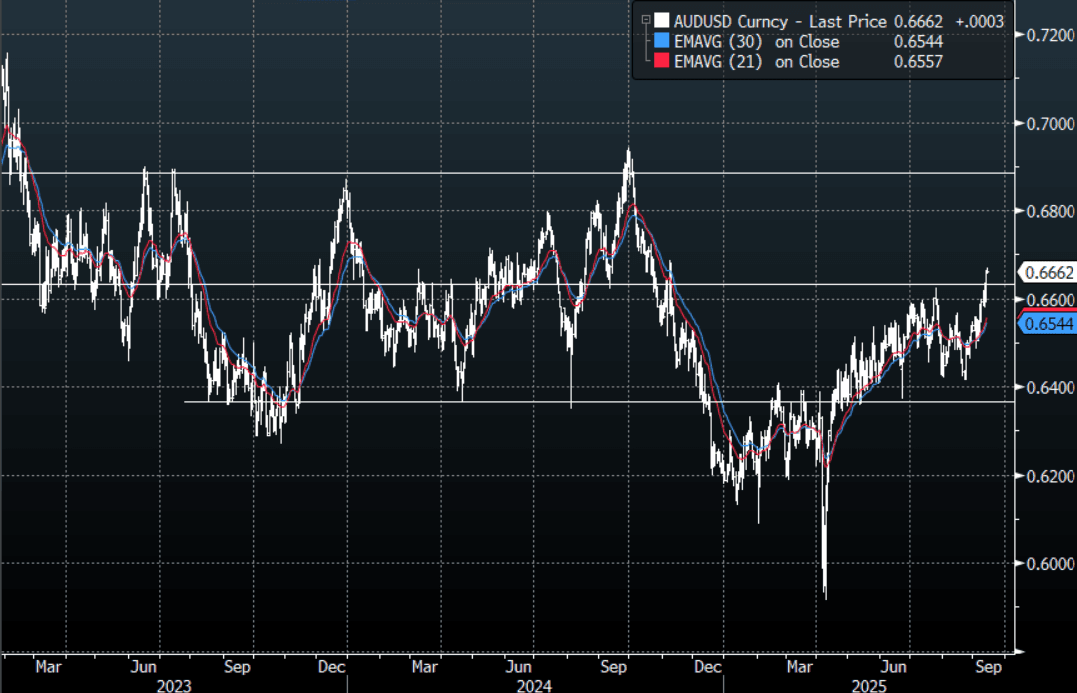

AUD: Asia Wrap - AUD/USD Probing Above 0.6650 Resistance, Can It Extend ?

The AUD/USD has had a range of 0.6656 - 0.6669 in the Asia- Pac session, it is currently trading around 0.6660, +0.05%. US stocks loved the CPI data and accelerated higher, while US yields most notably in the long-end continued lower. The AUD liked that combination and is looking to break above its pivotal 0.6650 resistance. Should the USD break and extend lower we could see the AUD gain momentum above 0.6650 and potentially target levels back towards 0.6900/0.7000. This price action suggests dips will be supported for now as we await confirmation of this potential break higher.

- Bloomberg - “An Aussie Rally May See Pensions Bolster FX Hedging: StanChart. The FX hedge ratio of foreign equities has edged up to 22.2% in Q2 from 20.6% in the prior period, “in line with our findings of limited evidence of increased FX hedging by foreign investors. This raises questions on what will lead Australia’s super funds to bolster their hedge ratios” given the Aussie’s positive correlation with risky assets is often cited as a key argument for a low hedge ratio; Chia says a medium-term rally by AUD/USD to around the 0.70 level may do that.”

- MNI INTERVIEW: Wages To Limit RBA Easing - Ex Research Chief. Trimmed-mean inflation is likely to remain near the top of the Reserve Bank of Australia’s 2-3% target if wages outpace its assumptions despite its recent productivity downgrade, the RBA’s former head of research told MNI, noting this would limit the degree of further easing.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6570(AUD383m), 0.6575(AUD377m). Upcoming Close Strikes : 0.6600(AUD449m Sept 16) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 98.01 - 98.27, Asia is trading around 98.25. The pair extended higher overnight, turning the focus back towards the 99.00/100.00 area. Dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

