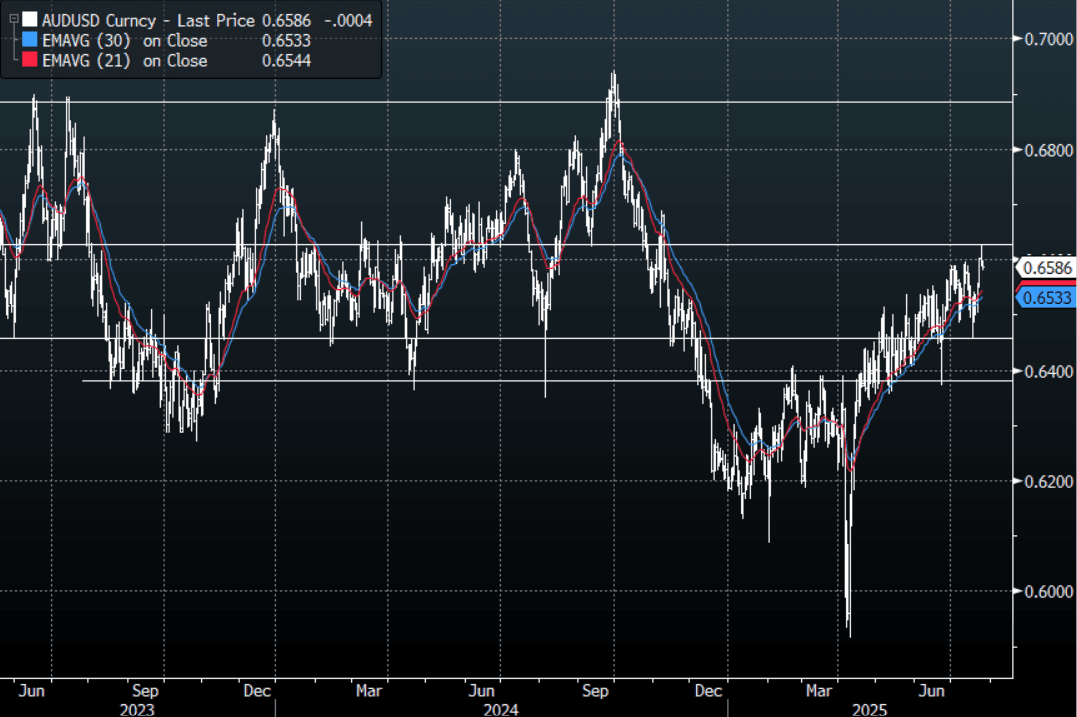

AUD: Asia Wrap - AUD/USD Drifts Lower

The AUD/USD has had a range of 0.6579 - 0.6599 in the Asia- Pac session, it is currently trading around 0.6582, -0.12%. The pair ran into some decent supply above 0.6600 and has drifted lower as the USD finally bounces. The pair is challenging the top of its recent range and a sustained move above 0.6600 could see it gain upward momentum, but there is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- WSJ - “Trump wants a deal, and China is willing to play ball.”

- (Bloomberg) -- “Australia and the UK will hold talks between their foreign and defense ministers in Sydney on Friday, with the aim of signing a £20 billion ($27 billion) “treaty” to help build nuclear-powered submarines.”

- (AFR) "In the new Reserve Bank regime, Bullock has limited opportunities to make policy speeches and so the Anika address was eagerly anticipated by economists and traders, most of whom were blindsided by the July call. Bullock made it clear that she is not all that fussed about guiding the market. But her message on Thursday is that the RBA intends to stick to its winning strategy of taking a slow and steady approach."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6450(AUD552m). Upcoming Close Strikes : 0.6600(AUD968m July29), 0.6600(AUD823m July 30), 0.6550(AUD704m July30) - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

- AUD/JPY - Today's range 96.87 - 97.14, it is trading currently around 96.95, +0.05%. The pair extended its move higher overnight. The support between 95.00 - 96.00 held as demand materialised first up, the pair is looking to regain its momentum for a move higher. The Event-risk of next week could provide some short-term headwinds.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Up on Second Day of Liquidity Injection

- Following a second successive day of CNY209bn of liquidity injection via the OMO, bond futures are up at lunch time.

- The 10YR is up +0.03 to 109.06 and remains above all major moving averages. The nearest being the 20-day EMA at 108.99

- The 3YR is up +0.02 at 102.52 taking it above the 50-day EMA of 102.50. Above at 102.61 lies the 100-day EMA.

- The CBG 10YR remains at 1.64%

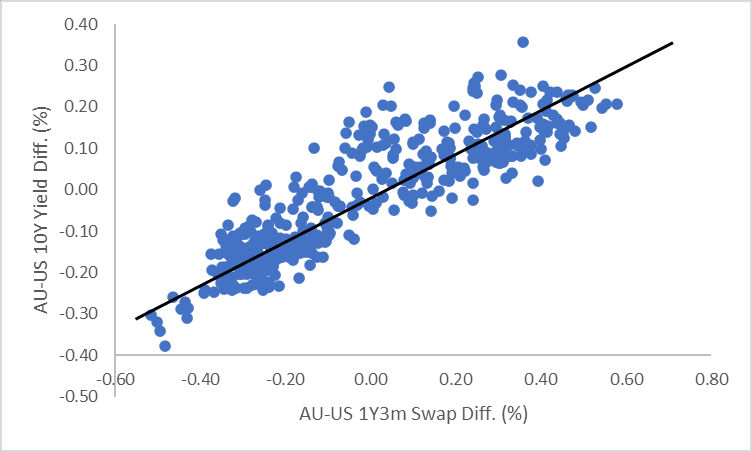

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

The AU-US 10-year cash yield differential currently stands at -16bps, positioned near the bottom of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -12bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the middle of the range at ~-20bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg

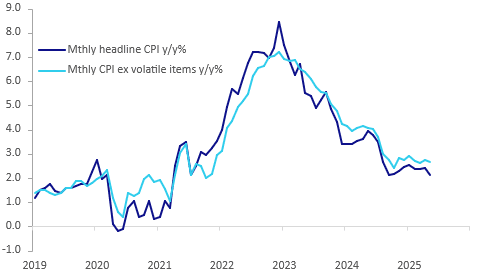

AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes

May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. However, CPI ex volatile items and holiday travel was only down 0.1pp to 2.7% y/y. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

Australia CPI y/y%

- Headline continued to be impacted by a number of volatile factors with automotive fuel down 2.9% m/m & 10% y/y due to global oil prices, which are likely to be higher in June given events in the Middle East. Also electricity prices fell 5.9% y/y although up from -6.5% y/y but would have been up 2% y/y without state and federal rebates. Fruit & veg eased to 2.8% y/y from 6.1%. Holiday travel & accommodation moderated sharply to 0.6% y/y from 5.3%.

- More stable components also saw a moderation with insurance at 3.9% y/y after 7.6% and rents 4.5% y/y down from 5.0%. New dwellings only rose 0.8% y/y, the slowest rate since April 2021 as discounts are offered to encourage new business.

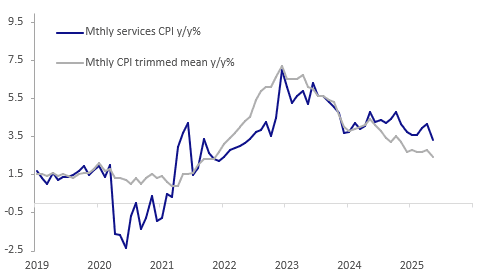

- Domestically-driven measures saw a moderation with services inflation at 3.3% y/y from 4.1%, the lowest since May 2022, and non-tradeables 3.2% from 3.6%, softest since the more recent December 2024.

- Goods inflation was stable in May at 1.0% y/y while tradeables fell to 0% y/y from 0.3% due to fuel.

Australia CPI services vs trimmed mean y/y%