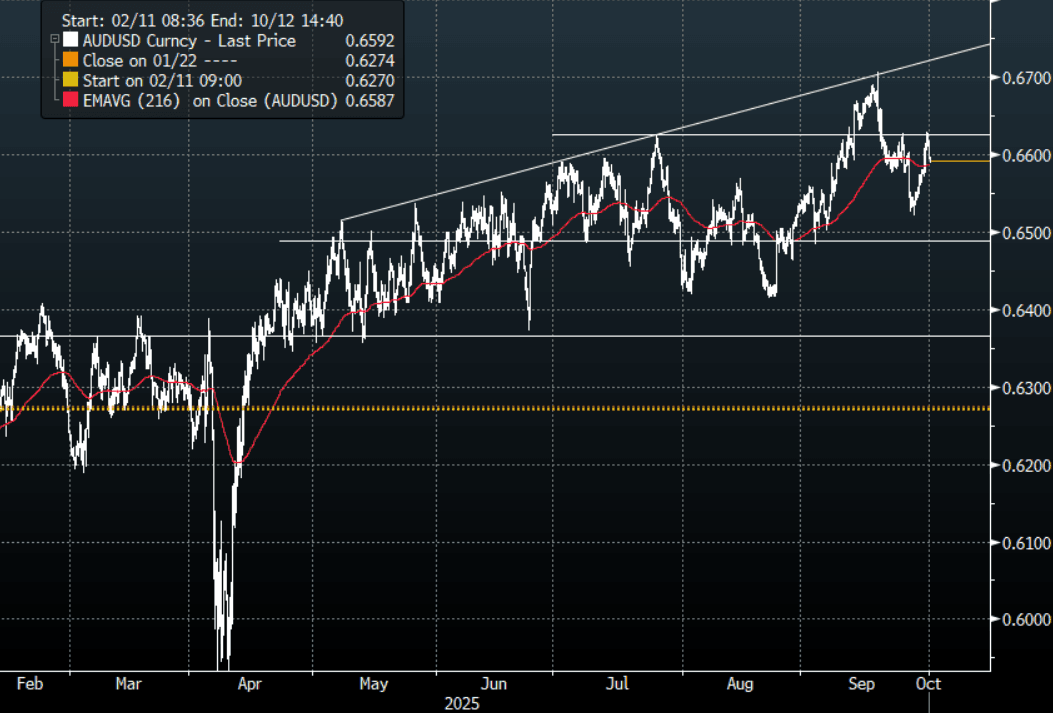

AUD: Asia Wrap - AUD/USD Gives Back Overnight Gains As Shutdown Begins

The AUD/USD has had a range of 0.6589- 0.6618 in the Asia- Pac session, it is currently trading around 0.6590, -0.32%. The AUD drifted lower in Asia in sympathy with US Equity futures which traded lower as the US Shutdown begins to be executed. Price action has stalled towards 0.6625 initially, the fate of the USD will determine if this move higher can regain the momentum to have another look toward the pivotal 0.6700 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print tonight could take on larger significance.

- MNI RBA WATCH: Bullock Declines To Confirm Easing Bias. Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Bloomberg - “China Bans New BHP Orin Ore Cargoes Ad Pricing Dispute Grows. China’s state-run iron ore buyer has told major steelmakers and traders to temporarily halt purchases of all new BHP Group cargoes, escalating a pricing dispute that risks upending one of the mining giants most important trading partnerships.”

- "ALBANESE SAYS CHINA'S BAN ON BHP ORE CARGOES IS `DISAPPOINTING"

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD742m), 0.6600(AUD983m), 0.6700(AUD1.64b). Upcoming Close Strikes : 0.6600(AUD1.55b Oct 3), 0.6600(AUD1.74b Oct 2), 0.6700(AUD1.06b Oct 6) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.49 - 97.92, Asia is trading around 97.50. The pair has struggled to gain any traction above 98.00 with the upward momentum stalling. A break sub 97.00 could signal a deeper correction.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Yields Firmer, Led By The Back End

Aussie bond futures sit lower for Monday trade, with the back end underperforming. XM (10yr futures)were last 95.655, off 4.5bps, while YM (3yr futures) we down 3bps to 96.56. US Tsy futures are weaker in the first part of Monday trade, although there is no cash trading today due to the US holiday later. On Friday the US cash Tsy curve finished steeper. The Fed's Daly gave some dovish remarks around the need to recalibrate policy soon.

- For cash ACGB yields, we are 2-6bps firmer across the benchmarks, with the back end leading. The 3 yr is up close to 3bps, last near 3.42%, while the 10 is +4bps, tracking above 4.31% .

- On the data front - Little Change In Q2 Inventories, Profits Remain Weak: Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday's Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1's 0.2% & 1.3%. July number of building approvals fell 8.2% m/m to be up 6.6% y/y after rising 12.2% m/m & 28% y/y in June.

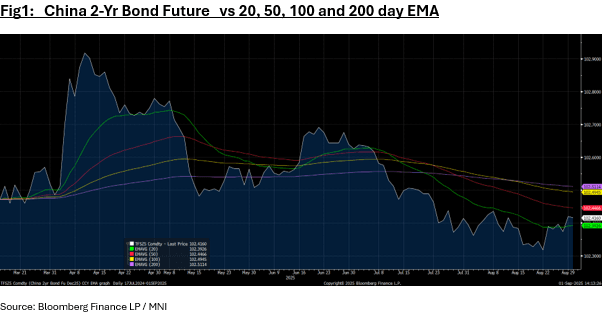

CHINA: Bond Futures Up Strongly Monday

- China's bond futures have started the trading week with a strong rally during the Monday morning session.

- Up +0.10 to 107.92, the 10-Yr remains well below the major moving averages with the 20-day EMA the nearest at 108.05.

- The 2-Yr is flat at 102.41 to remain at the mid-point of the 20-day EMA of 102.39 and the 50-day EMA of 102.44.

- Bonds are doing very little with the 10-Yr marginally better at 1.78%

AUD: Asia Wrap - AUD/USD Drifting Higher

The AUD/USD has had a range of 0.6535 - 0.6549 in the Asia- Pac session, it is currently trading around 0.6545, +10%. The USD is trading heavy just above its support as the market begins to think about the ramifications of tariffs being judged to be illegal. The AUD drifted higher but without real momentum. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Private House Approvals Moving Sideways: July number of building approvals fell 8.2% m/m to be up 6.6% y/y after rising 12.2% m/m & 28% y/y in June. Both months were driven by the volatile multi-dwelling component which fell 22.3% m/m after rising 33.5%. The more stable private homes rose 1.1% m/m to be up only 0.3% y/y after -1.9% m/m & +0.5% y/y in June with 3-month momentum in the sector soft.

- Little Change In Q2 Inventories, Profits Remain Weak: Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday’s Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1’s 0.2% & 1.3%.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6455(AUD555m). Upcoming Close Strikes : 0.6400(AUD768m Sept 2), 0.6445(AUD945m Sept 4), 0.6600(AUD813m Sept 4) - BBG

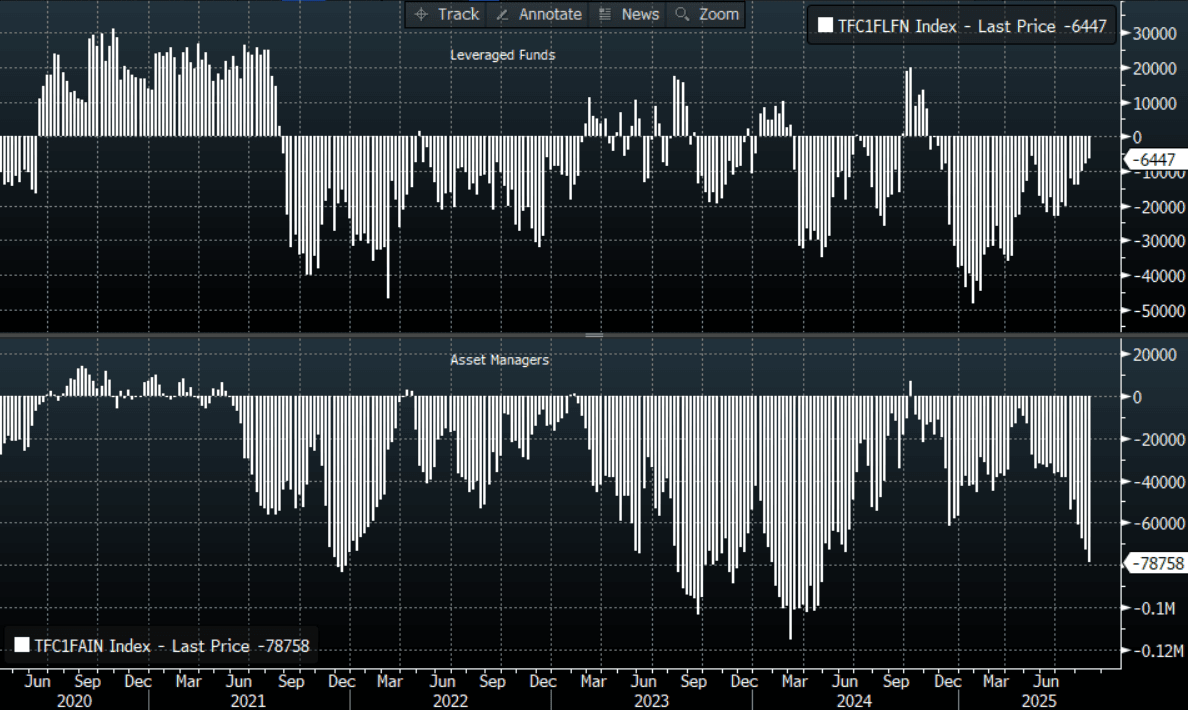

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.12 - 96.42, Asia is trading around 96.15. The pair is probing above the 96.00 area this morning. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/ CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P