MNI EUROPEAN OPEN: Not Necessary to Fire Powell

EXECUTIVE SUMMARY

- TRUMP SAYS 'NOT NECESSARY' TO FIRE POWELL - MNI

- THE EU BELIEVES THAT A TRADE DEAL WITH THE US IS 'WITHIN REACH.' - BBC

- BRITAIN AND INDIA SIGN A FREE TRADE AGREEMENT - RTRS

- FED-TREASURY ACCORD NEEDED ON DEBT TERM STRUCTURE - MNI

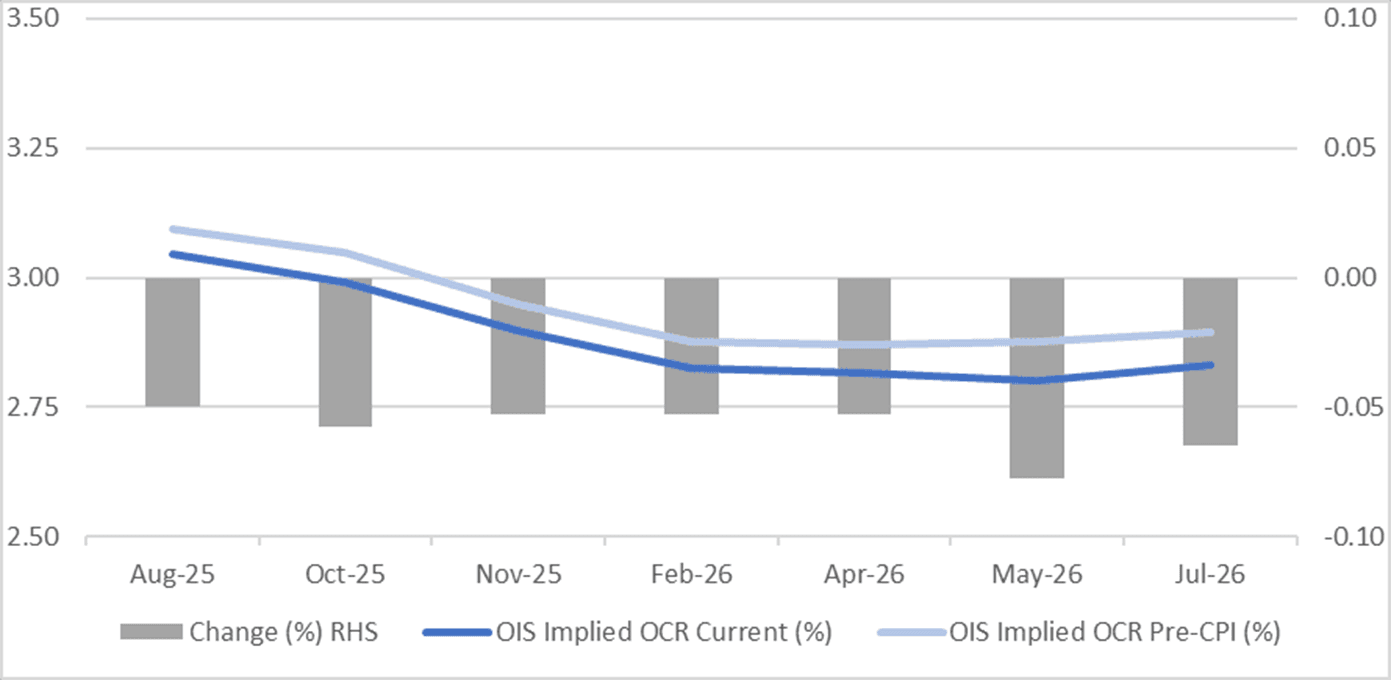

Fig 1: RBNZ-Dated OIS Holding Softer Than Pre-CPI Levels

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

Palestine (BBG) “UK Prime Minister Keir Starmer is facing pressure from senior members of his government and French President Emmanuel Macron to imminently recognize Palestine as a sovereign state due to the worsening humanitarian crisis in Gaza. “

India Trade Deal (RTRS)): “ Britain and India signed a free trade agreement on Thursday during a visit by Indian Prime Minister Narendra Modi, sealing a deal to cut tariffs on goods from textiles to whisky and cars and allow more market access for businesses. Talks on the trade pact were concluded in May after three years of stop-start negotiations, with both sides hastening efforts to clinch a deal in the shadow of tariff turmoil unleashed by U.S. President Donald Trump.”

AUKUS (BBG) “Australia and the UK will hold talks between their foreign and defense ministers in Sydney on Friday, with the aim of signing a £20 billion ($27 billion) “treaty” to help build nuclear-powered submarines. The annual meeting is part of the Australia-United Kingdom Ministerial Consultations (AUKMIN). Australian Defence Minister Richard Marles and Foreign Minister Penny Wong will host UK Foreign Secretary David Lammy and Defence Secretary John Healey. They are due to hold a news conference at Admiralty House on Sydney harbor after their talks.”

EU

Trade Deal Within Reach (BBC). “The European Union has said it believes a deal on trade tariffs with the US is "within reach", ahead of a 1 August deadline when President Donald Trump has threatened to impose a sweeping 30% levy on EU imports. Hopes were raised after EU diplomats suggested the US had proposed a broad 15% tariff on most European imports. A European Commission spokesman refused to speculate on the latest talks on Thursday, but said EU negotiators were working "might and main" to deliver a deal for Europe's consumers and companies. White House spokesman Kush Desai said earlier that any talk about deals should be seen as "speculation" unless it was confirmed by the president.”

US

MNI BRIEF: Trump Says It's Not Necessary To Fire Fed's Powell. President Donald Trump on Thursday said it's not necessary to fire Federal Reserve Chair Jerome Powell before his term as leader ends in May, adding that he is considering two or three names to potentially next lead the central bank.

MNI INTERVIEW: Fed-Treasury Accord Needed On Debt - Cochrane. The Treasury and the Federal Reserve need a new accord specifying who is in charge of the maturity structure of government debt, John Cochrane, a senior fellow at the Hoover Institution and former Fed adviser, told MNI. "One place where I do think there needs to be a better accord is on the maturity structure," he said in an interview. "We certainly need to get it straight who's in charge of the maturity structure."

JP

MNI BRIEF: Japan July Tokyo Core CPI Rises 2.9% Vs. June 3.1%. the Tokyo core inflation rate decelerated to 2.9% y/y in July, from June’s 3.1%, but stayed above 2% for the ninth straight month, data from the Ministry of Internal Affairs and Communications showed on Friday.

MNI BRIEF: Japan June Services PPI Rises 3.2% Vs. May 3.4%. Japan’s services producer price index (SPPI) rose 3.2% y/y in June, decelerating from May’s revised 3.4%, despite the continued increase in corporate pass-through cost, preliminary data released by the Bank of Japan showed on Friday.

CHINA

MNI China Press Digest July 25: Minerals, Meituan, Competition

MNI BRIEF: EU-China Summit Beat Expectations - Chamber. The results of the EU-China Summit held on Thursday in Beijing have exceeded the expectations of the European Chamber of Commerce in China, the chamber's president Jens Eskelund said in an online statement on Friday.

MNI: PBOC Net Injects CNY601.8 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY789.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY601.8 billion after offsetting maturities of CNY187.5 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.5793% at 10:00 am local time from the close of 1.5759% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Thursday, compared with the close of 53 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1419 Fri; +1.00% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1419 on Friday, compared with 7.1385 set on Thursday. The fixing was estimated at 7.1630 by Bloomberg survey today.

MARKET DATA

JAPAN TOKYO CPI YOY JULY 2.9%; EST 3.0%, PRIOR 3.1% YoY.

JAPAN TOKYO CPI EX-FRESH FOOD YOY JULY 2.9%; EST. 3.0%, PRIOR 3.0%,

JAPAN CPI EX-FRESH FOOD, ENERGY YOY JULY 3.1%, EST 3.1%, PRIO 3.1%

PPI SERVICES YoY JUNE 3.2%, EST 3.2%, PRIOR 3.4% (REVISED)

JAPAN LEADING INDEX CI MAY F 104.8; PRIOR 105.3

JAPAN COINCIDENT INDEX MAY F 116.0; PRIOR 115.9

JAPAN NATIONWIDE DEPT SALES YOY JUNE

JAPAN TOKYO DEPARTMENT SALES YOY JUNE

MARKETS

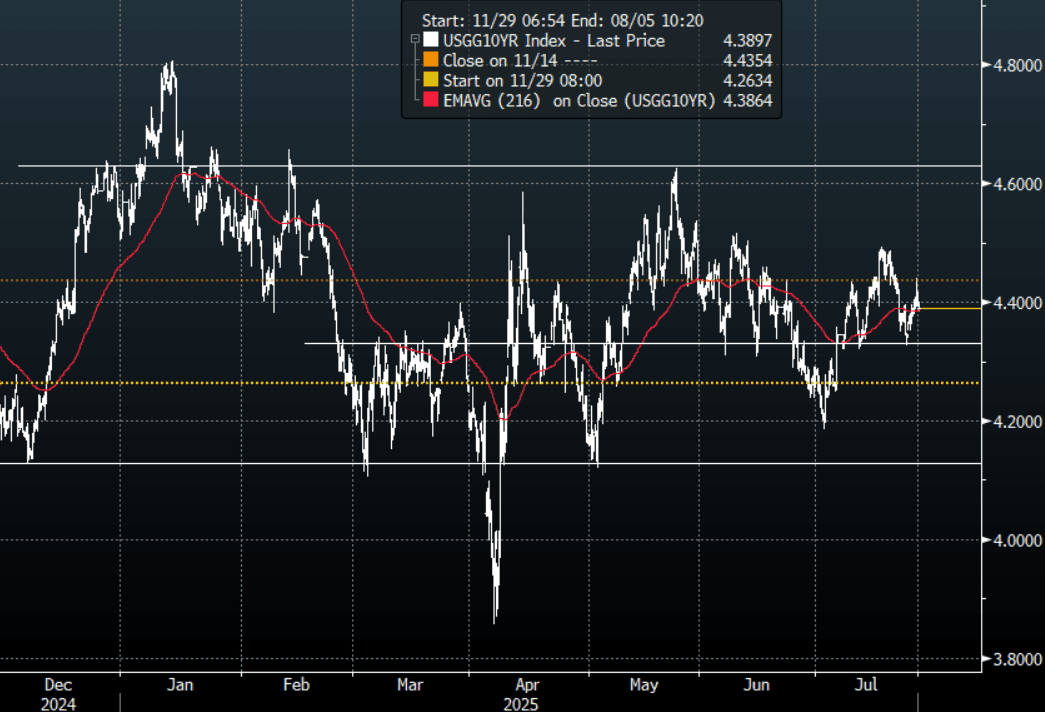

US TSYS: Asia Wrap - Yields Edge Slightly Lower

The TYU5 range has been 110-28 to 110-30+ during the Asia-Pacific session. It last changed hands at 110-29+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.912%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.39%, up 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A decent bounce off its support but the move failed to follow through above 4.40% overnight.

- Wei Li(CIS BLockRock) on LinkedIn: “Lower Fed policy rate does not always translate into lower long rates, this year's case in point. A number of factors explain the gap, list not exhaustive but all relevant this year: Fiscal trajectory; Investor appetite including international investors; Higher inflation premium: core service inflation volatility is twice the long term levels reflecting greater macro uncertainty. I continue to prefer the front and belly of the curve for income.”

- (Bloomberg) - “Donald Trump said he didn’t see the need to fire Jerome Powell, making it clear he saw lowering rates as a more pressing concern. The two publicly traded barbs over the Fed’s cost overruns during their tour of the project.”

- Bob Elliott on X: “With that performance today it's clear that there is no chance in hell Powell resigns before his chairmanship is up.”

- Data/Events: Durable Goods Orders, Kansas City Fed Services Activity

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bond Bull-Flattener To Close Out Week

JGB futures are stronger and hovering near session highs, +12 compared to settlement levels.

- Daily Chartbook on X: "Japan won't need to purchase as many Treasuries and other foreign bonds and stocks over the longer term after its trade deal with the US." @LondonSW via ZeroHedge.

- Taro Kimura, economist, said "Beneath the surface, cost pressures from earlier spikes in rice prices and rising labor expenses are still feeding through to costs of processed food and dining out," and the data should encourage the Bank of Japan to continue to raise rates gradually.

- (DJ via BBG) An early trade deal with the U.S. could put Bank of Japan's path towards monetary policy normalisation firmly back on track, according to HSBC economists in a research note.

- Cash US tsys are slightly richer in today's Asia-Pac session.

- Cash JGBs are showing a bull flattener across benchmarks, with yields flat to 6bps lower. The benchmark 10-year yield is 1.5bps lower at 1.591% versus the cycle high of 1.616%.

- Swap rates are 1-4bps lower, with a flatter curve. Swap spreads are mostly tighter.

- On Monday, the local calendar will be empty ahead of 2-year supply on Tuesday.

AUSSIE BONDS: Slightly Mixed After A Muted Session Of Trading

ACGBs (YM -0.5 & XM +1.5) are slightly mixed on a data-light session. The local calendar was empty today and will remain so until next Wednesday's Q2 CPI data.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest bear-flattener. Friday's US data, including Durable Goods Orders and Capital Goods Orders Nondef Ex Air, followed by the Kansas City Fed Services Activity.

- (Bloomberg) - "Donald Trump said he didn't see the need to fire Jerome Powell, making it clear he saw lowering rates as a more pressing concern. The two publicly traded barbs over the Fed's cost overruns during their tour of the project."

- Cash ACGBs are flat to 1bp richer with the AU-US 10-year yield differential -5bps.

- The bills strip is slightly weaker, with pricing -1 to -2.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in August is given a 94% probability, with a cumulative 57bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Next week, the AOFM plans to sell A$1000mn of the 2.25% 21 May 2028 bond on Tuesday and A$1200mn of the 2.75% 21 June 2035 bond on Friday.

BONDS: NZGBS: Closed On A Weak Note, Underperformed $-Bloc

NZGBs closed on a weak note, with benchmark yields 2-3bps higher.

- The RBNZ has updated its Kiwi-GDP nowcast for Q2, now estimating a 0.3% q/q contraction in GDP. The model has pointed to negative growth since early July, reflecting weakness across manufacturing, labour, and housing indicators. (BBG)

- NZGBs underperformed the $-Bloc, with the NZ-US and NZ-AU 10-year yield differentials 3-4bps wider on the day.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest bear-flattener. Friday's US data, including Durable Goods Orders and Capital Goods Orders Nondef Ex Air, followed by the Kansas City Fed Services Activity.

- Swaps finished showing a twist-flattener, with rates 2bps higher to 1bp lower.

- RBNZ dated OIS pricing closed slightly firmer across meetings. Nevertheless, pricing is 5-8bps softer across meetings versus Monday's pre-CPI levels. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- On Monday, the local calendar will see Filled Jobs data.

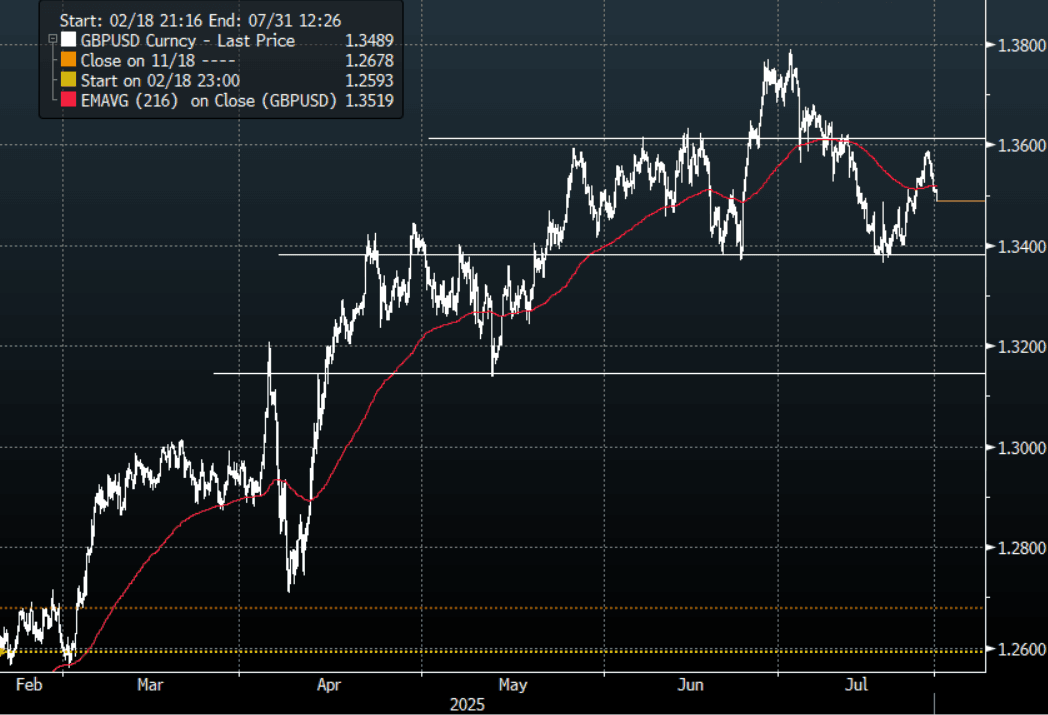

FOREX: Asia FX Wrap - The USD Slide Stalls Heading Into A Big Week For Risk

The BBDXY has had a range of 1195.23 - 1197.49 in the Asia-Pac session, it is currently trading around 1197, +0.16%. The USD’s slide lower finally stalled and some profit-taking was seen. There is lots of event risk coming up next week and we are heading into month-end so caution is warranted, this could potentially see some more paring back of USD shorts. “ECB officials pushing for a September cut are said to face tough odds after the central bank kept rates unchanged for the first time in about a year. Traders pared bets on further easing in 2025 after Christine Lagarde said policymakers are in “wait-and-see” mode amid US-EU tariff talks.”

- EUR/USD - Asian range 1.1734 - 1.1759, Asia is currently trading 1.1735. The pair’s upward momentum seems to be stalling towards 1.1800. The price looks a little stretched in the short term, but the USD is trading extremely poorly and the EUR will continue to be the main beneficiary.

- GBP/USD - Asian range 1.3487 - 1.3514, Asia is currently dealing around 1.3490. The support around 1.3350/1.3400 has proved to be solid first up. The pair could not build on its move higher and has drifted back to the middle of its recent range. While the support holds the market will be encouraged to continue to play from the long side.

- USD/CNH - Asian range 7.1511 - 7.1640, the USD/CNY fix printed 7.1419, Asia is currently dealing around 7.1650. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.19%, Gold $3359, US 10-Year 4.388%, BBDXY 1197, Crude oil $66.16

- Data/Events : France Consumer Confidence, EZ Survey Of Professional Forecasters & M3 Money Supply, Germany IFO, Italy Consumer & Manufacturing Confidence

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Extends Above 147.00

The Asia-Pac USD/JPY range has been 146.97 - 147.49, Asia is currently trading around 147.30, +0.17%. USD/JPY found good demand around 146.00 and has bounced nicely off its first support. Some demand for USD’s was finally seen as the market takes some risk off the table heading into next week which is filled with event risk and also month-end. The CFTC data showed the market is shifting its view on the JPY, with leverage funds just starting to build JPY shorts and Asset managers actively reducing their own. Price has managed a decent bounce off the 146.00 area, the question is can it now build on this ?

- WSJ - “Trump wants a deal, and China is willing to play ball.”

- Daily Chartbook on X: "Japan won’t need to purchase as many Treasuries and other foreign bonds and stocks over the longer term after its trade deal with the US." @LondonSW via ZeroHedge. See Graph Below.

- (Bloomberg) - "Tokyo's CPI rose 2.9% in July from a year earlier, slower than estimated. It’s the first time the pace of gains slipped below 3% since March. Still, food inflation stayed hot, keeping pressure on PM Shigeru Ishiba.”

- Taro Kimura, economist, said "Beneath the surface, cost pressures from earlier spikes in rice prices and rising labor expenses are still feeding through to costs of processed food and dining out," and the data should encourage the Bank of Japan to continue to raise rates gradually.

- “JAPAN'S MAEHARA: NOT THINKING ABOUT JOINING ISHIBA COALITION” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.16b),146.00($1.35b).Upcoming Close Strikes : 145.00($1.3b July 29), 145.00($982m July 28), 148.00($946m July 28) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

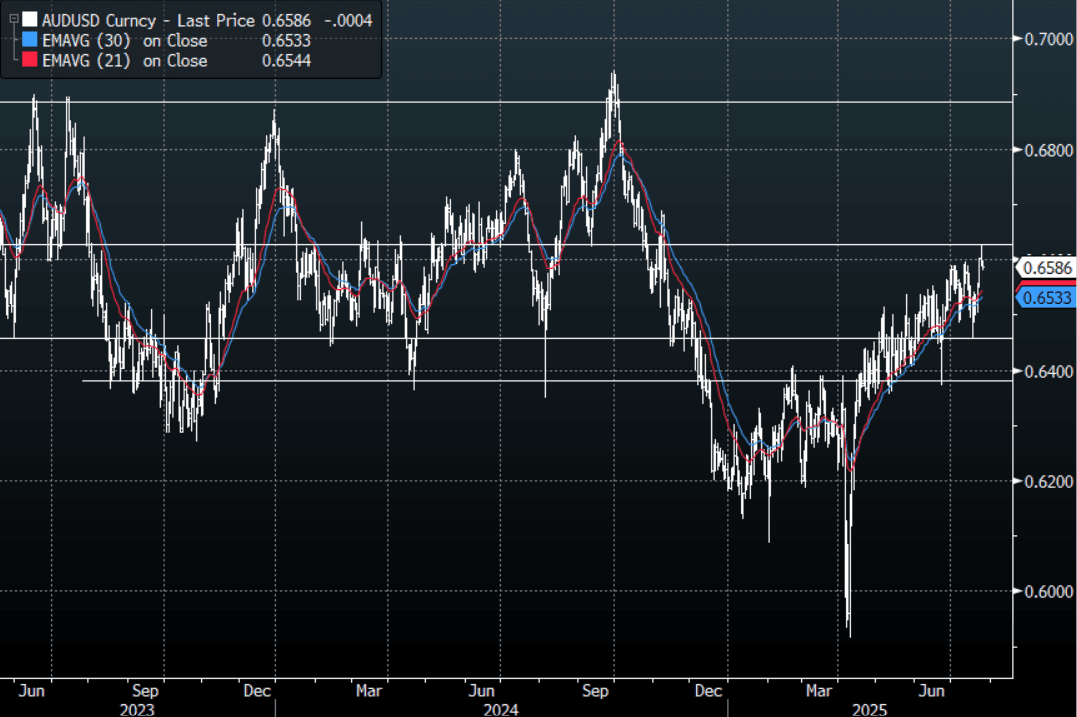

AUD: Asia Wrap - AUD/USD Drifts Lower

The AUD/USD has had a range of 0.6579 - 0.6599 in the Asia- Pac session, it is currently trading around 0.6582, -0.12%. The pair ran into some decent supply above 0.6600 and has drifted lower as the USD finally bounces. The pair is challenging the top of its recent range and a sustained move above 0.6600 could see it gain upward momentum, but there is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- WSJ - “Trump wants a deal, and China is willing to play ball.”

- (Bloomberg) -- “Australia and the UK will hold talks between their foreign and defense ministers in Sydney on Friday, with the aim of signing a £20 billion ($27 billion) “treaty” to help build nuclear-powered submarines.”

- (AFR) "In the new Reserve Bank regime, Bullock has limited opportunities to make policy speeches and so the Anika address was eagerly anticipated by economists and traders, most of whom were blindsided by the July call. Bullock made it clear that she is not all that fussed about guiding the market. But her message on Thursday is that the RBA intends to stick to its winning strategy of taking a slow and steady approach."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6450(AUD552m). Upcoming Close Strikes : 0.6600(AUD968m July29), 0.6600(AUD823m July 30), 0.6550(AUD704m July30) - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

- AUD/JPY - Today's range 96.87 - 97.14, it is trading currently around 96.95, +0.05%. The pair extended its move higher overnight. The support between 95.00 - 96.00 held as demand materialised first up, the pair is looking to regain its momentum for a move higher. The Event-risk of next week could provide some short-term headwinds.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

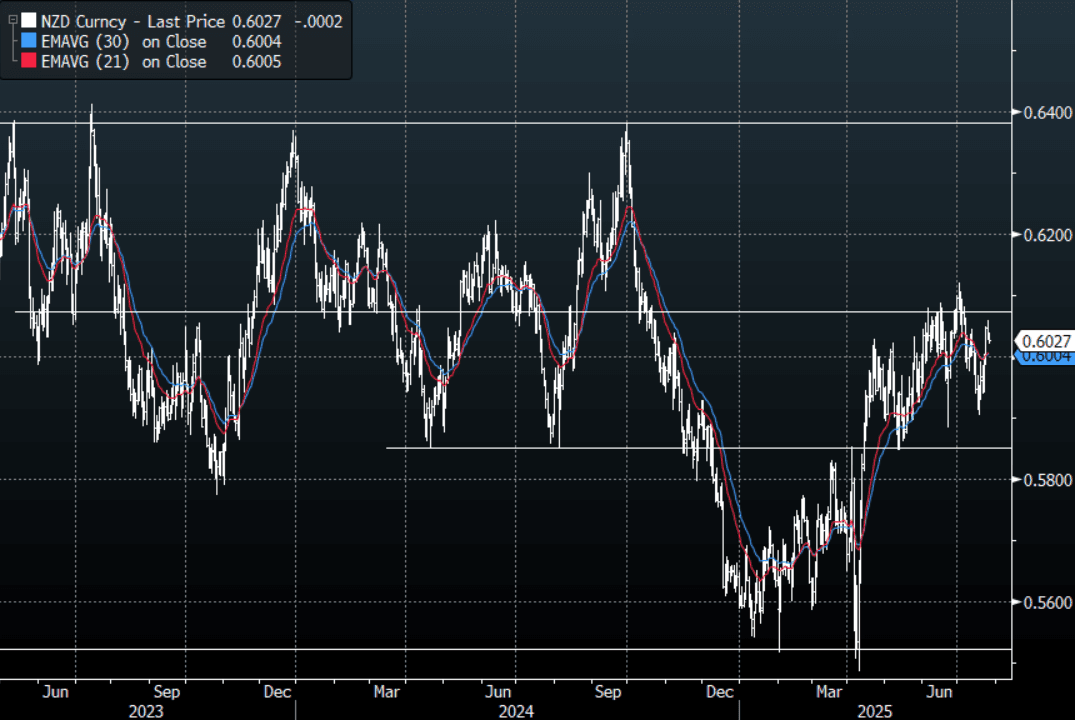

NZD: Asia Wrap - NZD/USD Drifts Back Towards 0.6000

The NZD/USD had a range of 0.6021 - 0.6039 in the Asia-Pac session, going into the London open trading around 0.6022, -0.12%. The pair ran into some decent supply around the 0.6050 area and has drifted lower as the USD finally finds some demand. Depending what your view is this 0.6050 area looks an attractive fade initially, the danger though is the USD which is looking sickly once more and should it capitulate the NZD could build momentum higher again. Price will need a sustained break back above the 0.6050/0.6100 area to signal a potential base might be in place. There is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- (Bloomberg) -- “Standard Chartered recommends buying the New Zealand dollar against the Swiss franc, calling it a clean way to position for continued improvement in global risk sentiment heading into the Aug. 1 US tariff deadline.”

- “Strategists including Steven Englander, head of global G-10 FX research at Standard Chartered, recommend going long NZD-CHF at 0.4796, with a target of 0.5150 and a stop-loss at 0.4680, expressing a tactical three-month view.”

- “We think the US is likely to conclude more trade deals with remaining holdouts such as Europe and Korea, following an agreement with Japan,” they wrote in a note. “Treasury Secretary Bessent also signalled an extension in US-China trade talks, reducing the probability of a re-escalation in trade tensions”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30). - BBG

- AUD/NZD range for the session has been 1.0916 - 1.0934, currently trading 1.0917. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Leads with Strong Weekly Returns

China's major bourses delivered strong weekly returns, despite falls on Friday. In a week dominated by new trade deal announcements and no key data from China, news that ETF purchases from the sovereign wealth fund and the announcement of a US / Japan trade deal was enough to get Chinese investors going.

- The Hang Seng is down today by -1.11%, but remains up +2.25% for the week. The CSI 300 is down -0.55% today but up +1.6% for the week. The Shanghai Comp lower by -0.35% today but higher by +1.6 for the week and Shenzhen is down -0.21% today but up over 2% for the week.

- The TAIEX in Taiwan has done very little this week, despite data showing that the ongoing inflows of FDI continued.

- The KOSPI had a modest week but its standard lately, up just +0.29% today and +0.37% for the week.

- The FTSE Malay KLCI fell -0.78% today and is barely holding onto a +0.16% gain for the week.

- The Jakarta Composite is lower by -0.14% today, but has added +2.85% for the week.

- The FTSE Straits Times in Singapore is up +1.4% for the week and the PSEi in the Philippines up +1.8%.

- The NIFTY 50 in India is lower by -0.57% to see it fall into the negative by -0.20% for the week.

OIL: WTI Finds Demand Towards $65.00, Trades Within Recent Ranges

The Asia-Pac overnight range for the CLU5(WTI) contract was $65.33 - $66.39, it is currently trading around $66.15 in the Asia-Pac session, +0.15%. WTI continues to find demand towards the $65.00 area as it consolidates within its recent $63 - $68 range. “(Bloomberg) -- Oil rose a second day on optimism over US trade talks ahead of next week’s deadline, and as tightness in diesel markets boosts sentiment.” - BBG

- Brent for September settlement is currently trading at $69.32 a barrel, +0.20%.

- Barchart on X: “U.S. Oil Production has now declined on a year-over-year basis for the first time since 2021.” Source: @dailychartbook. See Graph Below.

- (Bloomberg) - Oil may be at risk of a fresh leg lower as attention swivels back to OPEC+ and the alliance’s aggressive unwinding of production cuts. The group’s tap-loosening — a feature of the market for several months now — underpins concerns that global crude supplies will run ahead of demand into the year-end.

Fig 1: WTI Crude Future Hourly Chart

Source: MNI/@dailychartbook

Gold Clings to Modest Weekly Gain

- Gold's impressive start to the week is helping it hold onto modest gains for the week, after a third day of falls.

- Down -0.21% today, gold is at US$3,361.54, holding onto weekly gains of a mere +0.35%.

- Gold is holding its position barely above the 20-day EMA of $3356.25. Were it to break below, the next key level would be the 50-day EMA of $3,324.21.

- Any momentum that gold tried to build was taken out this week as the announcement of the trade deal between the US and Japan eased trade concerns.

- Gold will continue to pay attention to US data for any sign of weakness and hence a rate cut due to its sensitivity to interest rates.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 25/07/2025 | 0600/0800 | ** | PPI | |

| 25/07/2025 | 0600/0800 | ** | Unemployment | |

| 25/07/2025 | 0600/0700 | *** | Retail Sales | |

| 25/07/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/07/2025 | 0800/1000 | ** | M3 | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 25/07/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |