MNI EUROPEAN MARKETS ANALYSIS: Vote to Avoid Shutdown Fails

- The US begins a shutdown with Democrats and Trump unable to agree a deal.

- Asian markets largely ignore US troubles with several major bourses up strongly with China out.

- The Reserve Bank of India maintained rates at 5.50% for a second consecutive meeting.

- The day ahead sees PMIs in Europe, ADP and Global Manufacturing, ISM and Construction spend whilst all eyes on the shutdown.

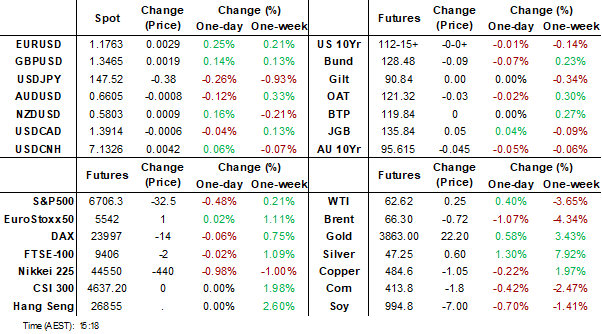

US TSYS: Asia Wrap - Yields A Little Lower As Shutdown Begins

The TYZ5 range has been 112-13 to 112-16+ during the Asia-Pacific session. It last changed hands at 112-16, unchanged from the previous close.

- The US 2-year yield has edged lower trading 3.605%.

- The US 10-year yield is trading around 4.148%.

- 10-Year yields remain subdued below 4.20% as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP tonight starts to take on a lot more relevance.

- MNI: Fed’s Logan Cautious On Cuts Given Still-High Inflation. “I will be cautious about further rate cuts,” Logan said. "Even setting aside temporary effects of this year's increases in tariff rates, inflation is not convincingly on track to return all the way to 2%.”

- Brian Sullivan on X: “It can be an uncomfortable thing because so many people and families are worried about their paychecks, but markets tend to go UP in government shutdowns. It's because shutdowns 1) don't involve all of the government and 2) tend to be short and 3) the economy actually tends to keep growing. Weird but true.”

- Data/Events: MBA Mortgage Applications, ADP Employment Change, S&P Global US Manufacturing PMI, ISM Manufacturing, Construction Spending

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Slight Twist-Steepener, $550bn Investment In US In Focus

JGB futures are stronger, +5 compared to settlement levels.

- Bloomberg - "Markets are focused on how Japan will finance $550 billion in investment it has agreed to make in the US as part of a trade deal with President Donald Trump. The readily available resources that meet Tokyo's funding conditions don't look sufficient - we see a $250 billion shortfall."

- Japan’s Akazawa said the next administration should implement the $550B fund, noting the U.S. is not concerned with the split between investment and loans, and Japan can decide allocation. He added the fund will be used without impacting forex.

- An Asahi poll shows Koizumi leading the LDP leadership race among lawmakers. MBBG

- Japan will get its second prime minister in just over a year when the ruling Liberal Democratic Party holds a leadership election on Oct. 4.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash JGBs are little changed across benchmarks out to the 10-year, but 1-2bps cheaper beyond.

- Swap rates are flat to 2bps higher, with a steepening bias. Swap spreads are mixed.

- Tomorrow, the local calendar will see Monetary Base and International Investment Flow data alongside 10-year supply and a speech by BOJ Deputy Governor Uchida.

AUSSIE BONDS: Holding Weaker But Off Worst levels

ACGBs (YM -2.5 & XM -4.0) are weaker but off session cheaps?

- Bloomberg - "China Bans New BHP Orin Ore Cargoes Ad Pricing Dispute Grows. China's state-run iron ore buyer has told major steelmakers and traders to temporarily halt purchases of all new BHP Group cargoes, escalating a pricing dispute that risks upending one of the mining giants most important trading partnerships."

- "ALBANESE SAYS CHINA'S BAN ON BHP ORE CARGOES IS `DISAPPOINTING".

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash ACGBs are 2-6bps cheaper with the AU-US 10-year yield differential at +21bps.

- The bills strip is -3 to -4 beyond the first contract (-2).

- RBA-dated OIS pricing has firmed modestly across meetings following yesterday's RBA Policy Decision. Pricing across meetings is 1-4bps firmer than yesterday's pre-RBA levels. Notably, this post-RBA move leaves pricing some 10-18bps firmer than last Wednesday's pre-CPI levels.

- A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

- Tomorrow, the local calendar will see Trade Balance data and the release of the RBA’s Financial Stability Review.

- The AOFM plans to sell A$1000mn of the 1.25% 21 May 2032 bond on Friday.

BONDS: NZGBS: Closed Modestly Cheaper

NZGBs closed 1-2bps cheaper across benchmarks after a relatively subdued session.

- NZGBs underperformed the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials finishing 2bps wider.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- (Bloomberg) -- A La Niña watch is in effect with international guidance suggesting a 60% chance it will be established before Dec 31, Earth Sciences New Zealand says in an update.

- Swap rates closed flat to 4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. 34bps of easing is priced for October, with a cumulative 62bps by November 2025.

- Tomorrow, the local calendar will see Cotality Home Values.

- The NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 4.50% May-35 bond.

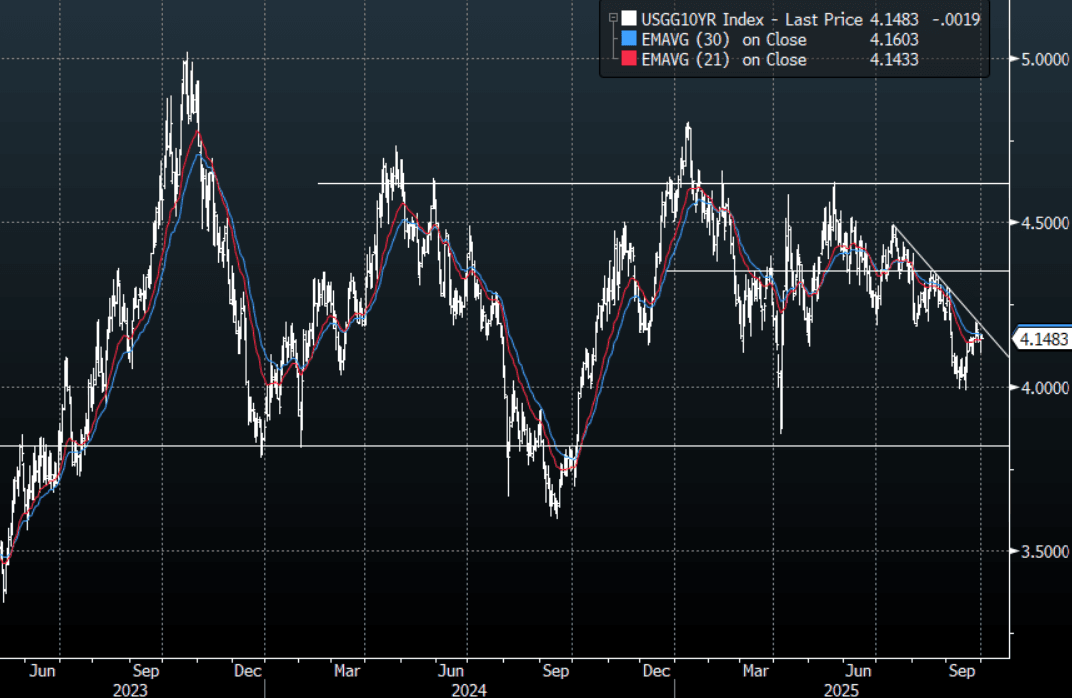

FOREX: Asia FX Wrap - BBDXY Testing 1200 On US Shutdown

The BBDXY has had a range of 1200.12 - 1201.63 in the Asia-Pac session; it is currently trading around 1200, -0.01%. The USD again found some support around the 1200 area after initially being heavily sold on the imminent shutdown. First support back towards the 1200 area and then 1195. The USD has historically not done well during shutdowns, but tends to bounce back quite hard when they eventually end. The fact we are still above 1200 has been impressive though I am not sure it can bounce too far as the shutdown orders look to be executed this morning. I thought it would be a tough ask to see any big directional moves this week until the market gets a look at the Payroll number but with this data now unavailable the ADP could take on a lot more relevance tonight.

- EUR/USD - Asian range 1.1730 - 1.1743, Asia is currently trading 1.1750. The pair found sellers just above 1.1750 overnight. The deeper correction looks to have been put on hold for now as the focus turns toward how this shutdown plays out.

- GBP/USD - Asian range 1.3435 - 1.3452, Asia is currently dealing around 1.3450. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should now be looking for bounces to fade initially, first sell zone is back towards the 1.3500 area.

- USD/CNH - Asian range 7.1251 - 7.1397, Asia is currently dealing around 7.1380. The area just below 7.1000 has proved to be well supported recently so looks like we could consolidate 7.09-7.16 for now.

- Cross asset : SPX -0.45%, Gold $3860, US 10-Year 4.146%, BBDXY 1200, Crude Oil $62.54

- Data/Events : Spain HCOB Spain Manufacturing PMI, Germany HCOB Germany Manufacturing PMI, France HCOB France Manufacturing PMI, Italy HCOB Italy Manufacturing PMI/Budget Balance, EZ HCOB Eurozone Manufacturing PMI/CPI

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

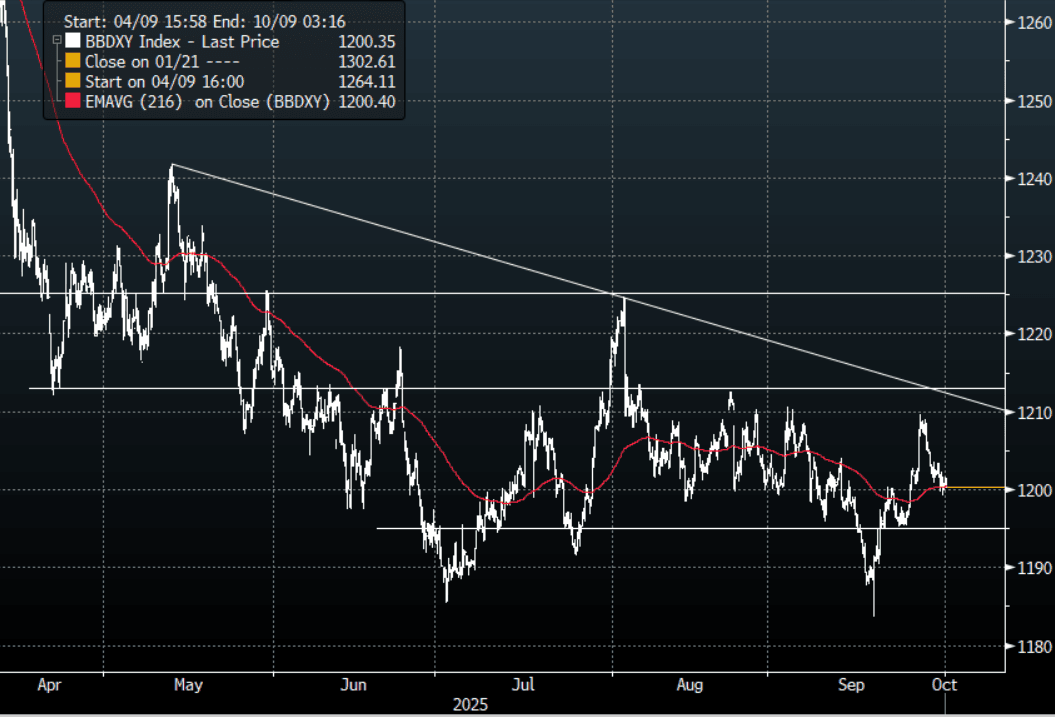

JPY: Asia Wrap - USD/JPY Tries And Fails Above 148.00 On The Tankan

The USD/JPY range has been 147.82 - 148.23 in the Asia-Pac session, it is currently trading around 147.90, -0.02%. The pair popped back above 148.00 on the Tankan survey but failed toward 148.25 and quickly reversed all of its gains. We are once again right back in the middle of very familiar ranges. The Payrolls data this week was to be critical, so a shutdown now makes the ADP print tonight take on larger significance. First support is seen around 147.50 then back toward the bottom of the range around 146.00.

- MNI - Tankan Steady, Capex Intentions Higher: The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector. Respondents see USDJPY around 145.68 in FY25.

- Bloomberg - “Markets are focused on how Japan will finance $550 billion in investment it has agreed to make in the US as part of a trade deal with President Donald Trump. The readily available resources that meet Tokyo’s funding conditions don’t look sufficient — we see a $250 billion shortfall.”

- "AKAZAWA: WANT NEXT ADMINISTRATION TO CARRY OUT $550B FUND, US NOT INTERESTED IN BREAKDOWN OF INVESTMENT, LOANS, UP TO JAPAN TO DECIDE INVESTMENT AMOUNT WITHIN $550B, ILL USE $550B FUND IN WAYS THAT WON'T IMPACT FOREX" - BBG

- "KOIZUMI LEADS JAPAN LDP RACE AMONG LAWMAKERS: ASAHI POLL" - BBG

- "JAPAN DPP LEADER TAMAKI: ETF SALES COULD FUND GOVT SPENDING, BOJ SHOULD OFFLOAD ALL ETFS WITHIN 15 YEARS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.15($864m), 146.50($1.09b), 147.50($650m). Upcoming Close Strikes : 147.00($1.21b Oct 6), 148.00($1.15b Oct 2) - BBG.

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

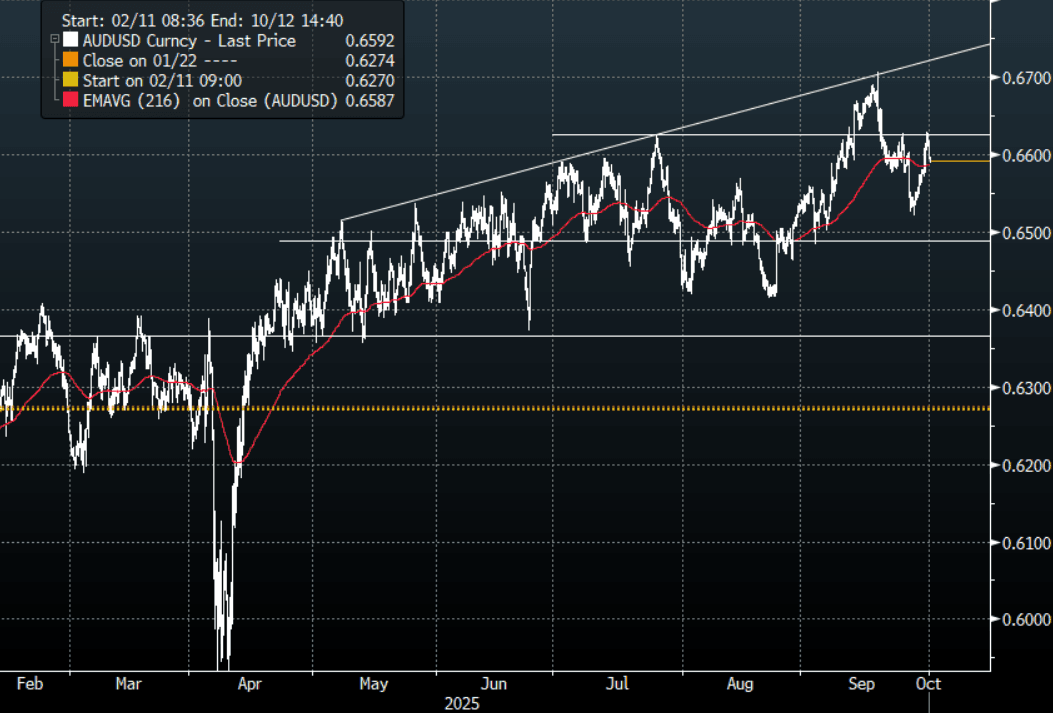

AUD: Asia Wrap - AUD/USD Gives Back Overnight Gains As Shutdown Begins

The AUD/USD has had a range of 0.6589- 0.6618 in the Asia- Pac session, it is currently trading around 0.6590, -0.32%. The AUD drifted lower in Asia in sympathy with US Equity futures which traded lower as the US Shutdown begins to be executed. Price action has stalled towards 0.6625 initially, the fate of the USD will determine if this move higher can regain the momentum to have another look toward the pivotal 0.6700 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print tonight could take on larger significance.

- MNI RBA WATCH: Bullock Declines To Confirm Easing Bias. Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Bloomberg - “China Bans New BHP Orin Ore Cargoes Ad Pricing Dispute Grows. China’s state-run iron ore buyer has told major steelmakers and traders to temporarily halt purchases of all new BHP Group cargoes, escalating a pricing dispute that risks upending one of the mining giants most important trading partnerships.”

- "ALBANESE SAYS CHINA'S BAN ON BHP ORE CARGOES IS `DISAPPOINTING"

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD742m), 0.6600(AUD983m), 0.6700(AUD1.64b). Upcoming Close Strikes : 0.6600(AUD1.55b Oct 3), 0.6600(AUD1.74b Oct 2), 0.6700(AUD1.06b Oct 6) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.49 - 97.92, Asia is trading around 97.50. The pair has struggled to gain any traction above 98.00 with the upward momentum stalling. A break sub 97.00 could signal a deeper correction.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

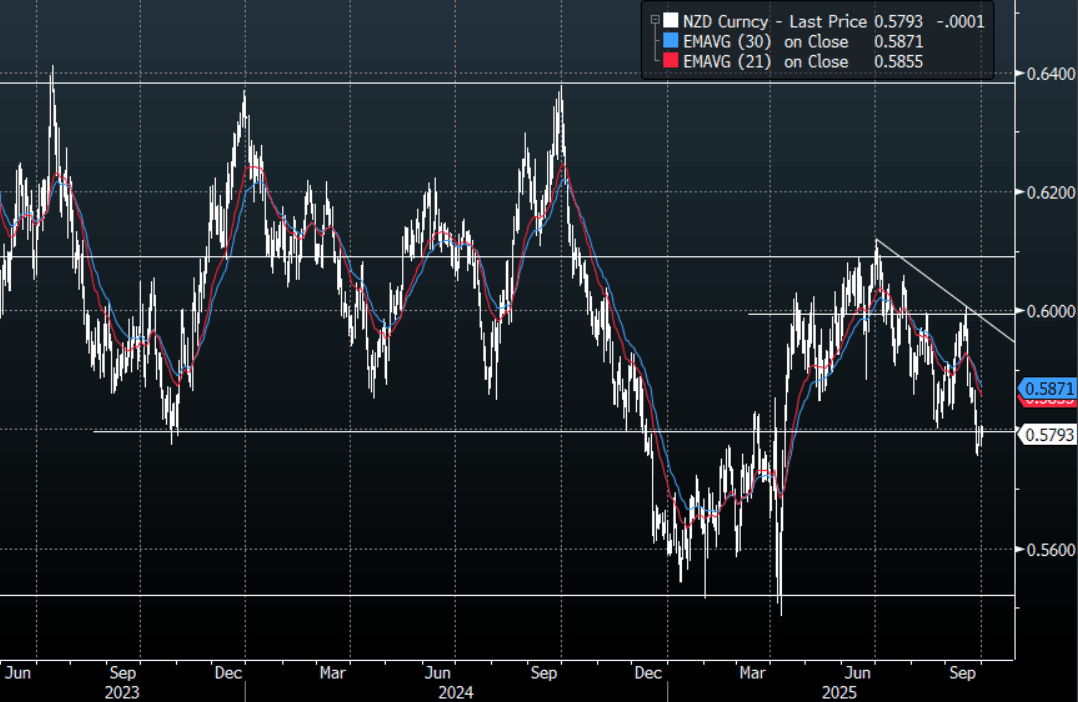

NZD: Asia Wrap - NZD/USD Consolidates Around 0.5800

The NZD/USD had a range of 0.5786 - 0.5805 in the Asia-Pac session, going into the London open trading around 0.5795, +0.05%. The NZD broke through its pivotal 0.5800 support last week and even though it has drifted higher the last few days it has traded heavily around 0.5800 even with the USD falling. The first sell zone would be between the 0.5850/0.5900 area.

- MNI INTERVIEW: RBNZ To Eye 2% OCR Level - Ex Assistant Gov. The Reserve Bank of New Zealand is likely to need to cut the 3% Official Cash Rate by 100 basis points over the medium term to stabilise output and inflation following weaker-than-expected Q2 GDP data, a former assistant governor told MNI.

- Bloomberg - “ The NZ government has offered to support the three power companies in which it has a majority shareholding if they need to raise capital for new electricity generation - even if it's not renewable.”

- MNI - Cotality home values for September are scheduled to be released between October 1 and 10. August was the fifth consecutive monthly decline in house prices, which may be weighing on consumer confidence.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5825(NZD360m). Upcoming Close Strikes : 0.5850(NZD310m Oct 2) - BBG

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

- AUD/NZD range for the session has been 1.1385 - 1.1415, currently trading around 1.1385. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 could initially be met with some selling and expect some work to be done up here before another extension higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: No China as KOSPI and TAIEX Lead Gains

South Korean companies have supported stock markets through buybacks. In most developed markets, once shares are bought back they are cancelled whereas in Korea they are retained by the company which (for some) opens up the opportunity for manipulation. The National Assembly is likely to pass a bill by year-end that would require companies to cancel shares bought back, according to Park Hong Bae, a lawmaker in the ruling Democratic Party.

- The NIKKEI continues to fall after last week's new all time highs and is off -0.85% today, and week to date down over -1.5%

- The KOSPI is up +0.85% on a strong day for data as exports surprised to the upside.

- The TAIEX had a strong day yesterday and followed that up again today with gains of +0.95%.

- The FTSE Malay KLCI is having one its strongest day of the week, up +0.57%.

- The Jakarta Composite fell by -0.77% yesterday and is barely positive today, up +0.10%

- The NIFTY 50 fell for eight consecutive day and following the RBI decision, has moved higher by +0.20%

OIL: Crude Stabilises, Holding Onto Week’s Losses Ahead Of OPEC Meeting

Oil prices are moderately higher during today’s APAC session after falling sharply earlier this week. WTI is up 0.4% to $62.61/bbl off the intraday low of $62.20 and Brent is 0.3% higher at $66.24/bbl after falling to $65.87. The USD index is down 0.1% after the US government shutdown began at midnight ET.

- Supply/demand fundamentals remain in focus with a prolonged US government shutdown potentially impacting energy demand and reportedly a 500kbd increase in OPEC’s output target for November to be discussed at its 5 October meeting. According to Bloomberg though, OPEC has denied that it is considering three consecutive monthly 500kbd rises.

- Bloomberg reported a US crude stock drawdown of 3.7mn last week, according to people familiar with the API data. However, gasoline rose 1.3mn and distillate 3.0mn. Inventory data is being monitored for signs of excess supply as the IEA is forecasting a record market surplus in 2026. The official EIA data is scheduled for Wednesday but may now be delayed. If it follows the industry data will show a third consecutive weekly inventory drop.

- With the government shutdown, some US data may be postponed. September ADP employment, final September S&P Global manufacturing PMI & ISM and August construction are scheduled for Wednesday. European September manufacturing PMIs and euro area September CPI print. The Fed’s Barkin and Goolsbee and ECB’s Elderson & de Guindos speak.

Gold Off Earlier High After Senate Vote Fails, Shutdown Has Begun

Gold prices spiked to a new record at $3878.53/oz during Wednesday after a vote in the US senate failed to break the debt ceiling impasse. It has benefited from significant safe haven flows driven by related concerns. The government shutdown began at midnight ET but bullion remains below the earlier high up 0.1% to $3860.8 as the risk had been priced in. The US dollar index is slightly higher and yields are little changed.

- September US payrolls scheduled for Friday were widely anticipated to gauge the Fed outlook but at this stage they look they will be delayed. Fed views continue to diverge with 2026’s FOMC member Logan saying that easing should proceed cautiously.

- President Trump has said that the shutdown is likely to result in job losses.

- Silver reached a high of $47.56, breaking above initial resistance at $47.251, earlier in the APAC session but is now up 0.9% today at around $47.04. It has also benefited from US concerns but also physical tightness given its use in solar panels.

- Equities are mixed with the S&P e-mini down 0.4% and Nikkei -1.0% but KOSPI up 0.8%. Oil prices are slightly higher with WTI +0.3% to $62.57/bbl. Copper is down 0.3%.

- With the government shutdown, some US data may be delayed. September ADP employment, final September S&P Global manufacturing PMI & ISM and August construction are scheduled for Wednesday. European September manufacturing PMIs and euro area September CPI print. The Fed’s Barkin and Goolsbee and ECB’s Elderson & de Guindos speak.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 01/10/2025 | 0630/0830 | ** | Retail Sales | |

| 01/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0730/0930 | ECB Elderson Keynote at ECB Climate Conference | ||

| 01/10/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ECB de Guindos Interview & Panel at Politico Summit | ||

| 01/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/10/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 01/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 01/10/2025 | 0955/1055 | BOE Mann In Bloomberg Interview | ||

| 01/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 01/10/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/10/2025 | 1215/0815 | *** | ADP Employment Report | |

| 01/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/10/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 01/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 01/10/2025 | 1730/1330 | BOC Summary of Deliberations | ||

| 01/10/2025 | 1805/1405 | BOC Sr Deputy Rogers speaks at competition panel | ||

| 02/10/2025 | 0130/1130 | ** | Trade Balance | |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export |