MNI EUROPEAN OPEN: US Announces Reciprocal Tariff Rates

EXECUTIVE SUMMARY

- TRUMP IMPOSES SWEEPING GLOBAL TARIFFS WITH MINIMUM RATE OF 10%- BBG

- SWITZERLAND SLAMMED WITH 39% TARIFF RATE IN TRUMP TRADE BLITZ - BBG

- TRUMP ESCALATES TRADE WAR WITH CANADA FOLLOWING PALESTINE STANCE - RTRS

- JAPAN’S KATO VOICES CONCERN WITH YEN AT WEAKEST SINCE MARCH - BBG

- S&P CHINA MFG. PMI FALLS INTO CONTRACTION IN JULY - MNI BRIEF

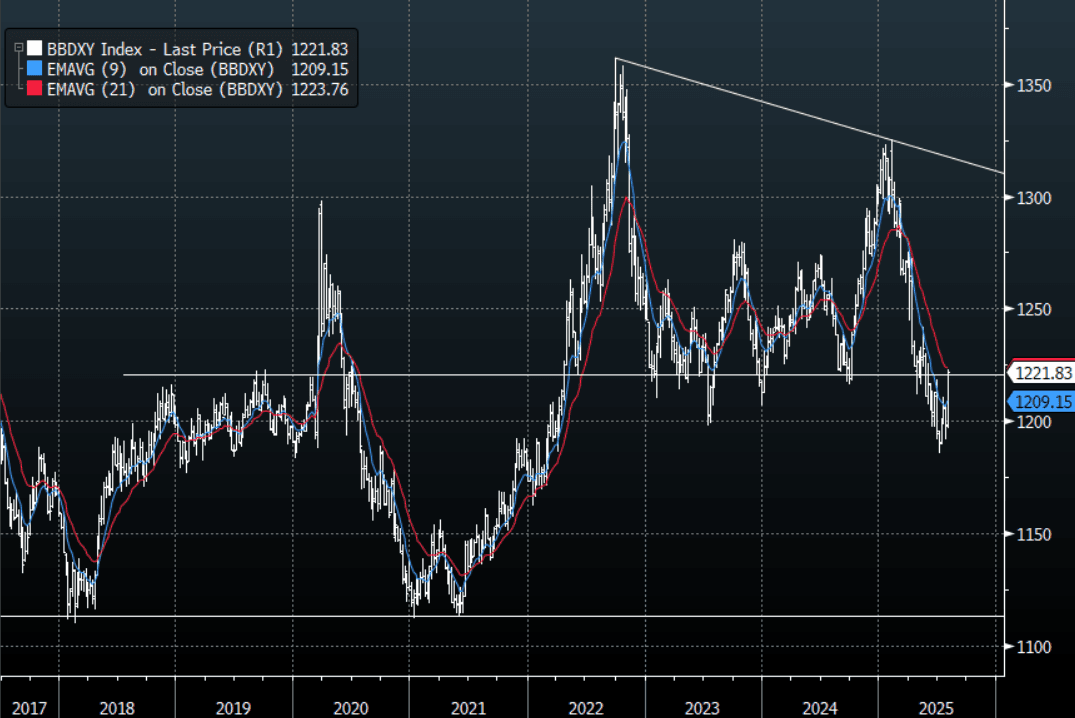

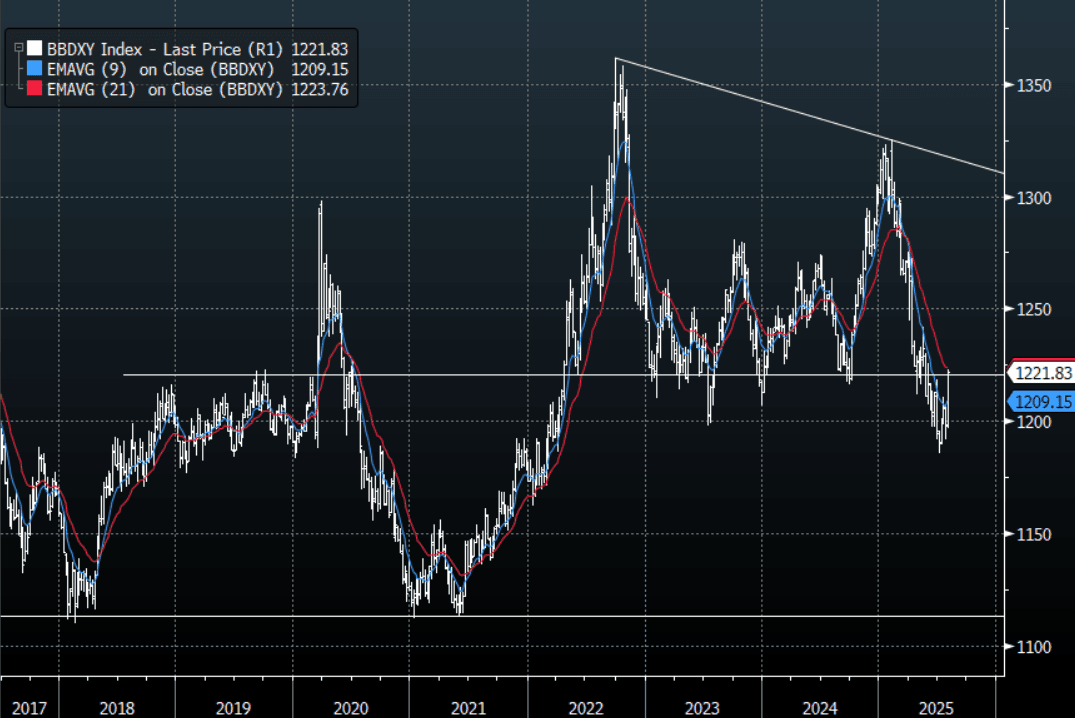

Fig 1: USD BBDXY Index

Source: Bloomberg Finance L.P./MNI

UK

ECONOMY (BBG): "British executives are less confident in the UK’s economic prospects than when the country shut down during the pandemic, a new survey showed, suggesting that the government has lost the support of the business community."

EU

SWITZERLAND (BBG): “Donald Trump will impose a 39% tariff on imports from Switzerland, leaving the European country with one of the steepest levies globally as the US president seeks to cut America’s trade deficit and lure manufacturing to its shores. “

UKRAINE (RTRS): "President Volodymyr Zelenskiy restored the independence of Ukraine's two main anti-corruption agencies on Thursday, moving to defuse a political crisis that has shaken faith in his wartime leadership and worried Western partners."

US

TARIFFS (BBG): “President Donald Trump announced a slew of new tariffs, including a 10% global minimum and 15% or higher duties for countries with trade surpluses with the US, forging ahead with his turbulent effort to reshape international commerce.”

US/CANADA (RTRS): “U.S. President Donald Trump intensified his trade war with Canada a day ahead of his August 1 deadline for a tariff agreement, saying it would be "very hard" to make a deal with Canada after it gave its support to Palestinian statehood. Trump is set to impose a 35% tariff on all Canadian goods not covered by the U.S.-Mexico-Canada trade agreement if the two countries do not reach an agreement by the deadline.”

BUSINESS CONDITIONS (MNI): The Chicago Business Barometer™ produced with MNI advanced 6.7 points to 47.1 in July. This was the largest increase in thirteen months, bringing the index to the highest since March 2025. However, the index has still been below 50 for twenty consecutive months.

TECH (RTRS): “Apple forecast revenue for the current quarter ending in September well above Wall Street’s estimates on Thursday, sending shares up despite a warning from CEO Tim Cook that U.S. tariffs would add $1.1 billion in costs over the period.”

CORPORATE (RTRS): “Amazon.com on Thursday forecast third-quarter sales above market estimates, but failed to live up to lofty expectations for its Amazon Web Services cloud computing unit after rivals handily beat Wall Street forecasts.

OTHER

JAPAN (BBG): “Japan’s Finance Minister said he’s worried by movements in the yen, which weakened to levels last seen in March following dovish messaging on interest rates from the Bank of Japan.”

JAPAN (MNI BRIEF): Japan’s economy is expected to have expanded in the April-June quarter, marking the first rise in two quarters, supported by solid private consumption and a positive contribution from net exports, though capital investment likely slowed, according to private economists.

NEW ZEALAND (BBG): "New Zealand will push for a reduction in the 15% tariff rate imposed on its exports to the US by President Donald Trump, Trade Minister Todd McClay said."

CHINA

POWER (MNI): A Chinese energy policy advisor provides insight into summer power demand.

MANUFACTURING (MNI BRIEF): China's S&P manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 49.5 in July, up from June's 50.4, falling back into the contraction zone below the 50 mark, as factory output scaled back amid a slower increase in new orders, the company said on Friday.

ECONOMY (CFLP): China’s July PMI showed the economy continues to face downward pressure, according to Zhang Liqun, analyst at the China Federation of Logistics and Purchasing, after the index reached 49.3%, down 0.4 percentage points from the previous month and below the boom and bust line for four consecutive months.

CONSUMPTION (SECURITIES TIMES): “The National Development and Reform Commission will intensify efforts to stabilise investment and promote consumption in the second half, with pledges to enhance the "full-cycle" management of government investment projects and stimulate the vitality of private investment, Securities Times reported, citing a recent announcement from the central planner.”

CAPITAL MARKETS (ECONOMIC INFORMATION DAILY): “Capital market analysts expect additional policy support and incremental funds after the Politburo called for measures to ensure the capital market's stability and consolidate recent upward momentum, Economic Information Daily reported, citing analysts.”

MNI: Central Bank Withdraws CNY663.3bn via OMO:

- The PBOC issued CNY126bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY789.3bn

- Net liquidity withdrawal CNY663.3bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.41%, from prior close of 1.55%.

- The China overnight interbank repo rate is at 1.32%, from the prior close of 1.20%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.55%.

MNI: PBOC Sets Yuan Parity Higher At 7.1496 Fri; -0.13% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1496 on Friday, compared with 7.1494 set on Thursday. The fixing was estimated at 7.2054 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND JULY ANZ CONSUMER CONFIDENCE INDEX 94.7; PRIOR 98.8

NEW ZEALAND JUNE BUILDING PERMITS M/M -6.4%; PRIOR 10.3%

AUSTRALIA JULY F S&P GLOBAL PMI MFG 51.3; PRIOR 51.6

AUSTRALIA Q2 PPI Q/Q 0.7%; PRIOR 0.9%

JAPAN JUNE JOBLESS RATE 2.5%; MEDIAN 2.5%; PRIOR 2.5%

JAPAN JUNE JOB-TO-APPLICANT RATIO 1.22; MEDIAN 1.25; PRIOR 1.24

JAPAN JULY F S&P GLOBAL PMI MFG 48.9; PRIOR 48.8

CHINA JULY S&P GLOBAL PMI MFG 49.5; MEDIAN 50.2; PRIOR 50.4

SOUTH KOREA JULY EXPORTS Y/Y 5.9%; MEDIAN 5.1%; PRIOR 4.3%

SOUTH KOREA JULY IMPORTS Y/Y 0.7%; MEDIAN 2.0%; PRIOR 3.3%

SOUTH KOREA JULY TRADE BALANCE $6610MN; MEDIAN $5700MN; PRIOR $9082MN

SOUTH KOREA JULY S&P GLOBAL PMI MFG 48.0; PRIOR 48.7

MARKETS

US TSYS: Asia Wrap - Yields End Mixed In A Quiet Session

The TYU5 range has been 110-29 to 111-00+ during the Asia-Pacific session. It last changed hands at 110-30+, down 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.947%, down 0.01 from its close.

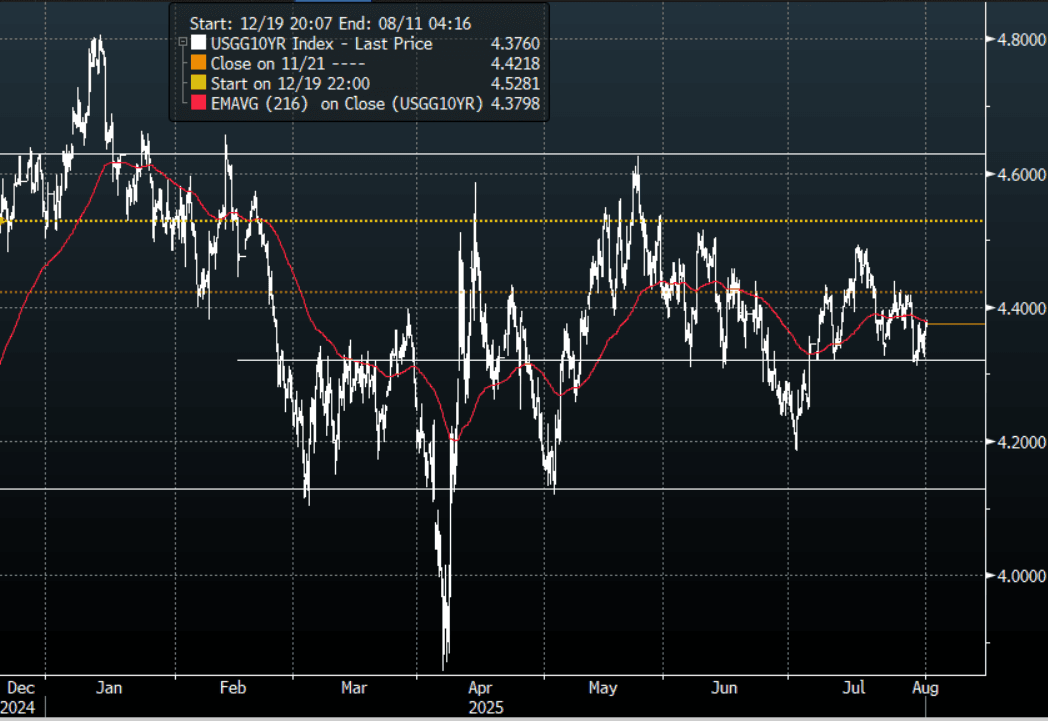

- The US 10-year yield has edged higher trading around 4.376%.

- The 10-year yield has again held the support around its pivot within the wider range 4.10% - 4.65%, decent supply was seen around the 4.30/35% area once more. This would need to clear above the 4.45% area to potentially regain upward momentum now.

- Bob Elliott on X: ”The combination of higher inflation and slowing wage growth is set to put even more of a squeeze on household consumption ahead and with it a weakening broader economy.”

- Nick Timiraos on X: “Core goods inflation is adding around 0.34 pp to core PCE inflation above the average contribution from the decade before the pandemic. Shelter is adding around 0.23 pp above the pre-pandemic trend. Remember, the pre-pandemic trend was below 2%, so not everything needs to go back to the pre-pandemic trend to hit 2%, but the disinflation in services is now being offset by the inflation in goods.”

- Robin Brooks on X: “The tariff inflation impulse to CPI and PCE is clear to see for stuff we import from China: furnishings and recreational goods. Monthly inflation is 100 - 120 bps above where it normally would be around this time of year. That's a massive inflation shock…”

- Data/Events: NFP, S&P Global Man PMI, ISM Manufacturing, Construction Spending, U. of Mich. Sentiment

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Subdued Session Ahead Of Payrolls, Tariff Uncertainty Remains

JGB futures are stronger but well off Tokyo session bests, +5 compared to the settlement levels.

- Yesterday, Governor Ueda stressed that underlying inflation remains below target and emphasised the need for more data to assess the full impact of 15% U.S. tariffs on Japan’s economy.

- The BoJ revised up its FY2025 growth and inflation forecasts modestly, expecting improvements in wage growth and activity later in the fiscal year, while warning of near-term headwinds from global demand and trade frictions.

- Although some speculate an October hike is possible post-political uncertainty, the BoJ is likely to wait until early 2026, seeking clearer evidence of wage-driven inflation and minimal tariff disruption. See full MNI BoJ Review here

- Cash US tsys are slightly mixed, with a steepening bias, in today’s Asia-Pac session. Today’s US calendar will see: NFP, S&P Global Man PMI, ISM Manufacturing, Construction Spending, U. of Mich. Sentiment.

- Cash JGBs are slightly richer out to the 20-year, but 1-2bps cheaper beyond. The benchmark 10-year yield is 0.6bp lower at 1.551% versus the cycle high of 1.616%.

- The swaps curve has twist-steepened, with rates 1bp lower to 2bps higher, pivoting at the 20-year.

- On Monday, the local calendar will see Monetary Base data.

AUSSIE BONDS: Cheaper Ahead Of US Payrolls

ACGBs (YM -5.0 & XM -5.0) are weaker after today’s domestic data drop and ahead of tonight’s US Payrolls release. Cash US tsys are slightly mixed, with a steepening bias, in today’s Asia-Pac session

- (DJ via BBG) "Australian house prices posted a sixth consecutive monthly rise in July, supported by ongoing speculation that the Reserve Bank of Australia will deliver further interest-rate cuts through the second half of the year. The home value index rose 0.6% in July from June, according to property research group Cotality, with the strongest growth reported in Brisbane, Perth and Adelaide."

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at -7bps.

- The bills strip has bear-steepened, with pricing -2 to-6.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given a 97% probability, with a cumulative 57bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- On Monday, the local calendar will see Melbourne Institute Inflation.

- Next week, the AOFM plans to sell A$300mn of the 4.25% 21 June 2034 bond on Tuesday, A$900mn of the 4.25% 21 March 2036 bond on Wednesday and A$1000mn of the 3.00% 21 November 2033 bond on Friday.

BONDS: NZGBS: Typical Subdued Pre-US Payrolls Friday Session

NZGBs closed little changed, with benchmark yields flat to 1bp higher, after a subdued pre-US payrolls Friday session.

- (Bloomberg) -- Smaller economies including New Zealand, Costa Rica and Bolivia saw US import tariffs rise to 15% — up from the 10% baseline released on April 2 — as part of a sweeping effort to penalize countries running trade surpluses with the US.

- Cash US tsys are slightly mixed, with a steepening bias, in today’s Asia-Pac session.

- Today’s US calendar will see: NFP, S&P Global Man PMI, ISM Manufacturing, Construction Spending, U. of Mich. Sentiment.

- Swap rates closed 1bp lower to 1bp higher, with a steeper 2s10s curve.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 34bps by November 2025.

- On Monday, the local calendar will be empty, ahead of Commodity Prices on Tuesday, and the Q2 Employment Report and House Prices on Wednesday.

FOREX: Asia FX Wrap - The USD Probing Pivotal Resistance Going Into NFP

The BBDXY has had a range of 1220.89 - 1223.02 in the Asia-Pac session, it is currently trading around 1222, +0.02%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Monday’s US-EU trade deal was seen as a big loss for the European Union and this provided the USD bounce with further tailwinds. A higher than expected PCE print overnight reinforced the hawkish tone from Powell and added to the USD’s tailwinds and to the shorts woes. The market is testing the pivotal 1220/30 area this morning, a sustained break of which could signal a deeper correction potentially back to the 1250 area. The market will now be gearing up for the NFP print tonight which could add further momentum to the move or help put a top in.

- EUR/USD - Asian range 1.1405 - 1.1429, Asia is currently trading 1.1420. The pair has found some demand around its first support for now. The pair is very quickly testing the important 1.1300/1.1400 area, where I would expect demand first up. When a market that is this long sees a move that quick it cannot reduce so initially bounces should now find sellers. The Long-term support looks to be towards the 1.1100 area where I would expect to find fresh buyers.

- GBP/USD - Asian range 1.3190 - 1.3216, Asia is currently dealing around 1.3195. This pair looks like it is now breaking lower indicating a deeper correction. Price has moved very quickly back towards the 1.3100/1.3200 support where I would expect demand first up, look for supply now on bounces back towards 1.3400.

- USD/CNH - Asian range 7.2058 - 7.2218, the USD/CNY fix printed 7.1496, Asia is currently dealing around 7.2150. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.20%, Gold $3290, US 10-Year 4.378%, BBDXY 1221, Crude Oil $69.47

- Data/Events : Spain Man PMI, Italy Man PMI/ Retail Sales, France Man PMI, Germany Man PMI, EZ Man PMI/CPI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

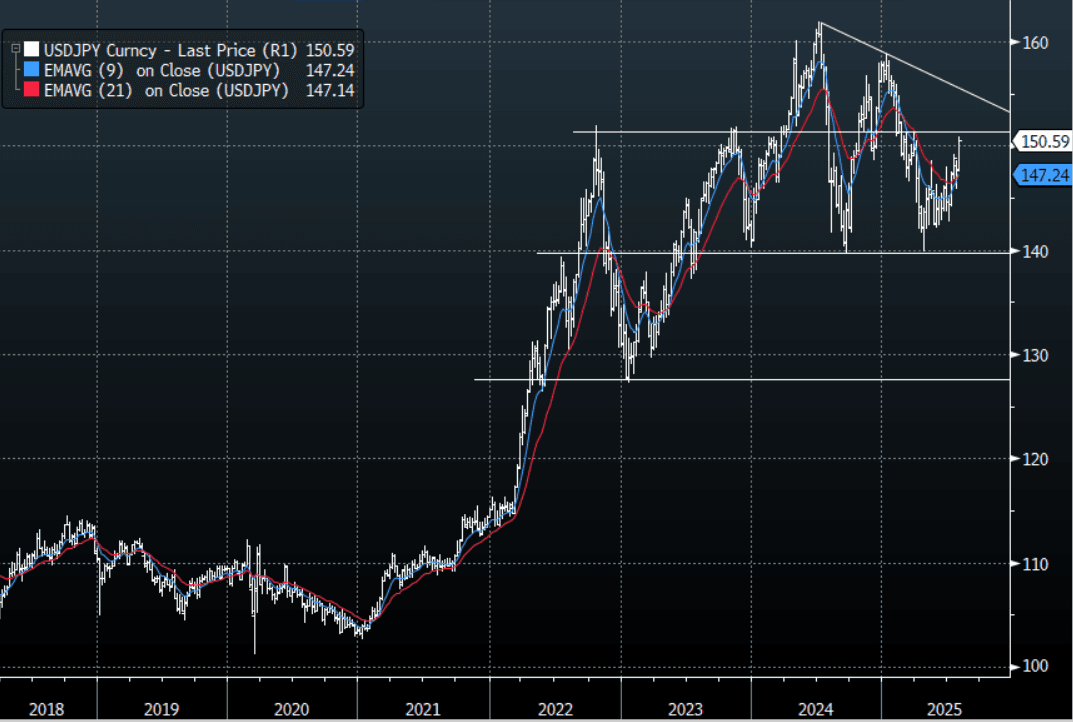

JPY: Asia Wrap - USD/JPY Pauses Towards 151.00, Officials Begin Jawboning

The Asia-Pac USD/JPY range has been 150.55 - 150.92, Asia is currently trading around 150.60, -0.10%. The JPY tried to rally on the inflation outlook being raised by the BOJ, but when Ueda spoke later he offered no clear idea of when the next rate hike would be. This saw the dip lower in USD/JPY be short-lived and its momentum higher resumed, the USD continued to grind higher adding to the pairs tailwinds. Price has moved quickly to now be testing its pivotal 151.00/152.00 area, I would expect some supply here first up but a sustained break above here would be a real worry for an institutional market that is still long JPY. The BOJ would also not be happy if this area does break as it would signal a potential move back to the area they have been defending 155-160.

- "JAPAN LABOUR MINISTRY COUNCIL EYES ABOUT 6% HIKE NATIONWIDE IN FY2025 AVERAGE MINIMUM WAGES, BIGGEST RISE EVER, KYODO SAYS - [RTRS]"

- (Bloomberg) - “Japan’s Finance Minister said he’s worried by movements in the yen, which weakened to levels last seen in March following dovish messaging on interest rates from the Bank Of Japan. “The government is deeply concerned about trends in the currency market, including speculative movements” Kato told reporters.”

- Earlier data showed mixed June labor market conditions. The unemployment rate was steady at 2.5%. This was in line with market forecasts. The unemployment rate has been steady at 2.5% since March of this year. This is just up from cycle lows of 2.4%. However, the job to applicant ratio rose fell to 1.22 from 1.24 prior, which was also below the 1.25 consensus expectation. This is the lowest job-to-applicant ratio since 2022.

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($1.16b), 147.00($1.62b).Upcoming Close Strikes : 150.00($1.04b Aug 4) - BBG.

- CFTC data shows last week Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

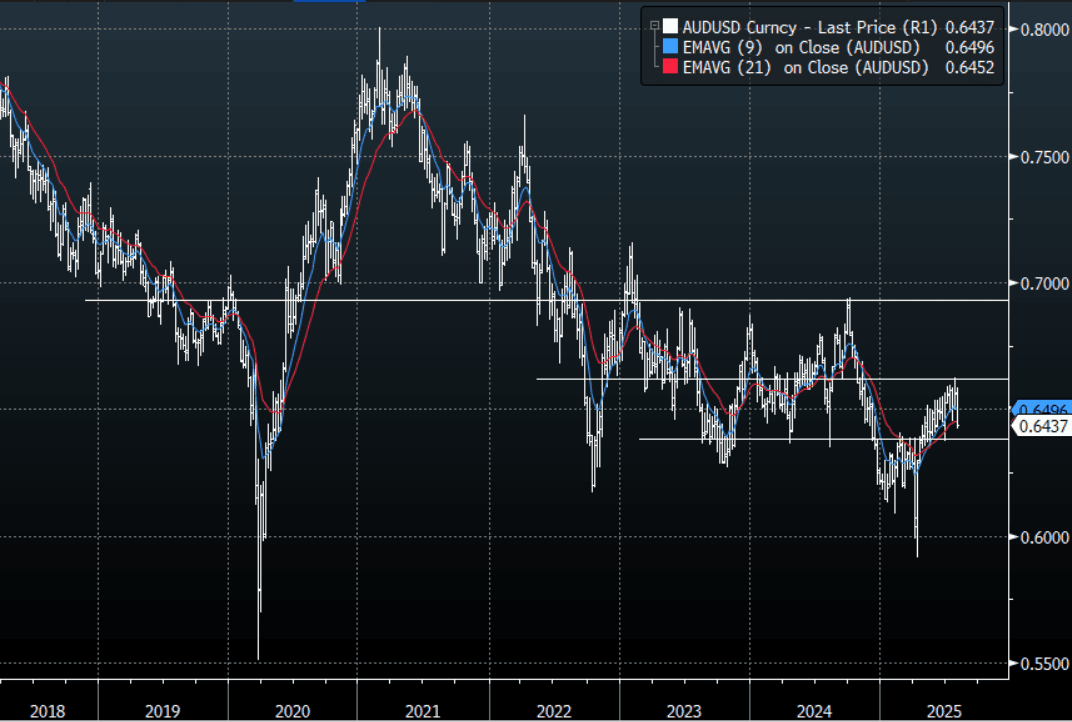

AUD: Asia Wrap - AUD/USD Retraces A Little Going Into NFP

The AUD/USD has had a range of 0.6422 - 0.6440 in the Asia- Pac session, it is currently trading around 0.6435, +0.17%. The momentum higher in risk could not be maintained overnight and a higher than expected PCE print overnight brought the hawkish tone of the Fed back into view. This saw the early AUD/USD rally stall and quickly move lower again. That looks like a very poor Daily close for US Stocks and could signal its time for risk to take a breather which opens the possibility of some reversion back to the mean. Should this unfold it will add to the AUD/USD headwinds being faced by a resurgent USD. The 0.6350 area is very important and a sustained move below that level should get the bears excited again as momentum would turn lower. The market will now be gearing up for the NFP print tonight which could add further momentum to the move or help put a base in.

- "AUSTRALIA 2Q PRODUCER PRICES RISE 0.7% Q/Q (prior 0.9%), AUSTRALIA 2Q PRODUCER PRICES RISE 3.4% Y/Y(prior 3.7%) " - BBG

- (Bloomberg) -- Australian home prices climbed for a sixth straight month with every major city reporting gains, while signs of resurgent rents are set to stretch the budgets of households in this segment.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD374m). Upcoming Close Strikes : 0.6000(AUD1.31b Aug 5), 0.6600(AUD847m Aug 5) - BBG

- AUD/JPY - Asia-Pac range 96.79 - 97.06, Asia is trading around 96.95. The pair has bounced nicely off its support around 96.00 and is again testing the recent tops above 97.00 this morning. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. With risk having a huge reversal lower overnight and opening soft this morning you would be forgiven for thinking this pair should be finding some headwinds and potentially drift lower. JPY longs are being squeezed and this is overriding everything.

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

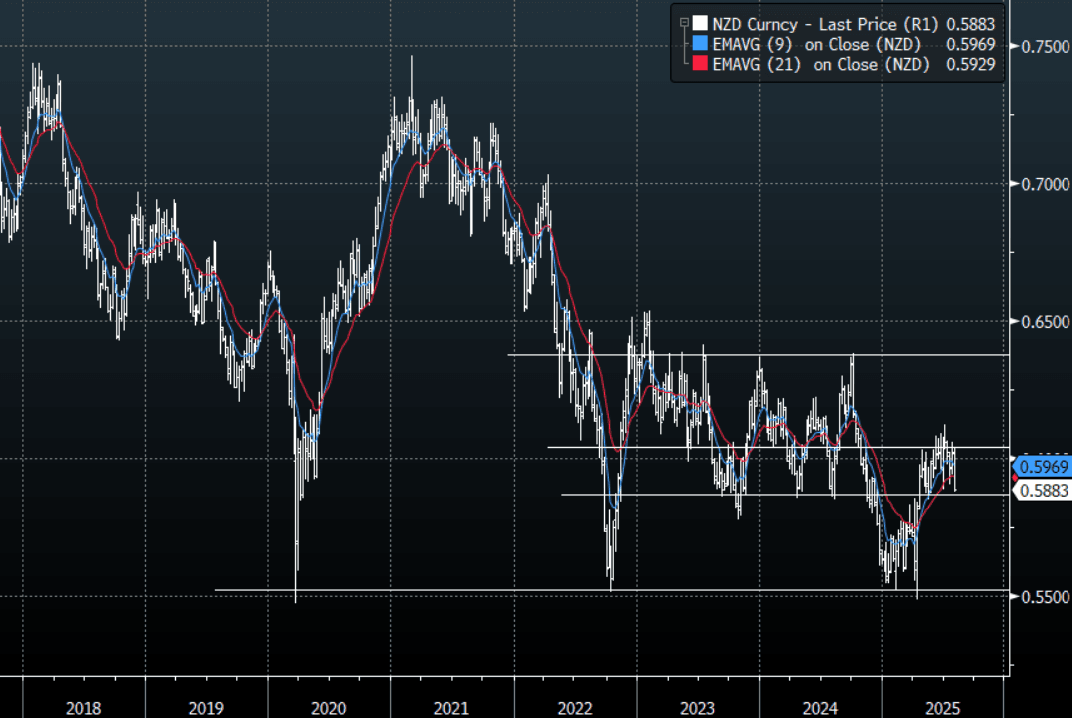

NZD: Asia Wrap - NZD/USD Remains Heavy Going Into NFP

The NZD/USD had a range of 0.5874 - 0.5901 in the Asia-Pac session, going into the London open trading around 0.5885, -0.10%. The momentum higher in risk could not be maintained and a higher than expected PCE print overnight brought the hawkish tone of the Fed back into view. This saw the early NZD/USD rally stall and quickly move lower again. That looks like a very poor Daily close for US Stocks and could signal its time for risk to take a breather which opens the possibility of some reversion back to the mean. Should this unfold it will add to the NZD/USD headwinds being faced by a resurgent USD. The 0.5800/50 area looks to be pivotal and a sustained break below could signal momentum is set to turn lower. The market will now be gearing up for the NFP print tonight which could add further momentum to the move or help put a base in.

- "NZ JUNE HOME-BUILDING APPROVALS FALL 6.4% M/M (prior +10.4%m/m) - BBG

- NEW ZEALAND ANZ Consumer Confidence Down In July, Inflation Expectations Up : The New Zealand ANZ consumer confidence index fell by 4.1% in July, putting the index back at 94.7 (prior was 98.8). The trend in consumer sentiment since the start of the year has largely been sideways. The index peaked around 100.0 at the end of last year, after trending up from lows of 82 from earlier in the year. Since late 2021, the index has spent no time above the 100.0 level.

- Kelly Eckhold(Westpac NZ) on LinkedIn: “The reciprocal tariff list is out and New Zealand got lifted to 15%. Australia was left at 10% so we lose some ground compared to them there. Not great news. Although interesting to note that generally our Asian trading partners rates got revised down from the 20s to 19%. Hence the direct impact on NZ is greater but the indirect impacts smaller. The indirect impacts are the main game here.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5375(NZD330m Aug 6). - BBG

- AUD/NZD range for the session has been 1.0905 - 1.0944, currently trading 1.0940. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Kospi Slumps Over 3%, China Vows To Curb Disorderly Competition

Most major Asia Pac indices are lower, although there are pockets of strength in parts of South East Asia. US equity futures are down modestly after mixed late earnings on Thursday US time (better for Apple, while Amazon disappointed). Broader US equity sentiment looks a little shakier, after what looked like a key day reversal on Thursday. Markets are also digesting the reciprocal tariff announcements from the US. South Korean markets are the weakest performers, down over 3%.

- China and Hong Kong markets are down modestly at this stage, the CSI 300 off 0.25% to 4065, following a sharp fall yesterday. The SHI was last near 24728, off 0.20%. Headlines have crossed from China's NDRC, which has vowed to regulate disorderly competition in the economy. This has become a key focus point for policy makers. The NDRC also stated that the fourth tranche of support for consumers (via the trade in program), will be allocated in Oct. NDRC also stated it will provide support for jobs and domestic when needed (per BBG). Earlier, the S&P Mfg PMI fell more than expected and is now back in contraction territory.

- The Kospi has fallen over 3%, putting the index back near3135, with sentiment weighed by tax changes. BBG notes :"The threshold for capital gains tax on stock holdings would drop to 1 billion won ($714,250) from 5 billion won and the transaction tax would increase, according to proposals released by the finance ministry in Seoul on Thursday. Meanwhile, the top corporate tax rate would rise to 25% from 24%, reversing a cut by the previous administration." Offshore investors have sold over $500mn of local stocks today. Note from late May the Kospi was up over 25%, driving significant outperformance.

- The Taiex is down around 0.70% at this stage. Taiwan's reciprocal tariff rate of 20% is higher than Japan and South Korea's but the authorities have vowed to negotiate further.

- In South East Asia, Malaysia and Indonesia indices are up over 1%. For Indonesia we are still sub late July highs, while offshore investors have remained net sellers. Elsewhere, the tone is mostly softer, although losses are modest at this stage.

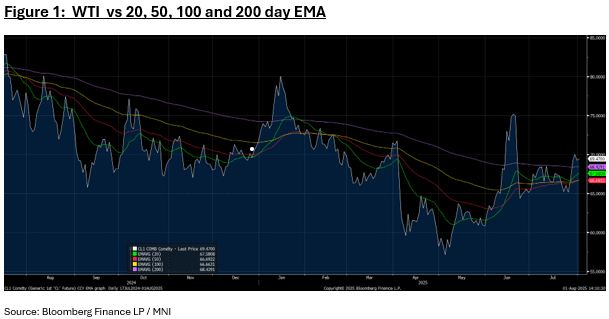

- Oil has had a strong week and is up in the Asia trading day today.

- WTI is up +0.30% today in Asia and over 6% for the week taking it back above all major moving averages.

- Brent is lower today by -0.85% but remains up over 5% for the week.

- Oil's attention is clearly on President Trump's threats against Moscow and an upcoming deadline for a truce in Ukraine.

- Trump has singled out India for buying Russian oil, a move that prompted the government to tell state owned refiners to search for new sources.

- With the tariff deadline here, Trump’s tariffs and any retaliatory measures from targeted countries will be the focus for oil markets in the coming days. The president signed an executive order that increases the rate on Canada to 35% from 25%, but kept in place an exemption for goods under the US-Mexico-Canada trade pact that includes oil.

- US gasoline, diesel and jet fuel demand in May were all markedly higher in the Energy Information Administration's monthly report compared to estimates published in the agency's Weekly Petroleum Status Report. Diesel demand climbed to 3.8 million barrels a day in May, about 6.5% higher than the weekly averages previously published by the agency, while demand for jet fuel was 5% higher and gasoline was 3% higher. (source BBG)

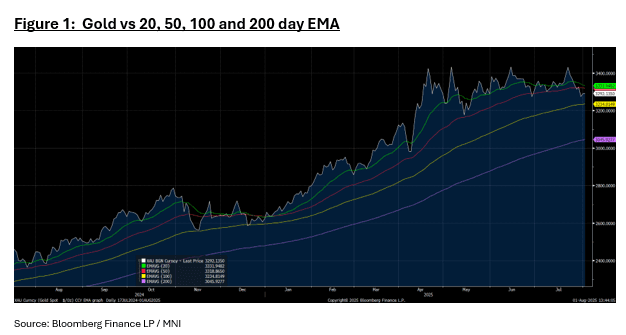

- Despite being up on four out of the five trading days this week, gold is set for a weekly decline.

- With the European and US trading sessions ahead, gold sits week to date down over 1 percent. It is up by a modest +0.10% in the Asia trading day at US$3,293.15.

- Tuesday saw the large down day which took gold below the 50-day EMA of $3,318.88, with the 100-day EMA of $3,234.82 below.

- Gold's modest gains have been supported by the unveiling of tariff rates from the US President which has announced a minimum global tariff of 10% while imports of countries with surpluses will be 15% or more.

- Gold finished it's best month of 2025 in July and could be set to trade within tight ranges in early August as the impact of the tariff announcements are assessed.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 01/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0800/1000 | * | Retail Sales | |

| 01/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/08/2025 | 0900/1100 | *** | HICP (p) | |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/08/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 01/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |