ASIA STOCKS: China Leads with Strong Weekly Returns

China's major bourses delivered strong weekly returns, despite falls on Friday. In a week dominated by new trade deal announcements and no key data from China, news that ETF purchases from the sovereign wealth fund and the announcement of a US / Japan trade deal was enough to get Chinese investors going.

- The Hang Seng is down today by -1.11%, but remains up +2.25% for the week. The CSI 300 is down -0.55% today but up +1.6% for the week. The Shanghai Comp lower by -0.35% today but higher by +1.6 for the week and Shenzhen is down -0.21% today but up over 2% for the week.

- The TAIEX in Taiwan has done very little this week, despite data showing that the ongoing inflows of FDI continued.

- The KOSPI had a modest week but its standard lately, up just +0.29% today and +0.37% for the week.

- The FTSE Malay KLCI fell -0.78% today and is barely holding onto a +0.16% gain for the week.

- The Jakarta Composite is lower by -0.14% today, but has added +2.85% for the week.

- The FTSE Straits Times in Singapore is up +1.4% for the week and the PSEi in the Philippines up +1.8%.

- The NIFTY 50 in India is lower by -0.57% to see it fall into the negative by -0.20% for the week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

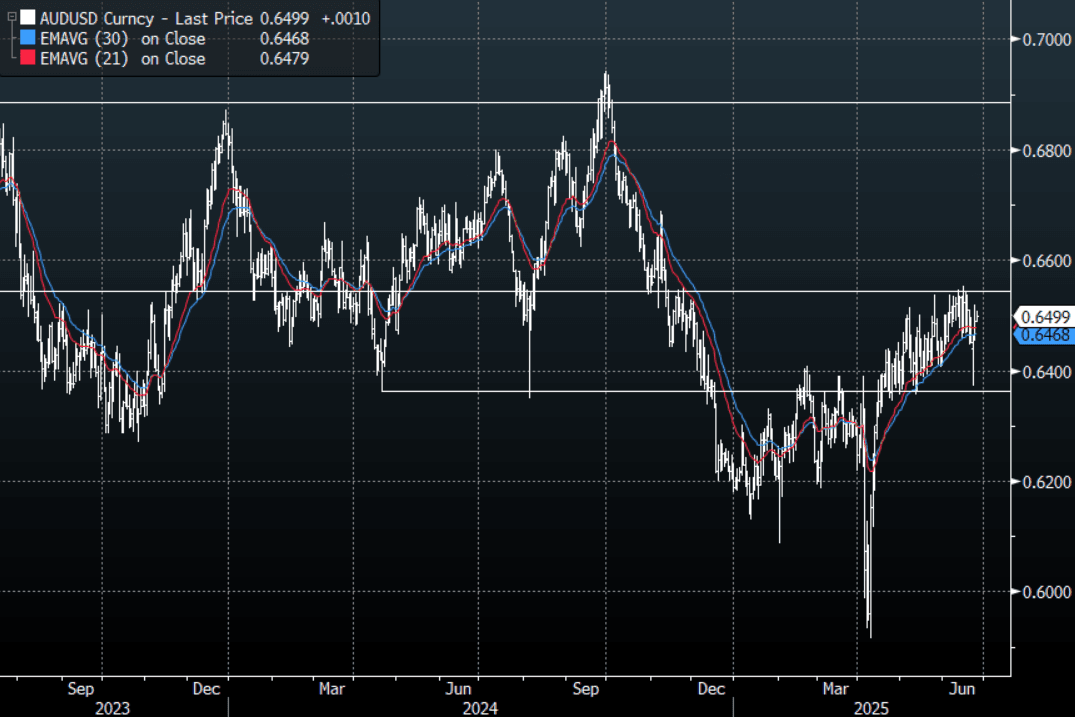

AUD: Asia Wrap - CPI Print Finds Bids Sub 0.6500

The AUD/USD has had a range of 0.6489 - 0.6508 in the Asia- Pac session, it is currently trading around 0.6500, +0.15%. The AUD attempted to move lower on the CPI print but found bids sub 0.6500 and clawed back all its losses. A quiet session sees AUD/USD continue to trade with an underlying bid tone. We are approaching the corporate month-end and this normally results in a demand for USD's so perhaps better levels could be seen for AUD buyers.

- AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes. May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

- The AUD/USD bounced hard off its support and is now back to potentially testing the top end of its range as the USD comes back under pressure.

- We are approaching the corporate month-end and this normally results in a demand for USD’s so perhaps better levels could be seen over the course of the next day or so for those wanting to express a long AUD position.

- Price remains in the wider 0.6350 - 0.6550 range for now. The AUD needs a sustained break above 0.6550 to potentially start building towards a move higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD2.11b June 26), 0.6425(AUD776m June 30).

- AUD/JPY - Today's range 93.98 - 94.28, it is trading currently around 94.20. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

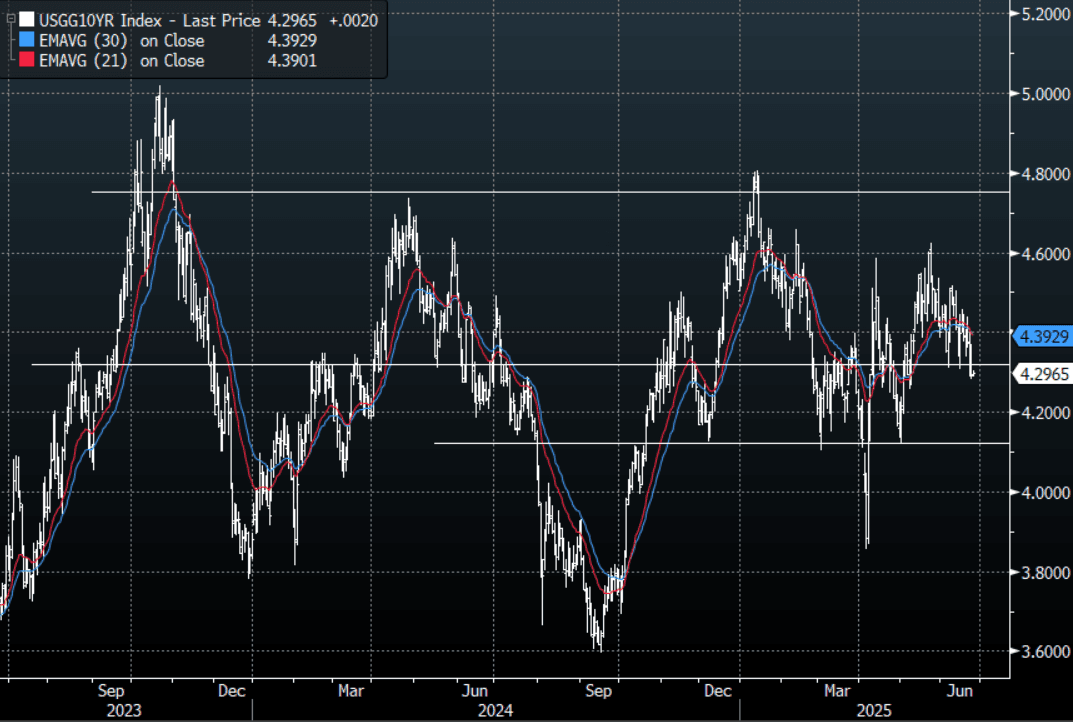

US TSYS: Asia Wrap - Front End Yield Extends Lower

The TYU5 range has been 111-17+ to 111.22 during the Asia-Pacific session. It last changed hands at 110-19+, down 0-01+ from the previous close.

- The US 2-year yield has moved lower trading around 3.79%, down 0.03 from its close.

- The US 10-year yield is relatively unchanged around 4.30%.

- This has seen the yield curve steepen: 2s10s +3.61 at 50.143

- (Bloomberg) - US bond investors are too complacent about inflation and the Fed’s fears it will reaccelerate. Expectations for the decline in yields to accelerate look optimistic given that President Trump’s tax-and-spending bill may boost supply. Inflation is also likely to accelerate ahead of the next Fed meeting. Both this week’s core PCE print for May and the June Core CPI data due in the middle of next month are forecast to show higher readings.

- FED - FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell’s comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy given its resilience, especially the labour market, rather than rushing to ease monetary policy.

- The 10-year yield was again seriously testing the 4.30% support overnight, a sustained move back below here is likely to see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Bond Futures Up on Second Day of Liquidity Injection

- Following a second successive day of CNY209bn of liquidity injection via the OMO, bond futures are up at lunch time.

- The 10YR is up +0.03 to 109.06 and remains above all major moving averages. The nearest being the 20-day EMA at 108.99

- The 3YR is up +0.02 at 102.52 taking it above the 50-day EMA of 102.50. Above at 102.61 lies the 100-day EMA.

- The CBG 10YR remains at 1.64%