US TSYS: Asia Wrap - Yields Edge Slightly Lower

The TYU5 range has been 110-28 to 110-30+ during the Asia-Pacific session. It last changed hands at 110-29+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.912%, up 0.01 from its close.

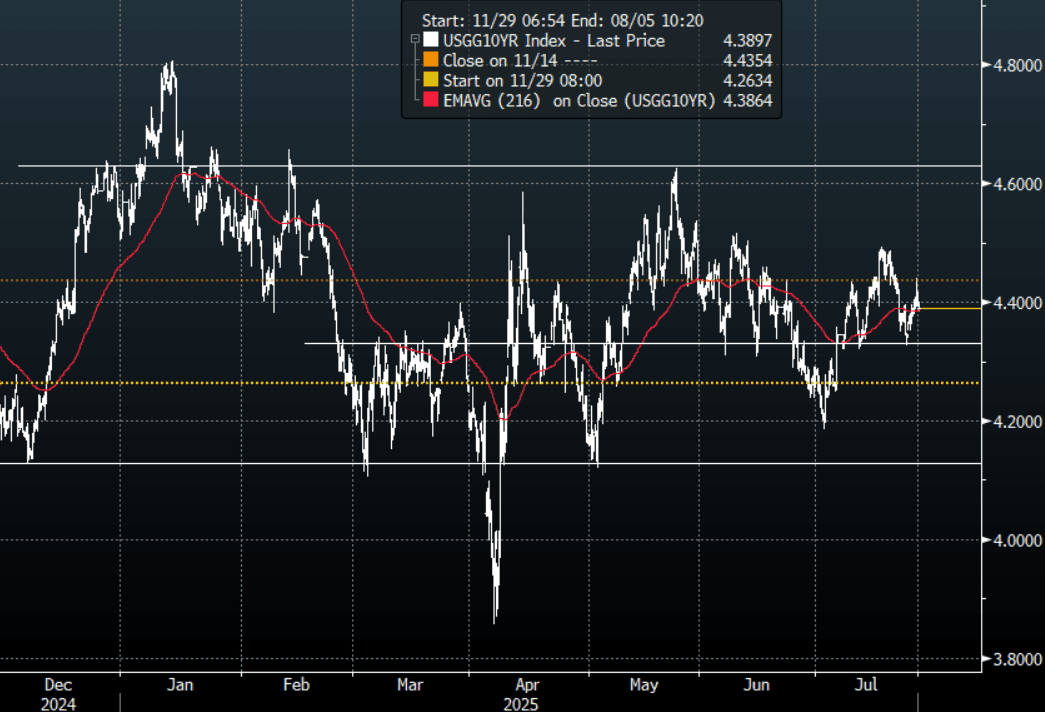

- The US 10-year yield has edged lower trading around 4.39%, up 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A decent bounce off its support but the move failed to follow through above 4.40% overnight.

- Wei Li(CIS BLockRock) on LinkedIn: “Lower Fed policy rate does not always translate into lower long rates, this year's case in point. A number of factors explain the gap, list not exhaustive but all relevant this year: Fiscal trajectory; Investor appetite including international investors; Higher inflation premium: core service inflation volatility is twice the long term levels reflecting greater macro uncertainty. I continue to prefer the front and belly of the curve for income.”

- (Bloomberg) - “Donald Trump said he didn’t see the need to fire Jerome Powell, making it clear he saw lowering rates as a more pressing concern. The two publicly traded barbs over the Fed’s cost overruns during their tour of the project.”

- Bob Elliott on X: “With that performance today it's clear that there is no chance in hell Powell resigns before his chairmanship is up.”

- Data/Events: Durable Goods Orders, Kansas City Fed Services Activity

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Up on Second Day of Liquidity Injection

- Following a second successive day of CNY209bn of liquidity injection via the OMO, bond futures are up at lunch time.

- The 10YR is up +0.03 to 109.06 and remains above all major moving averages. The nearest being the 20-day EMA at 108.99

- The 3YR is up +0.02 at 102.52 taking it above the 50-day EMA of 102.50. Above at 102.61 lies the 100-day EMA.

- The CBG 10YR remains at 1.64%

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

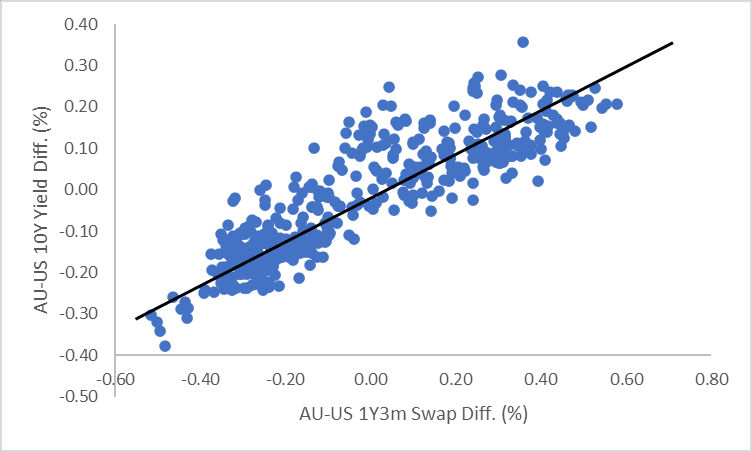

The AU-US 10-year cash yield differential currently stands at -16bps, positioned near the bottom of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -12bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the middle of the range at ~-20bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg

AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes

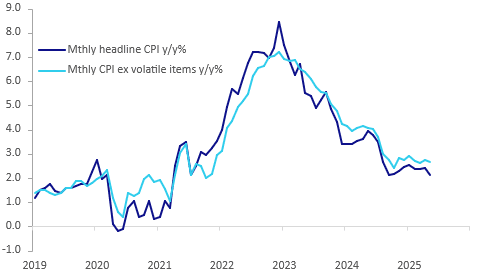

May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. However, CPI ex volatile items and holiday travel was only down 0.1pp to 2.7% y/y. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

Australia CPI y/y%

- Headline continued to be impacted by a number of volatile factors with automotive fuel down 2.9% m/m & 10% y/y due to global oil prices, which are likely to be higher in June given events in the Middle East. Also electricity prices fell 5.9% y/y although up from -6.5% y/y but would have been up 2% y/y without state and federal rebates. Fruit & veg eased to 2.8% y/y from 6.1%. Holiday travel & accommodation moderated sharply to 0.6% y/y from 5.3%.

- More stable components also saw a moderation with insurance at 3.9% y/y after 7.6% and rents 4.5% y/y down from 5.0%. New dwellings only rose 0.8% y/y, the slowest rate since April 2021 as discounts are offered to encourage new business.

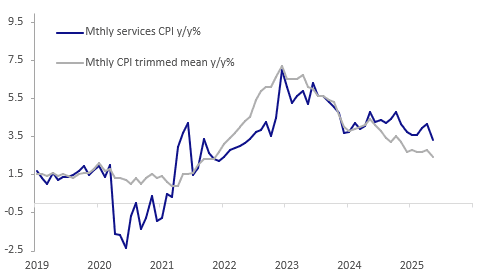

- Domestically-driven measures saw a moderation with services inflation at 3.3% y/y from 4.1%, the lowest since May 2022, and non-tradeables 3.2% from 3.6%, softest since the more recent December 2024.

- Goods inflation was stable in May at 1.0% y/y while tradeables fell to 0% y/y from 0.3% due to fuel.

Australia CPI services vs trimmed mean y/y%