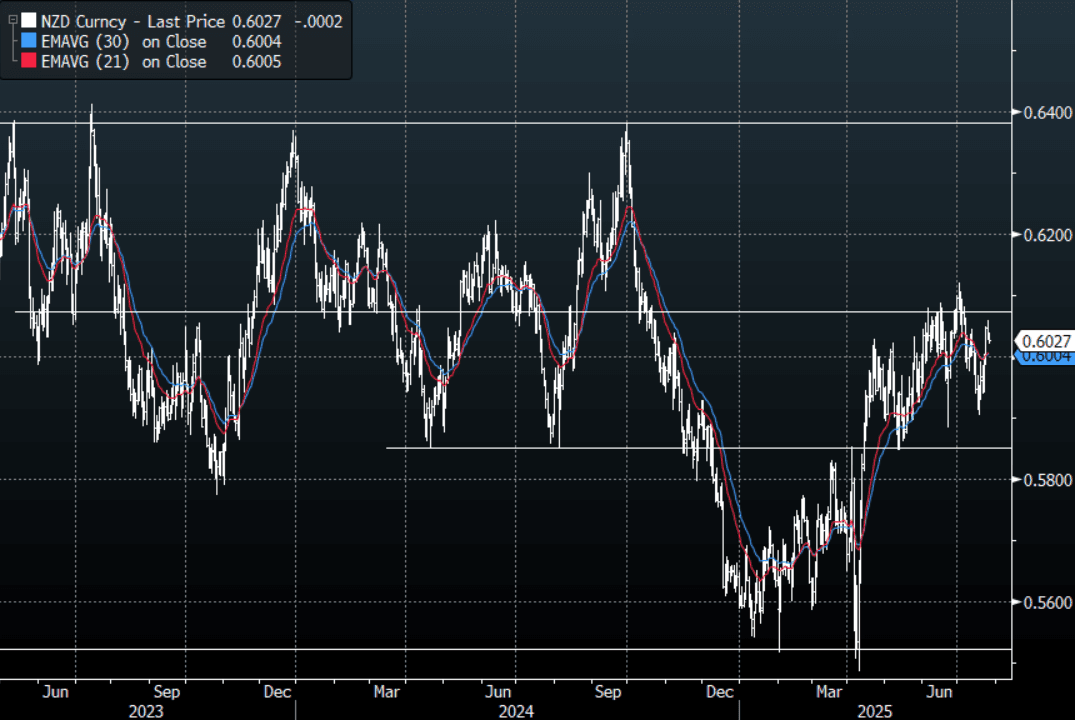

NZD: Asia Wrap - NZD/USD Drifts Back Towards 0.6000

The NZD/USD had a range of 0.6021 - 0.6039 in the Asia-Pac session, going into the London open trading around 0.6022, -0.12%. The pair ran into some decent supply around the 0.6050 area and has drifted lower as the USD finally finds some demand. Depending what your view is this 0.6050 area looks an attractive fade initially, the danger though is the USD which is looking sickly once more and should it capitulate the NZD could build momentum higher again. Price will need a sustained break back above the 0.6050/0.6100 area to signal a potential base might be in place. There is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- (Bloomberg) -- “Standard Chartered recommends buying the New Zealand dollar against the Swiss franc, calling it a clean way to position for continued improvement in global risk sentiment heading into the Aug. 1 US tariff deadline.”

- “Strategists including Steven Englander, head of global G-10 FX research at Standard Chartered, recommend going long NZD-CHF at 0.4796, with a target of 0.5150 and a stop-loss at 0.4680, expressing a tactical three-month view.”

- “We think the US is likely to conclude more trade deals with remaining holdouts such as Europe and Korea, following an agreement with Japan,” they wrote in a note. “Treasury Secretary Bessent also signalled an extension in US-China trade talks, reducing the probability of a re-escalation in trade tensions”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30). - BBG

- AUD/NZD range for the session has been 1.0916 - 1.0934, currently trading 1.0917. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Bullion Stabilises After Middle East Truce Drives Stronger Risk Appetite

After falling 1.3% on Tuesday, gold rose to a high of $3335.24/oz today as markets stabilised following an easing in tensions in the Middle East which reduced safe-haven flows. They are now monitoring how well Israel and Iran are sticking to the ceasefire. It has been quiet on this front so far today. Bullion has come off its intraday high to be up 0.1% to $3327.2. The USD and US yields are slightly higher from early in the session.

- Gold’s bullish theme is intact and this week’s decline is seen as corrective. Moving average studies are also still in a bull mode signalling a dominant uptrend. The yellow metal will monitor US data closely for signs of negative economic impacts from import duties and any change in the Fed’s “on hold” tone. Initial resistance is at $3451.3, 16 June high, while support is at $3286.2, 50-day EMA.

- Silver has range traded reaching a high of $35.99 and then a low of $35.90. It is currently moderately higher at $35.93. Initial support is at $35.55 and resistance at $37.32. Any sell off is still seen as corrective.

- Equities are mixed with the S&P e-mini flat, Topix down 0.2% but Hang Seng up 0.8%. Oil prices are higher with WTI +1.4% to $65.28/bbl. Copper is 0.4% higher.

- Later Fed Chair Powell continues his testimonies. The Fed’s Goolsbee, ECB’s Donnery and BoE’s Lombardelli speak. US May new home sales/permits print.

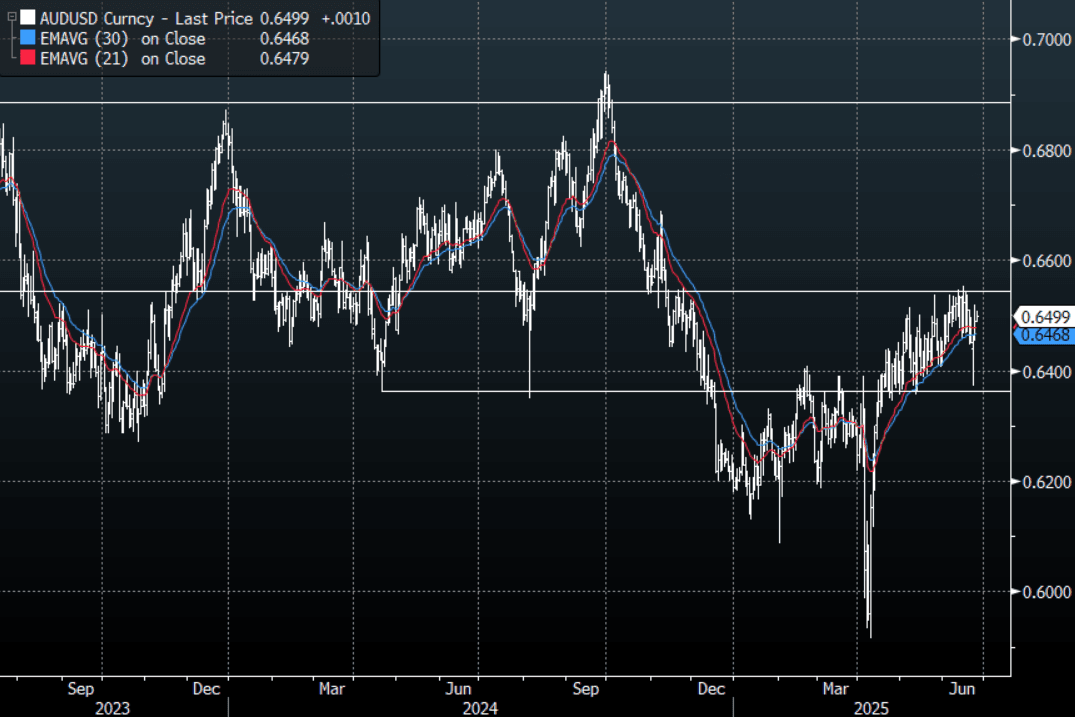

AUD: Asia Wrap - CPI Print Finds Bids Sub 0.6500

The AUD/USD has had a range of 0.6489 - 0.6508 in the Asia- Pac session, it is currently trading around 0.6500, +0.15%. The AUD attempted to move lower on the CPI print but found bids sub 0.6500 and clawed back all its losses. A quiet session sees AUD/USD continue to trade with an underlying bid tone. We are approaching the corporate month-end and this normally results in a demand for USD's so perhaps better levels could be seen for AUD buyers.

- AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes. May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

- The AUD/USD bounced hard off its support and is now back to potentially testing the top end of its range as the USD comes back under pressure.

- We are approaching the corporate month-end and this normally results in a demand for USD’s so perhaps better levels could be seen over the course of the next day or so for those wanting to express a long AUD position.

- Price remains in the wider 0.6350 - 0.6550 range for now. The AUD needs a sustained break above 0.6550 to potentially start building towards a move higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD2.11b June 26), 0.6425(AUD776m June 30).

- AUD/JPY - Today's range 93.98 - 94.28, it is trading currently around 94.20. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

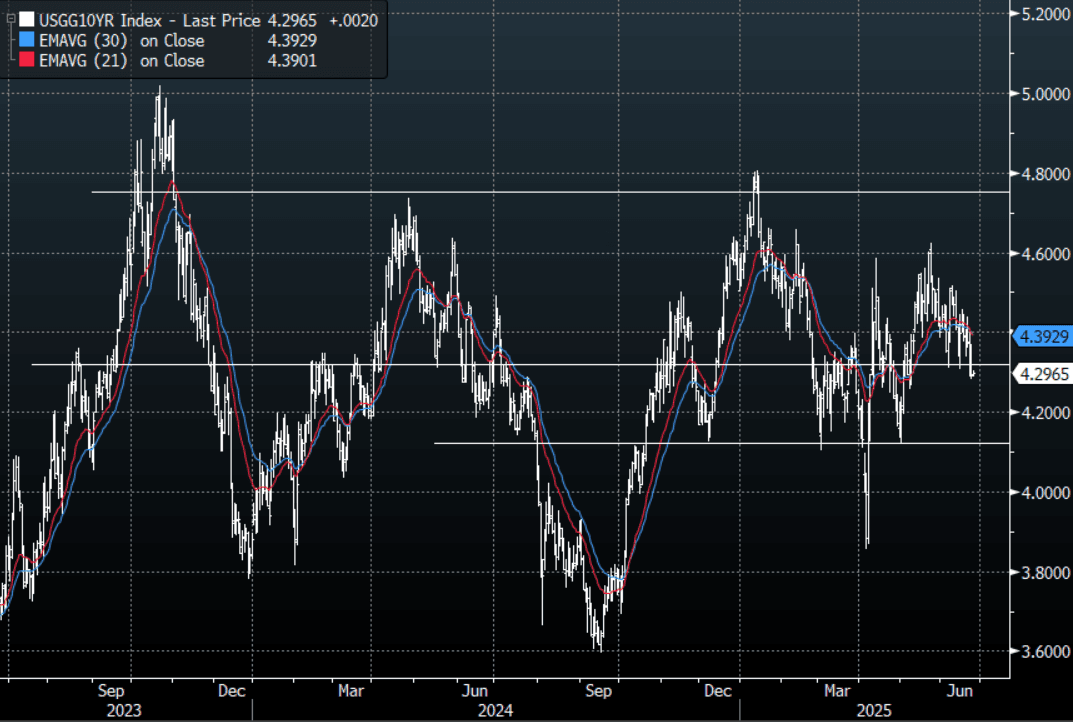

US TSYS: Asia Wrap - Front End Yield Extends Lower

The TYU5 range has been 111-17+ to 111.22 during the Asia-Pacific session. It last changed hands at 110-19+, down 0-01+ from the previous close.

- The US 2-year yield has moved lower trading around 3.79%, down 0.03 from its close.

- The US 10-year yield is relatively unchanged around 4.30%.

- This has seen the yield curve steepen: 2s10s +3.61 at 50.143

- (Bloomberg) - US bond investors are too complacent about inflation and the Fed’s fears it will reaccelerate. Expectations for the decline in yields to accelerate look optimistic given that President Trump’s tax-and-spending bill may boost supply. Inflation is also likely to accelerate ahead of the next Fed meeting. Both this week’s core PCE print for May and the June Core CPI data due in the middle of next month are forecast to show higher readings.

- FED - FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell’s comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy given its resilience, especially the labour market, rather than rushing to ease monetary policy.

- The 10-year yield was again seriously testing the 4.30% support overnight, a sustained move back below here is likely to see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P