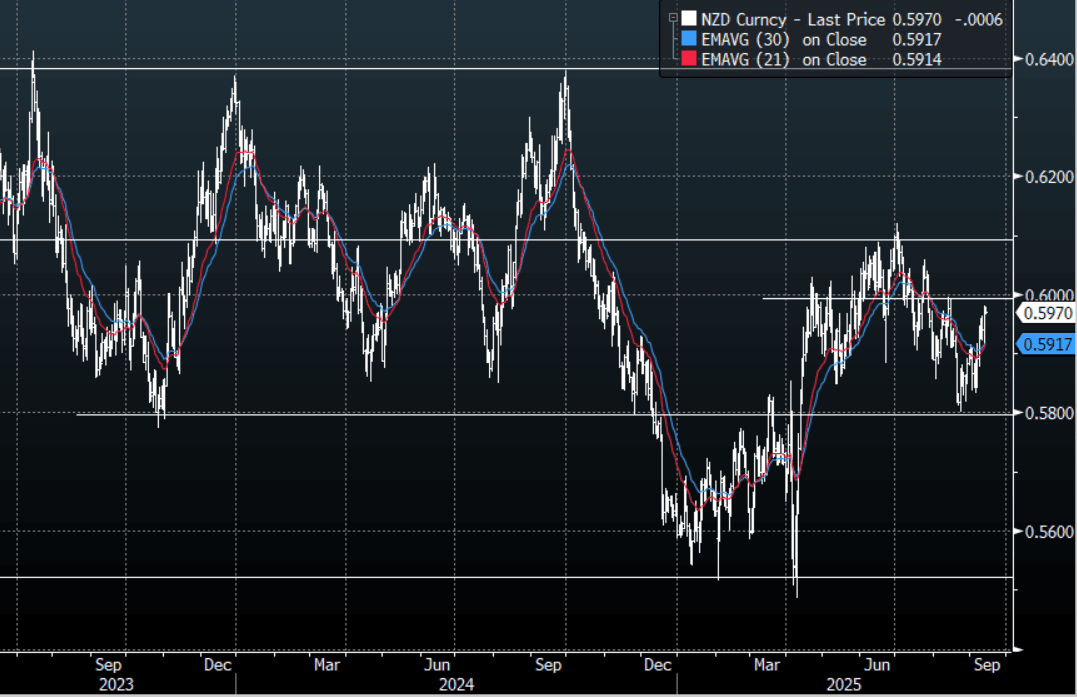

NZD: Asia Wrap - NZD/USD Challenging the Bears Conviction

The NZD/USD had a range of 0.5965 - 0.5979 in the Asia-Pac session, going into the London open trading around 0.5970, -0.10%. US stocks loved the data and accelerated higher, while US yields most notably in the long-end continued lower. The NZD found good demand towards 0.5900 and had a strong bounce in reaction to the data. The USD in particular is beginning to look vulnerable, this is dragging the NZD higher frustrating the bears. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting.

- August Card Spending Mixed, But Core Trends Improving : August card spending trends were mixed relative to the July pace. Retail spending rose 0.7%m/m, versus 0.2% in July. Total spending was up 0.4%, versus a 0.6%m/m gain in July.

- PMI Down In August, But Q3 TO Date Average Still Above Q2 Pace: The New Zealand manufacturing PMI fell back into contractionary territory in August. The 49.9 print compares with 52.8 for July. The index is still above recent lows (47.6 recorded in May), but continues the stop/start nature of NZ sentiment indicators.

- Bloomberg - “Tsy Secretary Bessent To Meet China Officials Next Week - Rtrs : Headlines have crossed from Reuters that US Tsy Secretary Bessent will meet with China officials, including Vice Premier He Lifeng, in Spain next week. The discussions are expected to cover - "trade, economic and national security issues". Tiktok is also expected to be discussed per Rtrs.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.6250(NZD427m Sept 17) - BBG

- AUD/NZD range for the session has been 1.1144 - 1.1159, currently trading 1.1155. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

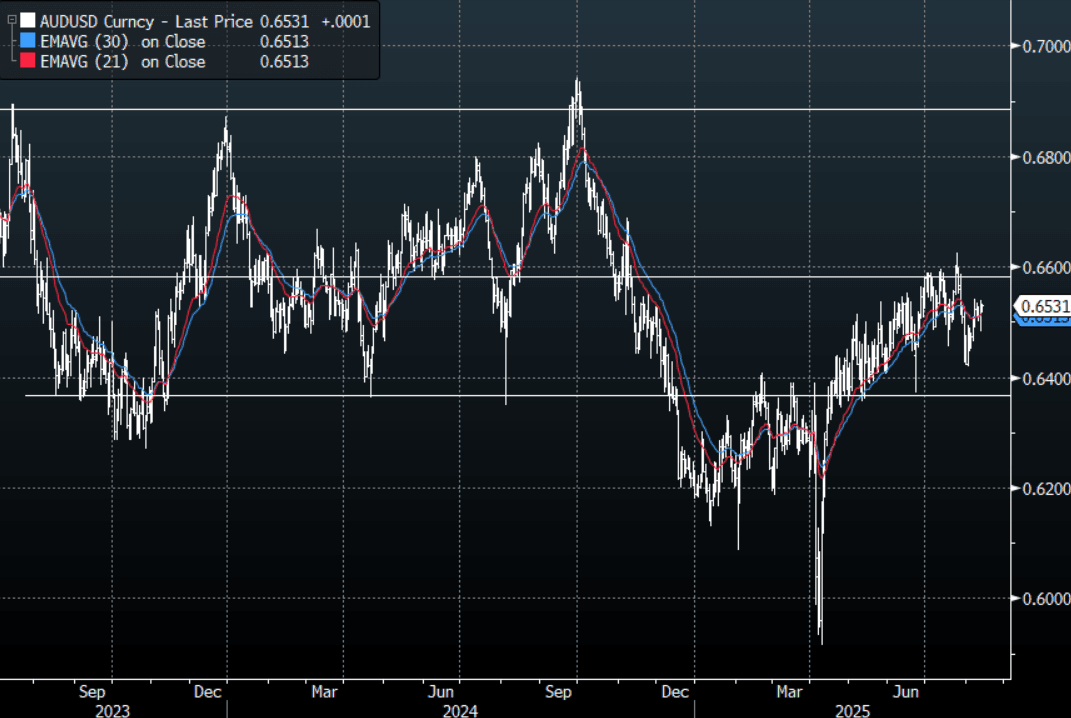

AUD: Asia Wrap - AUD/USD Consolidates Back Above 0.6500

The AUD/USD has had a range of 0.6517 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6530, +0.02%. US equities roared higher as the market gets ready for more rate cuts, the slight reprieve for the USD going into the print was quickly reversed. The more cuts being priced in increases the pressure on an already bearish USD market. I felt the bounce back towards 0.6550 offered a good risk/reward to fade initially but if the US starts pricing in more aggressive cuts can the AUD ignore it? The Price remains firmly in the 0.6350-0.6650 range, if the USD extends lower can it test the top end?

- MNI AUSTRALIA: Consensus Expects Some Normalisation In July Labour Data. With May and June employment gains disappointing, the July data will be monitored closely for signs that the labour market has turned. Q2 employment averaged 28.8k/month up from Q1’s 1.4k but slightly lower than Q2 2024’s 32.2k. Bloomberg consensus expects a 25k gain in July after June’s +2k, slightly below the Q2 average. The unemployment rate is forecast to decline 0.1pp to 4.2%, returning to the Q2 average.

- MNI AU DATA: Public Pay Growth Outpacing Private Sector. The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6575(AUD746m), 0.6550(AUD597m). Upcoming Close Strikes : 0.6600(AUD1.25b Aug 14), 0.6690(AUD583m Aug 14), 0.6523(AUD562m Aug15) - BBG

- AUD/JPY - Asia-Pac range 96.40 - 96.70, Asia is trading around 96.70. The pair has bounced and is testing its first resistance around the 96.50/97.00 area. There should be sellers around here initially, but a break above 97.50 though would negate this and reinstate the momentum higher.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

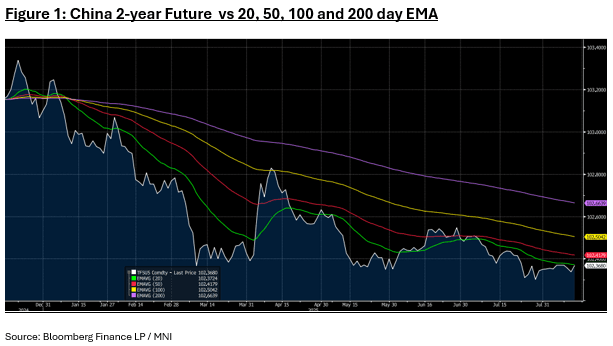

CHINA: Bond Futures Mixed in Morning Trade

- China's bond futures are moving in opposite direction in the morning session.

- The 10-year is lower by -0.02 at 108.36 to remain below all major moving averages.

- The 2-year is up +0.03 at 102.36, nearing the 20-day EMA of 102.37.

- Ten year government bond yields are modestly lower with the 10-year at 1.72%

GOLD: Gold Range Trading Post-US CPI Data, Fed Speakers Later

Gold prices have been moving in a narrow range during today’s APAC session with few drivers after rising 0.2% to $3348.26/oz on Tuesday as the market priced in a higher probability of a Fed rate cut in September, now around 95%, following July US CPI data showing subdued goods inflation despite higher import duties.

- Bullion fell to a low of $3342.78 before rising to $3354.35 to be 0.1% higher today at $3351.1. It is trading between initial resistance at $3409.2, 8 August high, and support at $3268.2, 30 July low. The US dollar and yields are also steady.

- Silver has outperformed today rising 0.7% to $38.193, close to the intraday high. It fell to $37.85 early in the session. The technical trend remains bullish with initial resistance at $39.655. Initial support is at $36.216, 31 July low.

- Equities are generally stronger with the Hang Seng up 1.9% and Nikkei +1.6% but S&P e-mini flat and ASX down 0.5%. Oil prices are flat with WTI around $63.18/bbl. Copper is down 0.3%.

- Later the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.