MNI US Inflation Insight: Solid But Could Have Been Firmer

Sep-12 14:58By: Chris Harrison and 1 more...

Federal Reserve+ 3

Download Full Report Here

- PPI started this week’s inflation releases with a report that relieved concerns about tariff-related price pressures whilst highlighting the volatile and revision-prone nature of the trade services category.

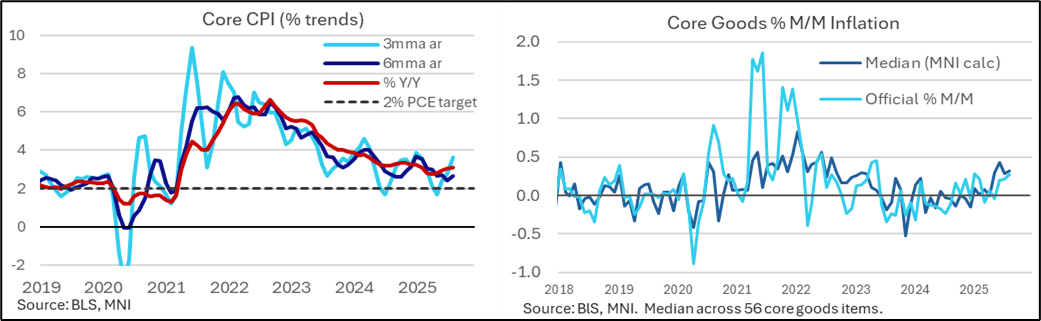

- CPI then followed and was marginally stronger than expected on a M/M basis for both headline and core but with a more benign readthrough to core PCE – analyst estimates are tracking at ~0.20% M/M.

- Underlying core goods inflation is still running at a robust monthly clip, as it has been since April when it stepped markedly higher, although its peak for now appears to have been in June.

- With CPI inflation readings reasonable close to expectations, we believe the main driver of the dovish reaction was instead a spike in initial jobless claims with some paring of that move owing to a concentration in Texas.