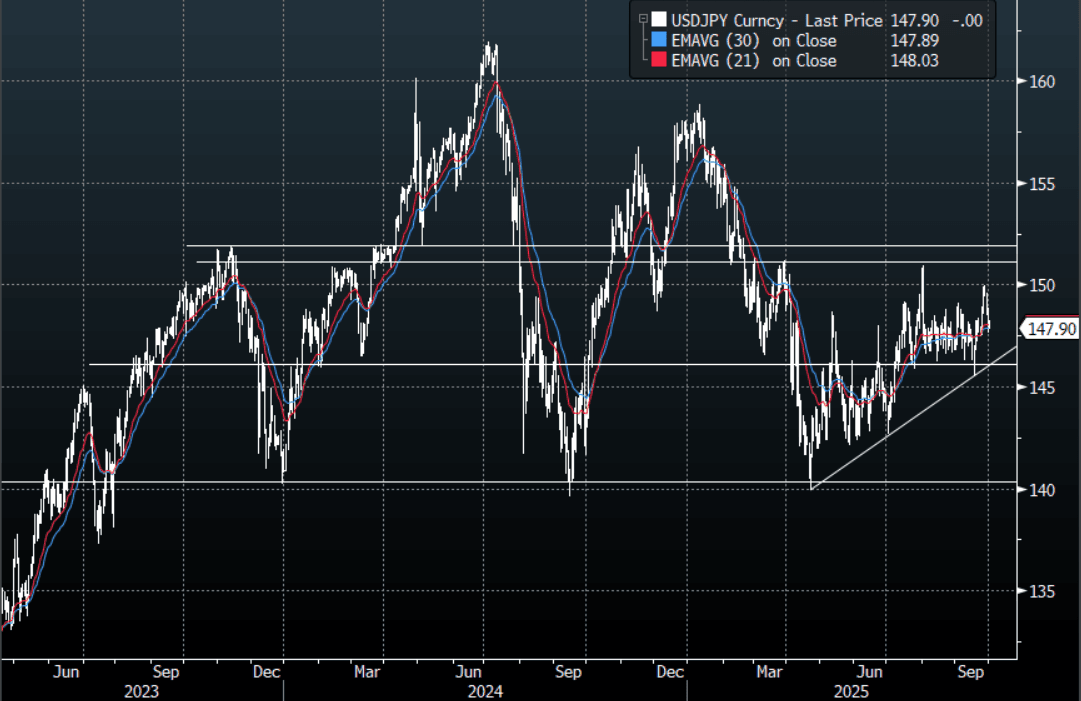

JPY: Asia Wrap - USD/JPY Tries And Fails Above 148.00 On The Tankan

The USD/JPY range has been 147.82 - 148.23 in the Asia-Pac session, it is currently trading around 147.90, -0.02%. The pair popped back above 148.00 on the Tankan survey but failed toward 148.25 and quickly reversed all of its gains. We are once again right back in the middle of very familiar ranges. The Payrolls data this week was to be critical, so a shutdown now makes the ADP print tonight take on larger significance. First support is seen around 147.50 then back toward the bottom of the range around 146.00.

- MNI - Tankan Steady, Capex Intentions Higher: The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector. Respondents see USDJPY around 145.68 in FY25.

- Bloomberg - “Markets are focused on how Japan will finance $550 billion in investment it has agreed to make in the US as part of a trade deal with President Donald Trump. The readily available resources that meet Tokyo’s funding conditions don’t look sufficient — we see a $250 billion shortfall.”

- "AKAZAWA: WANT NEXT ADMINISTRATION TO CARRY OUT $550B FUND, US NOT INTERESTED IN BREAKDOWN OF INVESTMENT, LOANS, UP TO JAPAN TO DECIDE INVESTMENT AMOUNT WITHIN $550B, ILL USE $550B FUND IN WAYS THAT WON'T IMPACT FOREX" - BBG

- "KOIZUMI LEADS JAPAN LDP RACE AMONG LAWMAKERS: ASAHI POLL" - BBG

- "JAPAN DPP LEADER TAMAKI: ETF SALES COULD FUND GOVT SPENDING, BOJ SHOULD OFFLOAD ALL ETFS WITHIN 15 YEARS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.15($864m), 146.50($1.09b), 147.50($650m). Upcoming Close Strikes : 147.00($1.21b Oct 6), 148.00($1.15b Oct 2) - BBG.

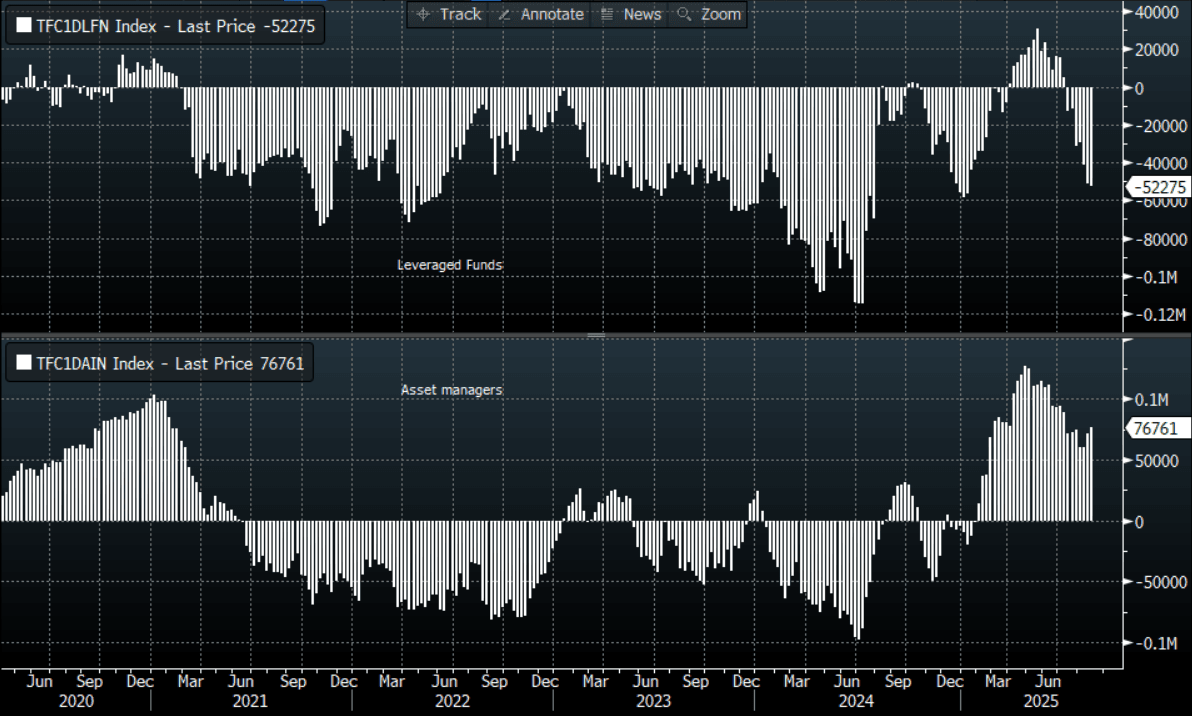

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Asia Wrap - USD/JPY Struggles Above 147.00

The Asia-Pac USD/JPY range has been 146.84-147.38, Asia is currently trading around 146.90, -0.10%. USD/JPY initially tried higher after the Japanese Fix, but ran into sellers and quickly fell back below 147.00. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00. The options market is showing signs of these JPY shorts beginning to buy strikes lower down to hedge themselves.

- (Bloomberg) --Leveraged investors are building positions in the options market that will benefit if Japan’s currency breaks free from its current narrow band of around 147 to the greenback and appreciate beyond 145, data from the Chicago Mercantile Exchange show.

- “Yen Shorts Are Running Out of Road as BOJ Hike Nears: USD/JPY’s downward path is set to accelerate at the start of a new trading month as big leveraged shorts will find it harder to justify their stance with an October BOJ rate hike looking increasingly likely. Especially as traders price for more rate cuts from the Federal Reserve.” - BBG

- MNI BRIEF: Japan Q2 Capex Lower; GDP Seen Revised Down. Bank of Japan officials are focused on the September Tankan survey due Oct 1 to assess the impact of tariffs on corporate profits and business plans, particularly capex. While demand for investment to ease labour shortages remains firm, global demand uncertainty is prompting some firms to delay implementation.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.35($310m).Upcoming Close Strikes : 146.50($1.39b Sept 3), 145.50($976m Sept 3) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Yields Firmer, Led By The Back End

Aussie bond futures sit lower for Monday trade, with the back end underperforming. XM (10yr futures)were last 95.655, off 4.5bps, while YM (3yr futures) we down 3bps to 96.56. US Tsy futures are weaker in the first part of Monday trade, although there is no cash trading today due to the US holiday later. On Friday the US cash Tsy curve finished steeper. The Fed's Daly gave some dovish remarks around the need to recalibrate policy soon.

- For cash ACGB yields, we are 2-6bps firmer across the benchmarks, with the back end leading. The 3 yr is up close to 3bps, last near 3.42%, while the 10 is +4bps, tracking above 4.31% .

- On the data front - Little Change In Q2 Inventories, Profits Remain Weak: Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday's Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1's 0.2% & 1.3%. July number of building approvals fell 8.2% m/m to be up 6.6% y/y after rising 12.2% m/m & 28% y/y in June.

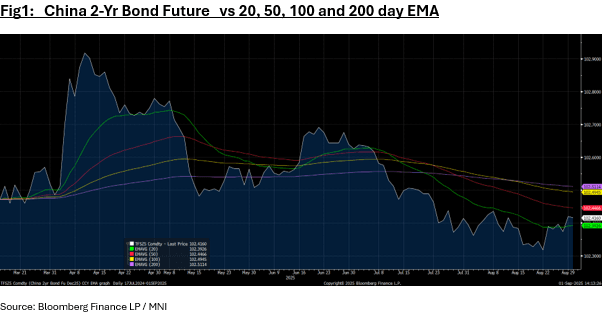

CHINA: Bond Futures Up Strongly Monday

- China's bond futures have started the trading week with a strong rally during the Monday morning session.

- Up +0.10 to 107.92, the 10-Yr remains well below the major moving averages with the 20-day EMA the nearest at 108.05.

- The 2-Yr is flat at 102.41 to remain at the mid-point of the 20-day EMA of 102.39 and the 50-day EMA of 102.44.

- Bonds are doing very little with the 10-Yr marginally better at 1.78%