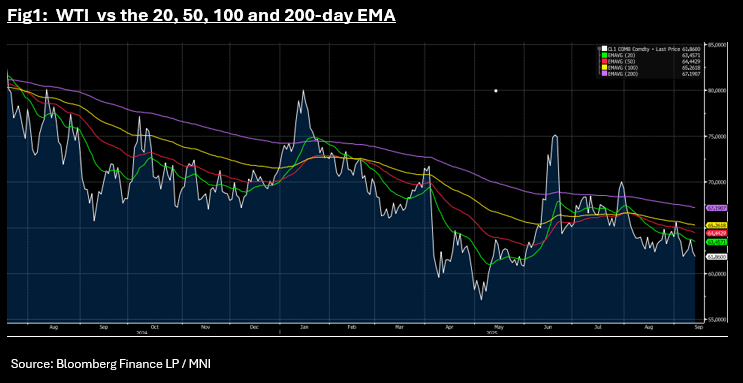

OIL: Oil Falls Again, Wiping Out Weekly Gains

- Oil dipped further in the Asia trading day, wiping out the gains delivered earlier in the week.

- Despite the IEA trying to temper expected further supply increases with suggestions there could be a modest uptick in demand, the current IEA projections are for world oil output to exceed demand in 2026 by over 3 million barrels per day, placing downward pressure on prices.

- WTI is off -0.82% today at US$61.85 bbl to be largely unchanged for the week. The early part of the week had seen three days of decent gains, resulting in WTI approaching the 20-day EMA of $63.49. Last night's sell off that continued into today has seen it push back below all major moving averages.

- Brent is lower by -0.72% today, but remains up +0.60% for the week. Brent too has traded below all major moving averages with the 20-day EMA above at US$67.14.

- BBG reports that a Goldman Sachs research report suggests that China could continue the ongoing stockpiling of oil into 2026, aiming to lock into the benefit of lower prices whilst predicting Brent to reach the around US$55 bbl. Saudi Aramco is set to sell ~50-51 million bbls of contractual supplies of Oct.-loading crude to customers in China, higher than 43 million bbls a month ago, according to traders informed by the producer.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia Wrap - USD Bears Back In Charge ?

The BBDXY has had a range of 1202.63 - 1204.07 in the Asia-Pac session, it is currently trading around 1203, -0.02%. The USD collapsed in the N/Y Session as the market rushed to re-enter or add to USD shorts. This is clearly the side the market is more comfortable trading and a sustained break below 1197 could see the move lower regain momentum and a retest of the year's lows.

- EUR/USD - Asian range 1.1670 - 1.1688, Asia is currently trading 1.1685. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. Will this second attempt have the impetus to break through.

- GBP/USD - Asian range 1.3493 - 1.3508, Asia is currently dealing around 1.3505. The pair bounced nicely off the 1.3100/1.3200 support area. Like a few other G10 currencies the reasons to fade this initial impulse higher don’t look as strong, as the USD begins to look vulnerable again.

- USD/CNH - Asian range 7.1817 - 7.1883, the USD/CNY fix printed 7.1350, Asia is currently dealing around 7.1830. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.05%, Gold $3350, US 10-Year 4.287%, BBDXY 1203, Crude Oil $63.23

- Data/Events : Germany Wholesale Price Index/CPI, Spain CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

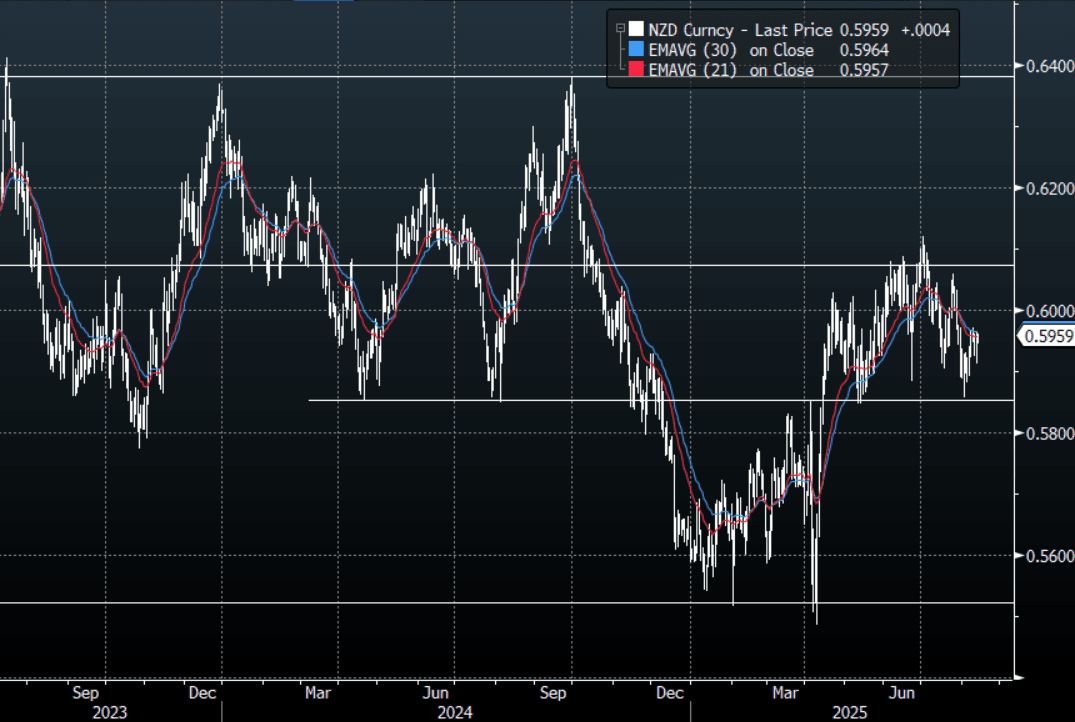

NZD: Asia Wrap - NZD/USD Slightly Higher As USD Bears Wrestle Back Control

The NZD/USD had a range of 0.5945 - 0.5961 in the Asia-Pac session, going into the London open trading around 0.5960, +0.08%. US equities roared higher as the market got ready for more rate cuts, the slight reprieve for the USD going into the print was quickly reversed and more cuts being priced in will increase the pressure on an already bearish USD market. Risk has ben pretty mute today, E-minis +0.05%, NQU5 +0.09%. The NZD/USD is still firmly within its 0.5850-0.6150 range, the CPI print last night will probably give pause to those wanting to fade the bounce, can it give it the boost it needs to regain upward momentum though, time will tell.

- MNI NZ: Gradual Recovery In Retail Card Spending. July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- (Bloomberg) - "China Consumer Loan Subsidy Expected to Drive Lending Recovery. China’s consumer loan interest subsidy program is expected to support a recovery in lending, especially for operating loans in the consumer services sector, while benefiting major banks and enhancing their market share, according to analysts from brokerages including China Merchants Securities." BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD300m Aug 14). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0955 - 1.0969, currently trading 1.0960. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

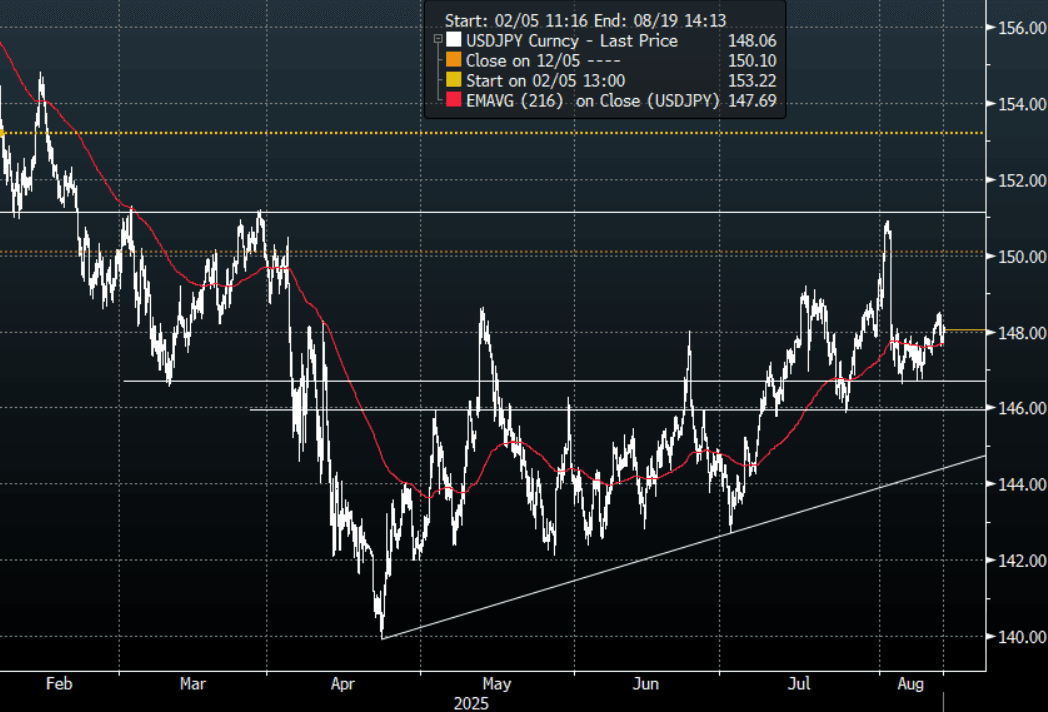

JPY: Asia Wrap - USD/JPY Finds Demand Sub 148.00

The Asia-Pac USD/JPY range has been 147.70 - 148.17, Asia is currently trading around 148.05, +0.15%. USD/JPY’s gains going into the US CPI were quickly reversed after the print. Price is currently still holding above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. Until then, the recent range of 146.50-148.50 will continue to dominate. Decent demand seen below 148.00 in our session.

- JAPAN DATA July PPI In Line, Suggests Further Moderation In Headline Y/Y CPI: Japan's July PPI was close to expectations. The m/m outcome printed at +0.2%, in line with expectations, while the June outcome was revised to 0.1%m/m (originally reported as -0.2%). In y/y terms we printed at 2.6%, versus 2.5% forecast and 2.9% prior.

- JAPAN DATA Import Prices Up For First Month Since Jan, Y/Y Still Negative : For July, export and import prices both rose in m/m terms. Export prices were up 1.6%, while import prices were up 2.4%m/m. For import prices this was the first m/m rise since January of this year. In y/y terms, both export and import prices were still in negative territory, but up from the June levels. Export prices were -5.4%y/y, while imports were -10.4%.

- "JAPAN'S AKAZAWA: NOT BAD IF TRUMP EXEC ORDER COMES BY MID SEPT, US CAN'T GET INVESTMENT HELP IF PROMISES NOT KEPT. JAPAN COULD INCREASE ACTUAL US INVESTMENT PERCENTAGE, 1-2%, INVESTMENT FOLLOWS PAST CASES, COULD BE HIGHER" - BBG

- "AKAZAWA: WILL SUPPORT ISHIBA IF HE RUNS AGAIN FOR LDP HEAD" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.06b), 146.85($751m).Upcoming Close Strikes : 149.00($1.15b Aug 14) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P