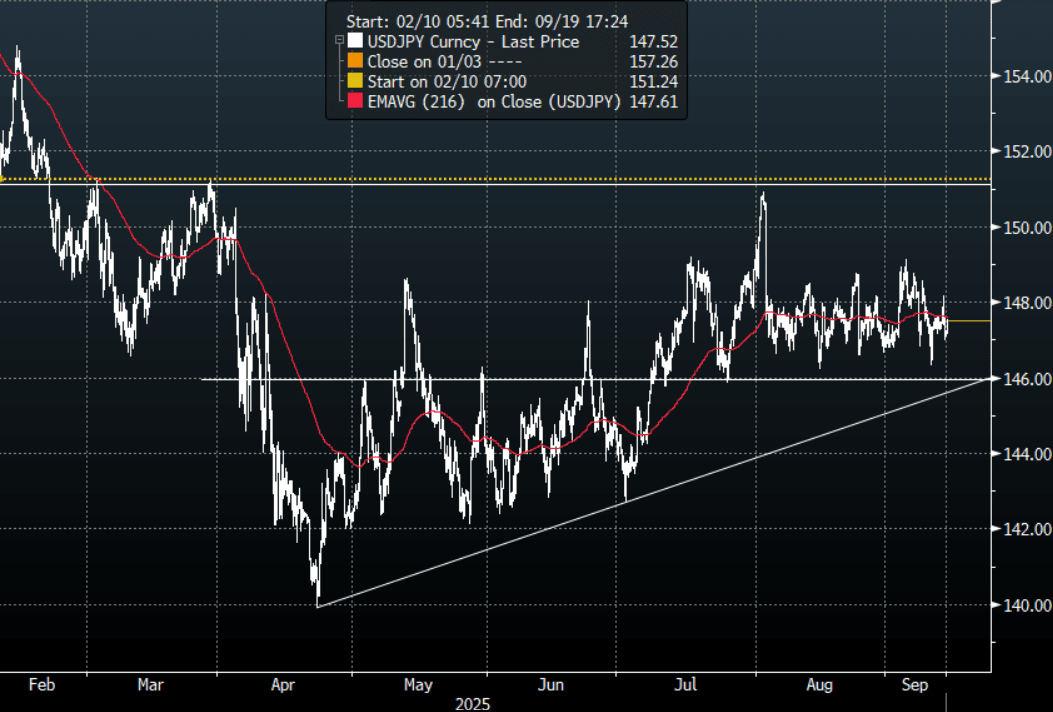

JPY: Asia Wrap - USD/JPY Continues To Hold Above Support

The USD/JPY range has been 147.12 - 147.53 in the Asia-Pac session, it is currently trading around 147.50, +0.20%. USD/JPY tried to push higher into the CPI with the market suspecting a higher print, the benign outcome saw it very quickly reverse and we opened this morning back towards 147.00 again. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so they will be hoping this support remains intact. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- Joint Statement On FX Looks To Maintain Status Quo - USD/JPY Steady: Headlines have crossed following US and Japan issuing a joint statement on FX. At face value, the headlines from the statement on FX look to largely reaffirm what both sides already broadly agree to on FX markets. FX markets should be market determined and that manipulating exchange rates for competitive purposes should be avoided. Domestic policies on monetary and fiscal policy should also not be geared towards driving FX rates.

- Samantha LaDuc on X: “Toyota can absorb the ¥1 trillion ($6.8 billion) cost of a 15% automobile tariff and make profits [it estimates ¥3 trillion ($20.4 billion) in earnings after the tariffs—rk]. However, few companies are as resilient as Toyota. According to a 2024 Cabinet Office survey of 587 large listed Japanese manufacturing exporters, the 40 most competitive companies expected to be able to record profits [on their exports] even if the yen rose to ¥101. However, the 127 least competitive companies [22% of these listed firms] would need the yen to weaken to the ¥146-152 range to be able to compete and maintain a profit.” Richard Katz Nikkei.”

- "JAPAN TRADE MINISTRY: TO RESTRICT EXPORTS TO ADDITIONAL ENTITIES, INCLUDING 6 IN CHINA, 2 IN TURKEY, 1 IN UAE, AS PART OF SANCTIONS AGAINST RUSSIA'S INVASION OF UKRAINE - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.07b), 147.40($1.6b).Upcoming Close Strikes : 146.00($1.41b Sept 16), 150.00($1.49b Sept 16) - BBG.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Range Trading Post-US CPI Data, Fed Speakers Later

Gold prices have been moving in a narrow range during today’s APAC session with few drivers after rising 0.2% to $3348.26/oz on Tuesday as the market priced in a higher probability of a Fed rate cut in September, now around 95%, following July US CPI data showing subdued goods inflation despite higher import duties.

- Bullion fell to a low of $3342.78 before rising to $3354.35 to be 0.1% higher today at $3351.1. It is trading between initial resistance at $3409.2, 8 August high, and support at $3268.2, 30 July low. The US dollar and yields are also steady.

- Silver has outperformed today rising 0.7% to $38.193, close to the intraday high. It fell to $37.85 early in the session. The technical trend remains bullish with initial resistance at $39.655. Initial support is at $36.216, 31 July low.

- Equities are generally stronger with the Hang Seng up 1.9% and Nikkei +1.6% but S&P e-mini flat and ASX down 0.5%. Oil prices are flat with WTI around $63.18/bbl. Copper is down 0.3%.

- Later the Fed’s Barkin, Goolsbee and Bostic speak. Apart from July updates for German & Spanish CPI, there are no data of note.

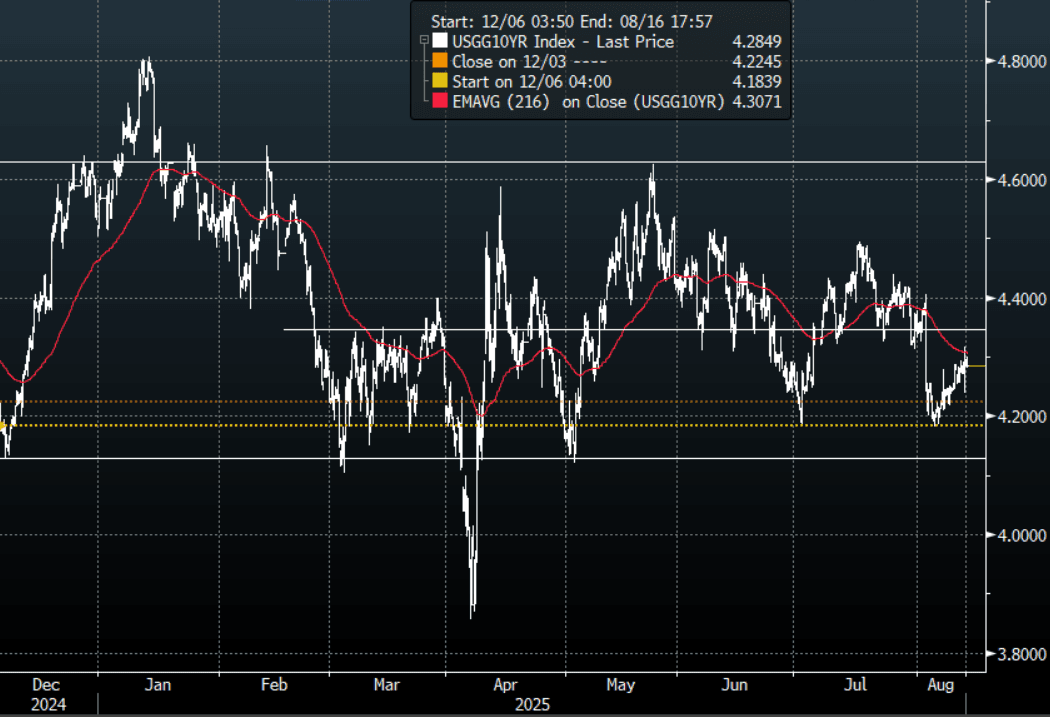

US TSYS: Yield Moves Muted In A Quiet Session

The TYU5 range has been 111-23 to 111-27 during the Asia-Pacific session. It last changed hands at 111-27, up 0-01 from the previous close.

- The US 2-year yield is trading around 3.73%, unchanged from its close.

- The US 10-year yield has edged slightly lower trading around 4.285%.

- Price action in the long-end is a little disconcerting for the bulls though the 10-Year yield still trades below its 4.30/35%% pivot within the wider range 4.10% - 4.65%. There should still be buyers of treasuries on bounces back towards 4.30/35%, looking to initially test the 4.10% area.

- Ben Hunt(Epsilon Theory) on X: “If we’re gonna cut in Sept (90% mkt odds as I write this) with core at 3.1% and rising, wages at 3.9% and rising, stocks and home prices at all-time highs … Can we at least stop talking about the Fed’s 2% inflation ‘target’? It’s just insulting to continue this charade.”

- Jim Bianco on X: “YoY Core CPI, 3.1%. Up 0.3% in the last 3-months. In the last 40 YEARS, only once has the Fed CUT rates when core was above 3% AND the 3m chg was >0.3%, Oct 1990 to Mar 1991. Agree with @EpsilonTheory, the 2% inflation target is dead. We are accepting a higher inflation world.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mostly A Sea Of Green Following US Lead, Aust Lags

Asian stocks markets are nearly higher across the board (with the ASX 200 and Philippines bourse the main outliers at this stage). After very strong gains in cash Tuesday trade, as speculation grew for Fed easing after the US CPI print), US futures are close to unchanged so far in Wednesday trade. Nevertheless, the positive spillover is evident for most parts of the region.

- Japan markets continue to rally, the NKY 225, up around +1.4% and above 43300, which is a fresh record high. The Topix is up +0.90%, while a poor 5yr debt auction has impacted sentiment at this stage. Positive spill over from US moves have been cited as a major driver so far today.

- In US trade on Tuesday, the SOX index rose nearly 3.0%. The Taiex, in Taiwan, was up in the first part of trade, tracking to a fresh record high, but is now back around flat. South Korea's Kospi is up 0.65%, back above the 3200 level. Foreign investors have been net buyers so far today (per NBUY on BBG), while onshore institutional and retail investors have been net sellers.

- China and Hong Kong markets are also higher. The CSI 300 last around +0.90%. Earlier we heard from the authorities who outlined plans on consumption subsidies (via subsidizing personal loans) to boost consumption. The HSI is up around +1.90%, with the tech sub index +2.35%.

- In South East Asia, Thailand markets have returned from a two-day break and are higher by 0.75%. We have the BoT later, which is expected to cut, albeit as a close call. Malaysia and Indonesia are both up over 1%, but the Philippines is lagging.

- In Australia, the ASX 200 is struggling, last down around 0.50%. Reported profit taking on CBA (after it posted results) is weighing on financial related stocks.