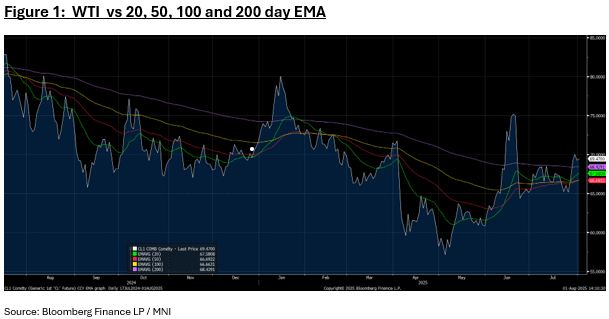

OIL: Oil Set For Large Weekly Gain

Aug-01 04:16

- Oil has had a strong week and is up in the Asia trading day today.

- WTI is up +0.30% today in Asia and over 6% for the week taking it back above all major moving averages.

- Brent is lower today by -0.85% but remains up over 5% for the week.

- Oil's attention is clearly on President Trump's threats against Moscow and an upcoming deadline for a truce in Ukraine.

- Trump has singled out India for buying Russian oil, a move that prompted the government to tell state owned refiners to search for new sources.

- With the tariff deadline here, Trump’s tariffs and any retaliatory measures from targeted countries will be the focus for oil markets in the coming days. The president signed an executive order that increases the rate on Canada to 35% from 25%, but kept in place an exemption for goods under the US-Mexico-Canada trade pact that includes oil.

- US gasoline, diesel and jet fuel demand in May were all markedly higher in the Energy Information Administration's monthly report compared to estimates published in the agency's Weekly Petroleum Status Report. Diesel demand climbed to 3.8 million barrels a day in May, about 6.5% higher than the weekly averages previously published by the agency, while demand for jet fuel was 5% higher and gasoline was 3% higher. (source BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

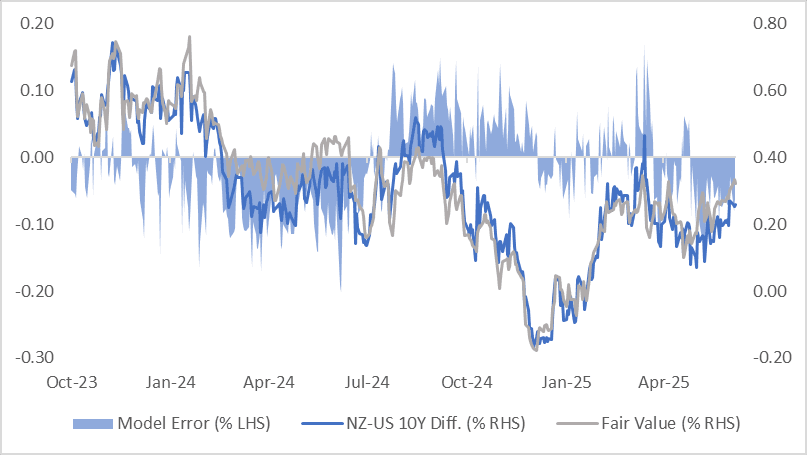

BONDS: NZ-US 10Y Differential In the Top Half Of This Year’s Range

Jul-02 04:12

NZGBs are richer today, with benchmark yields 2bps lower. The NZGB 10-year has slightly outperformed US 10-year since yesterday’s close, with the NZ-US yield differentials 2bps tighter on the day.

- At +25bps, the NZ-US 10-year differential is in the top half of the -20bp to +40bps range seen this year.

- A simple regression analysis of the 3-month forward swap rate spread (1Y3M) over the past 18 months indicates the 10-year yield differential is around 7bps below its estimated fair value of +32bps.

- Notably, the regression error has fluctuated within a range of ±15bps over the past year, highlighting some variability in the relationship.

- The 1Y3M differential continues to be a key driver of market expectations for long-term yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

CHINA: Bond Futures Strong as OMO Withdraws Liquidity

Jul-02 03:58

- China's bond futures rallied in the morning session as the Central Bank withdrew liquidity during the OMO.

- The 10yr future is up +.10 to 109.08, following on from yesterday's rally. The move sees the 10yr trade above the 20-day EMA of 108.99.

- The 2yr future +0.02 to 102.50 to trade through the 20-day EMA of 102.49 and approach the 50-day EMA of 102.51

- The 10YR government bond is lower in yield by -0.05bps at 1.64%

JGBS: Futures Slightly Weaker, Heavy US Calendar Before Long Weekend

Jul-02 03:39

In early afternoon trade, JGB futures weaker, -5 compared to the settlement levels, after reversing modest overnight gains.

- Japan’s monetary base fell 3.5 percent in June from a year ago.

- Japan’s super-long bonds are set to remain under pressure in the medium term as local life insurers may offload holdings to sidestep impairment losses on deeply discounted debt. (per BBG)

- (Bloomberg) -- Japan will continue actively negotiating tariffs in good faith with the US for both countries’ mutual benefit, Deputy Chief Cabinet Secretary Kazuhiko Aoki says at a regular press conference on Wednesday.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash JGBs are little changed across benchmarks out to the 10-year and ~1bp richer beyond. The benchmark 10-year yield is 0.5bp higher at 1.40% versus the cycle high of 1.596%.

- The swaps curve has twist-steepened, with rates 1bp lower to 1bp higher. Swap spreads are tighter out the 10-year and wider beyond.