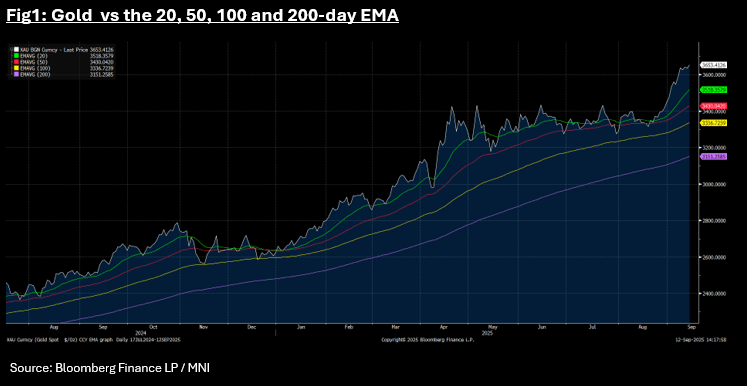

GOLD: Another Record High for Gold

Sep-12 04:21

- Gold had softened overnight also in what has been a mixed week of performance for the precious metal as it bounces off new all time highs.

- Having closed at a new high of US$3,640.75 on Wednesday, the fall of -0.18% overnight appears to be driven by profit taking as the 14-day Relative Strength Index points to it looking over-bought market.

- However this didn't stop the bulls taking over in the Asia trading day with gold up +0.53% to a new record high of US$3,653.26.

- For the week, gold has delivered solid gains of +1.85% to see year to date gains, over 38%.

- Gold is highly sensitive to interest rate cuts and with economic data suggesting the probability of a cut is improving, gold has risen.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

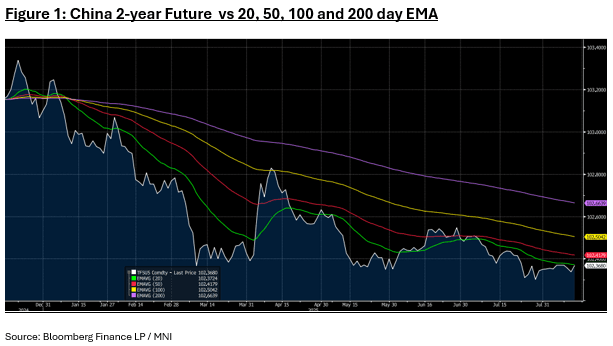

CHINA: Bond Futures Mixed in Morning Trade

Aug-13 04:20

- China's bond futures are moving in opposite direction in the morning session.

- The 10-year is lower by -0.02 at 108.36 to remain below all major moving averages.

- The 2-year is up +0.03 at 102.36, nearing the 20-day EMA of 102.37.

- Ten year government bond yields are modestly lower with the 10-year at 1.72%

GOLD: Gold Range Trading Post-US CPI Data, Fed Speakers Later

Aug-13 04:18

Gold prices have been moving in a narrow range during today’s APAC session with few drivers after rising 0.2% to $3348.26/oz on Tuesday as the market priced in a higher probability of a Fed rate cut in September, now around 95%, following July US CPI data showing subdued goods inflation despite higher import duties.

- Bullion fell to a low of $3342.78 before rising to $3354.35 to be 0.1% higher today at $3351.1. It is trading between initial resistance at $3409.2, 8 August high, and support at $3268.2, 30 July low. The US dollar and yields are also steady.

- Silver has outperformed today rising 0.7% to $38.193, close to the intraday high. It fell to $37.85 early in the session. The technical trend remains bullish with initial resistance at $39.655. Initial support is at $36.216, 31 July low.

- Equities are generally stronger with the Hang Seng up 1.9% and Nikkei +1.6% but S&P e-mini flat and ASX down 0.5%. Oil prices are flat with WTI around $63.18/bbl. Copper is down 0.3%.

- Later the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

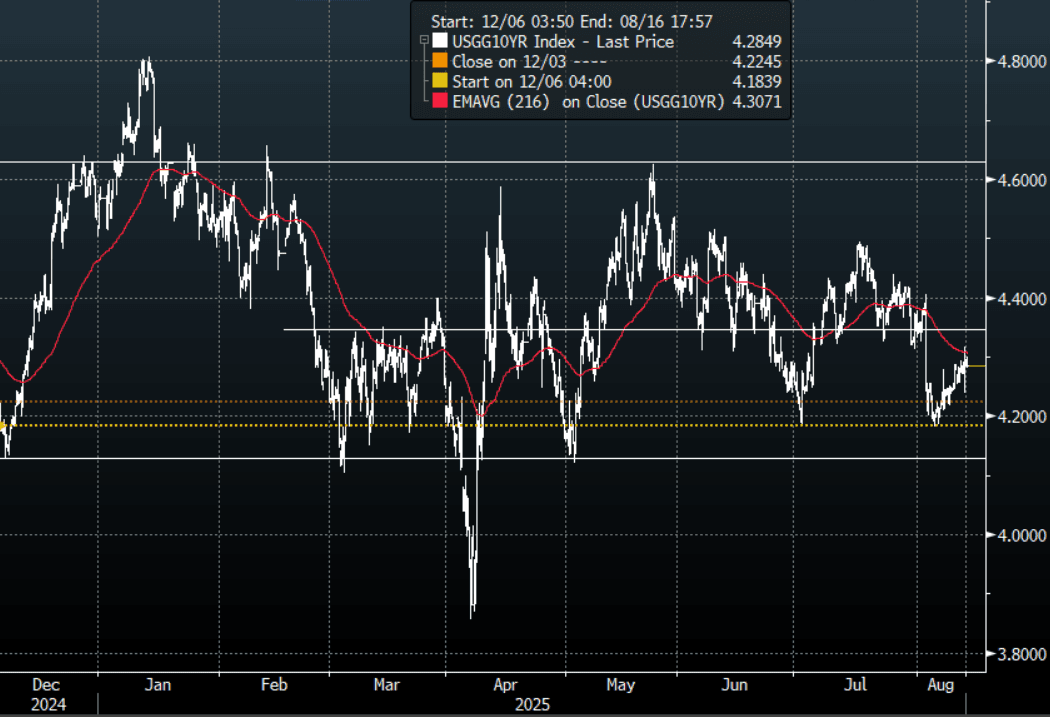

US TSYS: Yield Moves Muted In A Quiet Session

Aug-13 04:14

The TYU5 range has been 111-23 to 111-27 during the Asia-Pacific session. It last changed hands at 111-27, up 0-01 from the previous close.

- The US 2-year yield is trading around 3.73%, unchanged from its close.

- The US 10-year yield has edged slightly lower trading around 4.285%.

- Price action in the long-end is a little disconcerting for the bulls though the 10-Year yield still trades below its 4.30/35%% pivot within the wider range 4.10% - 4.65%. There should still be buyers of treasuries on bounces back towards 4.30/35%, looking to initially test the 4.10% area.

- Ben Hunt(Epsilon Theory) on X: “If we’re gonna cut in Sept (90% mkt odds as I write this) with core at 3.1% and rising, wages at 3.9% and rising, stocks and home prices at all-time highs … Can we at least stop talking about the Fed’s 2% inflation ‘target’? It’s just insulting to continue this charade.”

- Jim Bianco on X: “YoY Core CPI, 3.1%. Up 0.3% in the last 3-months. In the last 40 YEARS, only once has the Fed CUT rates when core was above 3% AND the 3m chg was >0.3%, Oct 1990 to Mar 1991. Agree with @EpsilonTheory, the 2% inflation target is dead. We are accepting a higher inflation world.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P