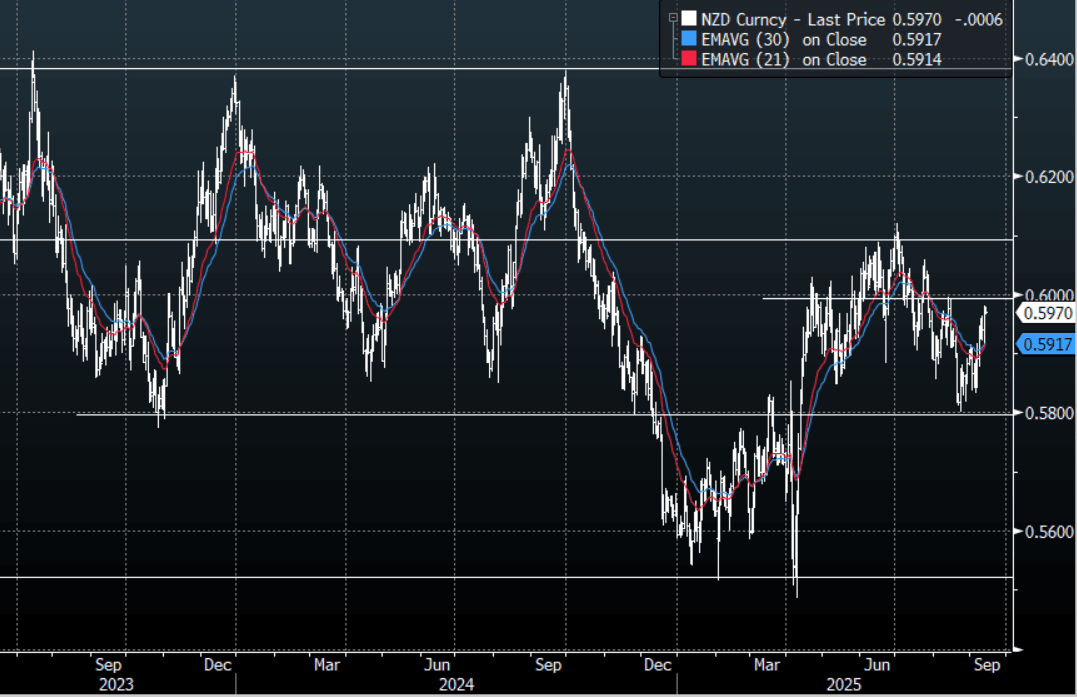

NZD: Asia Wrap - NZD/USD Challenging the Bears Conviction

The NZD/USD had a range of 0.5965 - 0.5979 in the Asia-Pac session, going into the London open trading around 0.5970, -0.10%. US stocks loved the data and accelerated higher, while US yields most notably in the long-end continued lower. The NZD found good demand towards 0.5900 and had a strong bounce in reaction to the data. The USD in particular is beginning to look vulnerable, this is dragging the NZD higher frustrating the bears. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting.

- August Card Spending Mixed, But Core Trends Improving : August card spending trends were mixed relative to the July pace. Retail spending rose 0.7%m/m, versus 0.2% in July. Total spending was up 0.4%, versus a 0.6%m/m gain in July.

- PMI Down In August, But Q3 TO Date Average Still Above Q2 Pace: The New Zealand manufacturing PMI fell back into contractionary territory in August. The 49.9 print compares with 52.8 for July. The index is still above recent lows (47.6 recorded in May), but continues the stop/start nature of NZ sentiment indicators.

- Bloomberg - “Tsy Secretary Bessent To Meet China Officials Next Week - Rtrs : Headlines have crossed from Reuters that US Tsy Secretary Bessent will meet with China officials, including Vice Premier He Lifeng, in Spain next week. The discussions are expected to cover - "trade, economic and national security issues". Tiktok is also expected to be discussed per Rtrs.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.6250(NZD427m Sept 17) - BBG

- AUD/NZD range for the session has been 1.1144 - 1.1159, currently trading 1.1155. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Strong Week for Most, NIKKEI Hits New Highs

Japanese stocks rose for a third day, led by gains in the tech sector, on with gains from tech stocks in the US flowing through to buying of AI-related shares in Japan. Several key bourses in the regions have either hit or are approaching news highs this week on hopes for a cut in interest rates at the Federal Reserve. Signs of life for China's property developers as Evergrande jumped 40% on Friday morning on news of a possible bid. With the exception of the Jakarta Composite, which fell on the news of the departure of the Finance Minister, all major bourses have posted positive gains for the week.

- China's major bourses are finishing the week up with the Hang Seng leading the way. Up +1.53%, the Hang Seng is over +4.2% higher for the week. The CSI 300 is only marginally up today but higher by +1.98% for the week. The Shanghai Comp is up +0.24% Friday, and +1.89% for the week. The Shenzhen Comp is up +0.20% today, and +2.82% for the week.

- The NIKKEI is up again, reaching new highs of 44,812. Up 1% Friday, the weekly gain of just over 4% comes despite having one day of declines.

- Taiwan's TAIEX has seen major portfolio flows ramp up and is up +0.69% Friday and +3.66% for the week.

- The KOSPI is having a very strong period of late, up +1.28% Friday and +5.71% for the week on hopes that the planned tax changes to capital gains won't proceed.

- The FTSE Malay KLCI continues to underperform relative to regional peers. Up +0.42% today, it is higher by just +0.71% for the week.

- The Jakarta Composite is up +1.04% today but unable to recover from losses earlier in the week; to be down -0.49% week to date.

- The NIFTY 50 is higher by +0.35% Friday morning, and up +1.3% for the week.

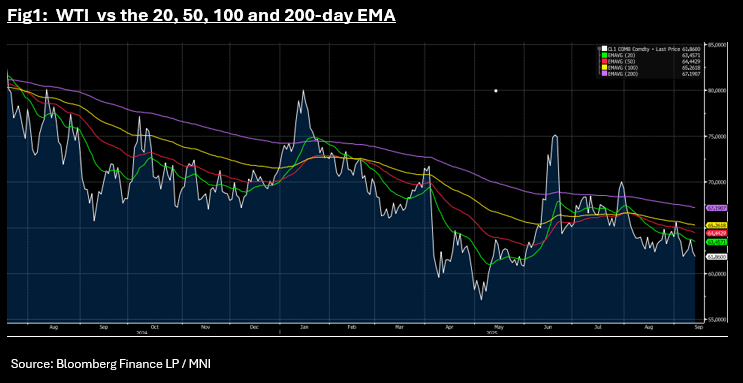

Oil Falls Again, Wiping Out Weekly Gains

- Oil dipped further in the Asia trading day, wiping out the gains delivered earlier in the week.

- Despite the IEA trying to temper expected further supply increases with suggestions there could be a modest uptick in demand, the current IEA projections are for world oil output to exceed demand in 2026 by over 3 million barrels per day, placing downward pressure on prices.

- WTI is off -0.82% today at US$61.85 bbl to be largely unchanged for the week. The early part of the week had seen three days of decent gains, resulting in WTI approaching the 20-day EMA of $63.49. Last night's sell off that continued into today has seen it push back below all major moving averages.

- Brent is lower by -0.72% today, but remains up +0.60% for the week. Brent too has traded below all major moving averages with the 20-day EMA above at US$67.14.

- BBG reports that a Goldman Sachs research report suggests that China could continue the ongoing stockpiling of oil into 2026, aiming to lock into the benefit of lower prices whilst predicting Brent to reach the around US$55 bbl. Saudi Aramco is set to sell ~50-51 million bbls of contractual supplies of Oct.-loading crude to customers in China, higher than 43 million bbls a month ago, according to traders informed by the producer.

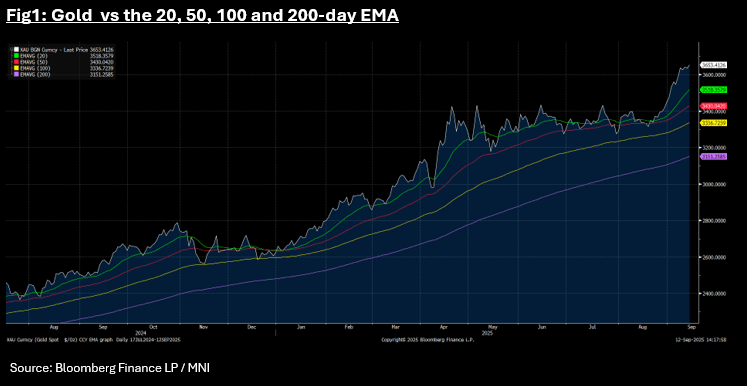

GOLD: Another Record High for Gold

- Gold had softened overnight also in what has been a mixed week of performance for the precious metal as it bounces off new all time highs.

- Having closed at a new high of US$3,640.75 on Wednesday, the fall of -0.18% overnight appears to be driven by profit taking as the 14-day Relative Strength Index points to it looking over-bought market.

- However this didn't stop the bulls taking over in the Asia trading day with gold up +0.53% to a new record high of US$3,653.26.

- For the week, gold has delivered solid gains of +1.85% to see year to date gains, over 38%.

- Gold is highly sensitive to interest rate cuts and with economic data suggesting the probability of a cut is improving, gold has risen.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/09/2025 | 0430/1330 | ** | Industrial Production | |

| 12/09/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 12/09/2025 | 0600/0700 | ** | Trade Balance | |

| 12/09/2025 | 0600/0700 | ** | Index of Services | |

| 12/09/2025 | 0600/0700 | ** | Index of Production | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0645/0845 | *** | HICP (f) | |

| 12/09/2025 | 0700/0900 | *** | HICP (f) | |

| 12/09/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/09/2025 | 0900/1100 | Labour Market Quarterly Statistics | ||

| 12/09/2025 | - | *** | Money Supply | |

| 12/09/2025 | - | *** | New Loans | |

| 12/09/2025 | - | *** | Social Financing | |

| 12/09/2025 | 1230/0830 | * | Building Permits | |

| 12/09/2025 | 1400/1000 | * | Services Revenues | |

| 12/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 12/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 12/09/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |