JPY: Asia Wrap - USD/JPY Extends Above 147.00

The Asia-Pac USD/JPY range has been 146.97 - 147.49, Asia is currently trading around 147.30, +0.17%. USD/JPY found good demand around 146.00 and has bounced nicely off its first support. Some demand for USD’s was finally seen as the market takes some risk off the table heading into next week which is filled with event risk and also month-end. The CFTC data showed the market is shifting its view on the JPY, with leverage funds just starting to build JPY shorts and Asset managers actively reducing their own. Price has managed a decent bounce off the 146.00 area, the question is can it now build on this ?

- WSJ - “Trump wants a deal, and China is willing to play ball.”

- Daily Chartbook on X: "Japan won’t need to purchase as many Treasuries and other foreign bonds and stocks over the longer term after its trade deal with the US." @LondonSW via ZeroHedge. See Graph Below.

- (Bloomberg) - "Tokyo's CPI rose 2.9% in July from a year earlier, slower than estimated. It’s the first time the pace of gains slipped below 3% since March. Still, food inflation stayed hot, keeping pressure on PM Shigeru Ishiba.”

- Taro Kimura, economist, said "Beneath the surface, cost pressures from earlier spikes in rice prices and rising labor expenses are still feeding through to costs of processed food and dining out," and the data should encourage the Bank of Japan to continue to raise rates gradually.

- “JAPAN'S MAEHARA: NOT THINKING ABOUT JOINING ISHIBA COALITION” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.16b),146.00($1.35b).Upcoming Close Strikes : 145.00($1.3b July 29), 145.00($982m July 28), 148.00($946m July 28) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

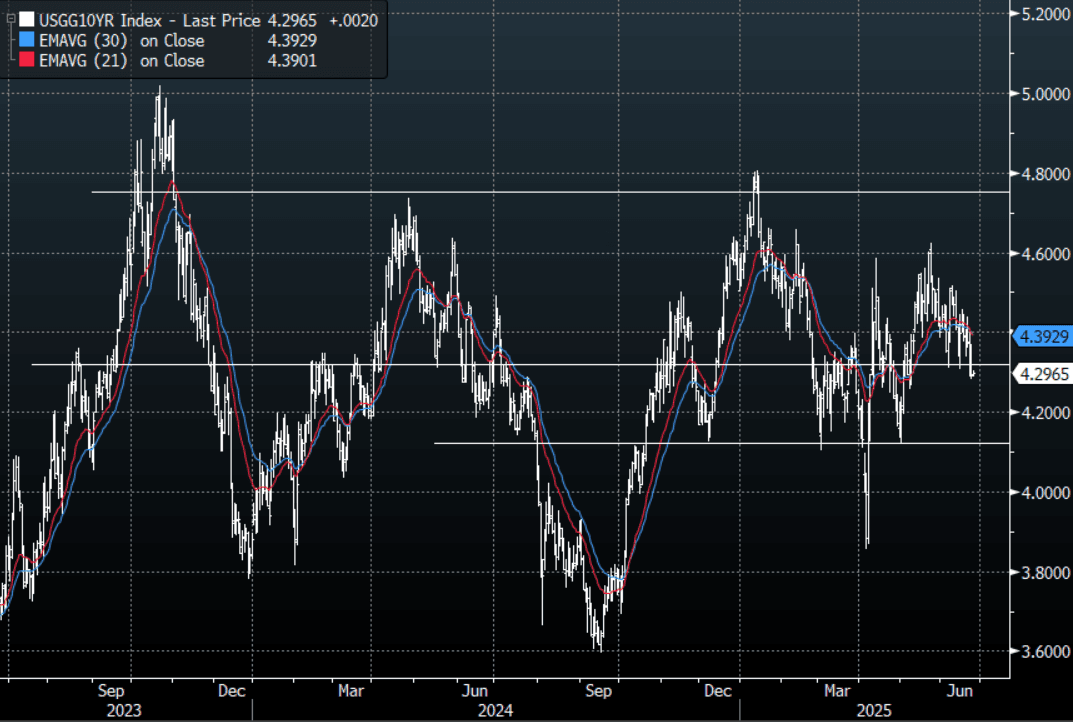

US TSYS: Asia Wrap - Front End Yield Extends Lower

The TYU5 range has been 111-17+ to 111.22 during the Asia-Pacific session. It last changed hands at 110-19+, down 0-01+ from the previous close.

- The US 2-year yield has moved lower trading around 3.79%, down 0.03 from its close.

- The US 10-year yield is relatively unchanged around 4.30%.

- This has seen the yield curve steepen: 2s10s +3.61 at 50.143

- (Bloomberg) - US bond investors are too complacent about inflation and the Fed’s fears it will reaccelerate. Expectations for the decline in yields to accelerate look optimistic given that President Trump’s tax-and-spending bill may boost supply. Inflation is also likely to accelerate ahead of the next Fed meeting. Both this week’s core PCE print for May and the June Core CPI data due in the middle of next month are forecast to show higher readings.

- FED - FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell’s comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy given its resilience, especially the labour market, rather than rushing to ease monetary policy.

- The 10-year yield was again seriously testing the 4.30% support overnight, a sustained move back below here is likely to see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Bond Futures Up on Second Day of Liquidity Injection

- Following a second successive day of CNY209bn of liquidity injection via the OMO, bond futures are up at lunch time.

- The 10YR is up +0.03 to 109.06 and remains above all major moving averages. The nearest being the 20-day EMA at 108.99

- The 3YR is up +0.02 at 102.52 taking it above the 50-day EMA of 102.50. Above at 102.61 lies the 100-day EMA.

- The CBG 10YR remains at 1.64%

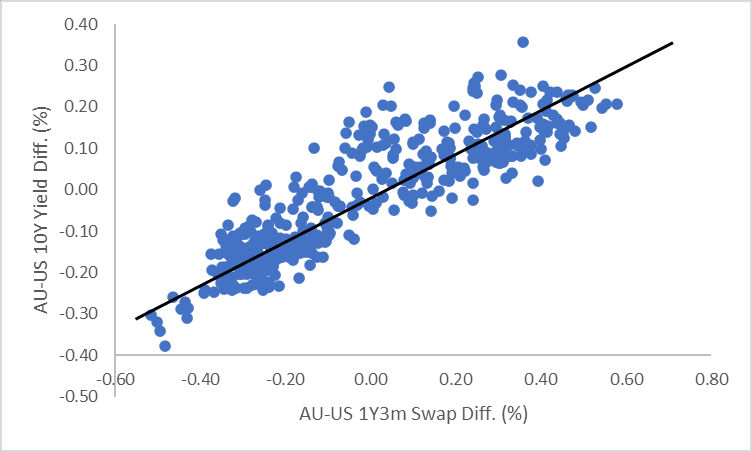

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

The AU-US 10-year cash yield differential currently stands at -16bps, positioned near the bottom of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -12bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the middle of the range at ~-20bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg