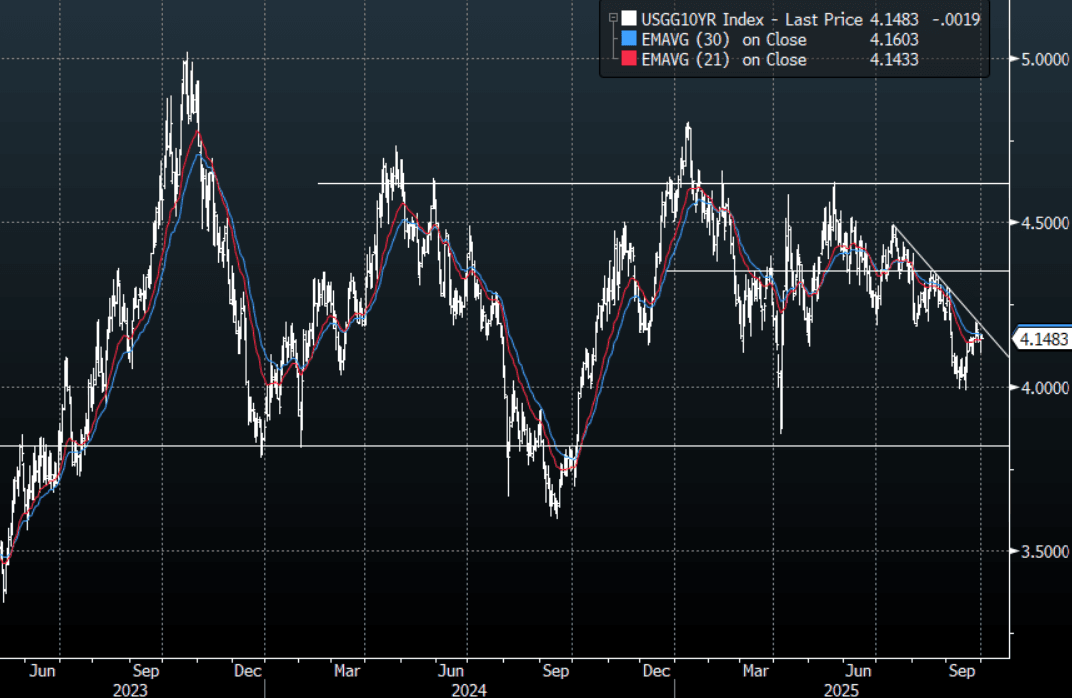

US TSYS: Asia Wrap - Yields A Little Lower As Shutdown Begins

The TYZ5 range has been 112-13 to 112-16+ during the Asia-Pacific session. It last changed hands at 112-16, unchanged from the previous close.

- The US 2-year yield has edged lower trading 3.605%.

- The US 10-year yield is trading around 4.148%.

- 10-Year yields remain subdued below 4.20% as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP tonight starts to take on a lot more relevance.

- MNI: Fed’s Logan Cautious On Cuts Given Still-High Inflation. “I will be cautious about further rate cuts,” Logan said. "Even setting aside temporary effects of this year's increases in tariff rates, inflation is not convincingly on track to return all the way to 2%.”

- Brian Sullivan on X: “It can be an uncomfortable thing because so many people and families are worried about their paychecks, but markets tend to go UP in government shutdowns. It's because shutdowns 1) don't involve all of the government and 2) tend to be short and 3) the economy actually tends to keep growing. Weird but true.”

- Data/Events: MBA Mortgage Applications, ADP Employment Change, S&P Global US Manufacturing PMI, ISM Manufacturing, Construction Spending

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD/USD Drifting Higher

The AUD/USD has had a range of 0.6535 - 0.6549 in the Asia- Pac session, it is currently trading around 0.6545, +10%. The USD is trading heavy just above its support as the market begins to think about the ramifications of tariffs being judged to be illegal. The AUD drifted higher but without real momentum. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Private House Approvals Moving Sideways: July number of building approvals fell 8.2% m/m to be up 6.6% y/y after rising 12.2% m/m & 28% y/y in June. Both months were driven by the volatile multi-dwelling component which fell 22.3% m/m after rising 33.5%. The more stable private homes rose 1.1% m/m to be up only 0.3% y/y after -1.9% m/m & +0.5% y/y in June with 3-month momentum in the sector soft.

- Little Change In Q2 Inventories, Profits Remain Weak: Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday’s Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1’s 0.2% & 1.3%.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6455(AUD555m). Upcoming Close Strikes : 0.6400(AUD768m Sept 2), 0.6445(AUD945m Sept 4), 0.6600(AUD813m Sept 4) - BBG

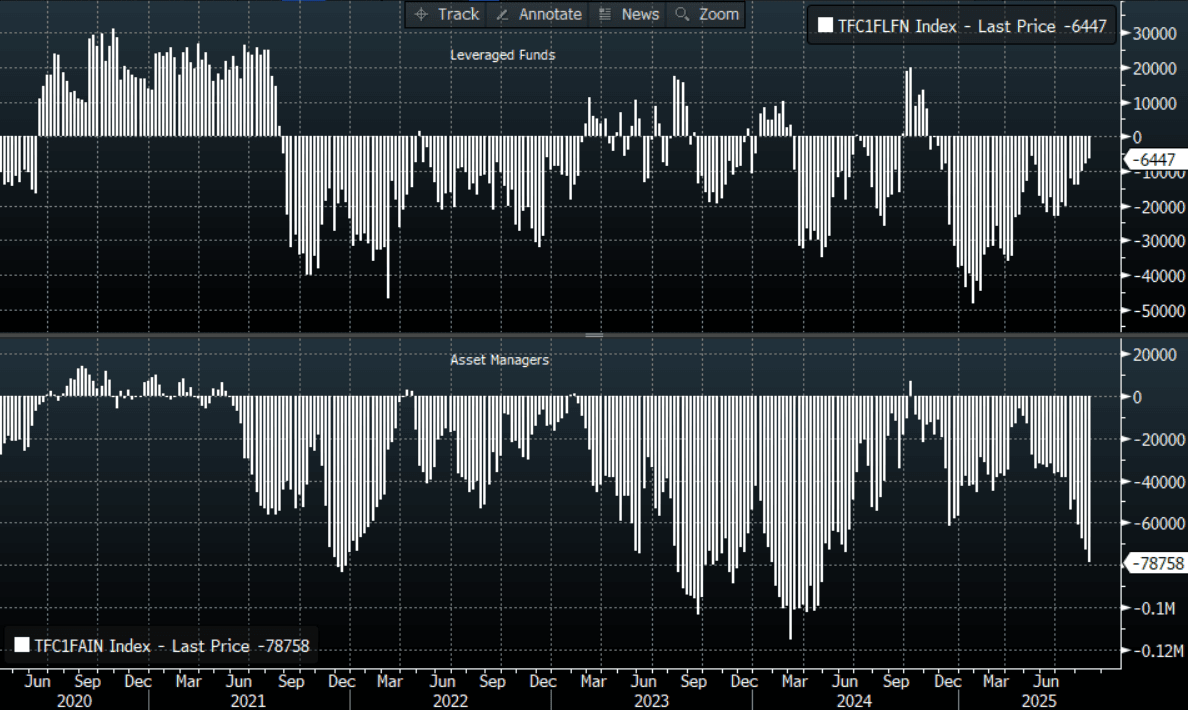

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.12 - 96.42, Asia is trading around 96.15. The pair is probing above the 96.00 area this morning. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/ CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

MNI EXCLUSIVE: MNI Discusses The RBA's Cash Rate Strategy

BONDS: NZGBS: Yields Edge Higher, New RBNZ Governor Expected Soon

New Zealand government bond yields have risen in Monday trade. Benchmark yields are up 1-2bps with the back end outperforming marginally. The 2yr was at 2.96%, while the 10yr (up around 2bps) was close to 4.36%. For the 2yr focus will be on whether we can recapture the 3.00% handle, while for the 10yr pre RBNZ highs were closer to 4.50%, so still some distance away. The 2yr swap rate is up a little over 1bps, last at 2.74%.

- The bias for Asia Pac bond yields has been to move higher, with back end Aussie bond yields notably higher. US Tsy futures are also biased lower (with no cash trading today given the US holiday). These shifts have likely aided NZ yield moves, albeit lagging the ACGB yield moves.

- In terms of news flow: "- New Zealand expects to appoint a new Reserve Bank governor within weeks, Prime Minister Christopher Luxon said.", while "New Zealand will loosen its ban on foreigners buying houses, allowing holders of golden visas to buy houses worth at least NZ$5 million. (both via BBG).

- Earlier data showed building approvals up 5.4%m/m for July, but this followed a -6.0% fall prior. The data out this week is term tier, with terms of trade printing tomorrow.