GOLD: Gold Off Earlier High After Senate Vote Fails, Shutdown Has Begun

Gold prices spiked to a new record at $3878.53/oz during Wednesday after a vote in the US senate failed to break the debt ceiling impasse. It has benefited from significant safe haven flows driven by related concerns. The government shutdown began at midnight ET but bullion remains below the earlier high up 0.1% to $3860.8 as the risk had been priced in. The US dollar index is slightly higher and yields are little changed.

- September US payrolls scheduled for Friday were widely anticipated to gauge the Fed outlook but at this stage they look they will be delayed. Fed views continue to diverge with 2026’s FOMC member Logan saying that easing should proceed cautiously.

- President Trump has said that the shutdown is likely to result in job losses.

- Silver reached a high of $47.56, breaking above initial resistance at $47.251, earlier in the APAC session but is now up 0.9% today at around $47.04. It has also benefited from US concerns but also physical tightness given its use in solar panels.

- Equities are mixed with the S&P e-mini down 0.4% and Nikkei -1.0% but KOSPI up 0.8%. Oil prices are slightly higher with WTI +0.3% to $62.57/bbl. Copper is down 0.3%.

- With the government shutdown, some US data may be delayed. September ADP employment, final September S&P Global manufacturing PMI & ISM and August construction are scheduled for Wednesday. European September manufacturing PMIs and euro area September CPI print. The Fed’s Barkin and Goolsbee and ECB’s Elderson & de Guindos speak.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold & Silver Rally On Risk Appetite Pullback

Gold prices are 0.9% higher at $3478.0/oz after a peak of $3486.11 which followed a low of $3437.11. It is above resistance at $3451.3 opening up the bull trigger at $3500.1. The US dollar is only slightly lower but generally risk appetite is a bit weaker ahead of a number of risk events this week.

- There could be a decision on whether Fed Governor Cook can continue in her role as early as Tuesday and August payrolls print on Friday, which could shift market pricing for a September 17 rate cut in either direction. Currently over an 85% chance is priced into the market.

- Following a US appeals court decision on Friday that this year’s tariffs are illegal, uncertainty over their future remains high. They remain in place though until a final ruling is made.

- Silver is up sharply by 1.9% to $40.48, breaking above round number resistance at $40.00 reinforcing the uptrend. It reached a high of $40.539 earlier.

- Equities are mixed with the Hang Seng up 1.8%, S&P e-mini flat and Nikkei down 1.7% and KOSPI -1.1%. Oil prices are lower with WTI -0.4% to $63.74/bbl. Copper is 0.1% higher.

- The US is closed for a holiday. Later ECB President Lagarde speaks and ECB’s Schnabel and Cipollone appear. European August manufacturing PMIs and euro area July unemployment are released.

JPY: Asia Wrap - USD/JPY Struggles Above 147.00

The Asia-Pac USD/JPY range has been 146.84-147.38, Asia is currently trading around 146.90, -0.10%. USD/JPY initially tried higher after the Japanese Fix, but ran into sellers and quickly fell back below 147.00. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00. The options market is showing signs of these JPY shorts beginning to buy strikes lower down to hedge themselves.

- (Bloomberg) --Leveraged investors are building positions in the options market that will benefit if Japan’s currency breaks free from its current narrow band of around 147 to the greenback and appreciate beyond 145, data from the Chicago Mercantile Exchange show.

- “Yen Shorts Are Running Out of Road as BOJ Hike Nears: USD/JPY’s downward path is set to accelerate at the start of a new trading month as big leveraged shorts will find it harder to justify their stance with an October BOJ rate hike looking increasingly likely. Especially as traders price for more rate cuts from the Federal Reserve.” - BBG

- MNI BRIEF: Japan Q2 Capex Lower; GDP Seen Revised Down. Bank of Japan officials are focused on the September Tankan survey due Oct 1 to assess the impact of tariffs on corporate profits and business plans, particularly capex. While demand for investment to ease labour shortages remains firm, global demand uncertainty is prompting some firms to delay implementation.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.35($310m).Upcoming Close Strikes : 146.50($1.39b Sept 3), 145.50($976m Sept 3) - BBG.

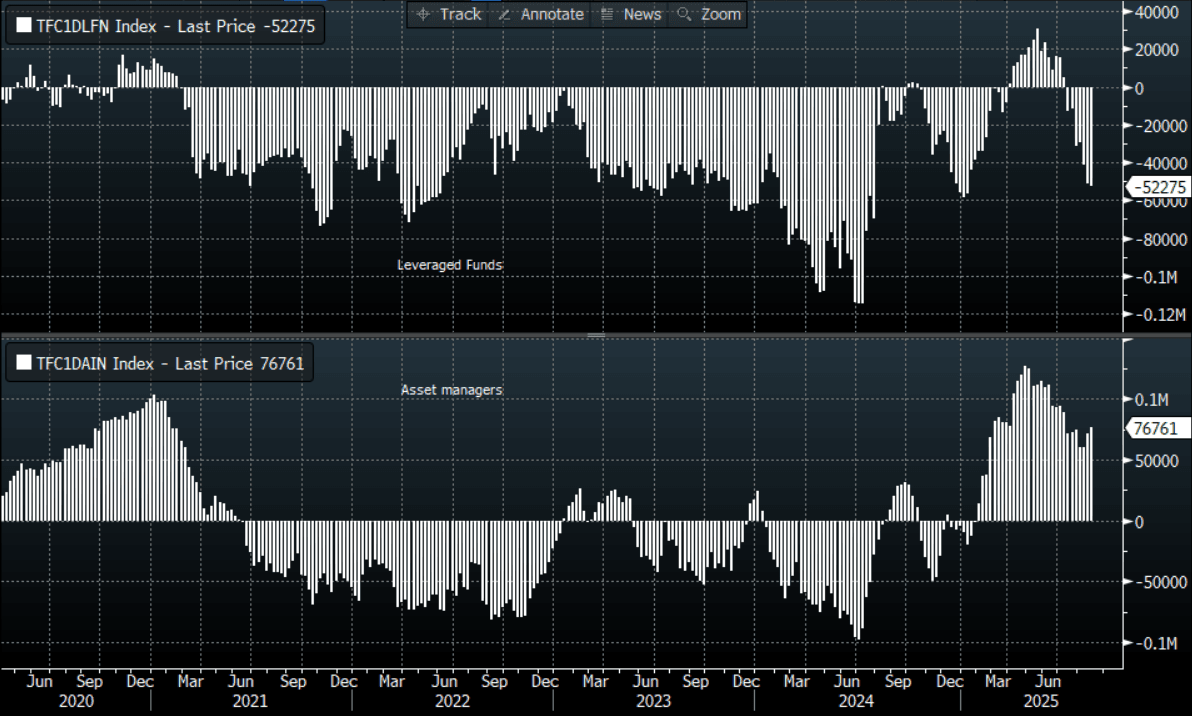

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Yields Firmer, Led By The Back End

Aussie bond futures sit lower for Monday trade, with the back end underperforming. XM (10yr futures)were last 95.655, off 4.5bps, while YM (3yr futures) we down 3bps to 96.56. US Tsy futures are weaker in the first part of Monday trade, although there is no cash trading today due to the US holiday later. On Friday the US cash Tsy curve finished steeper. The Fed's Daly gave some dovish remarks around the need to recalibrate policy soon.

- For cash ACGB yields, we are 2-6bps firmer across the benchmarks, with the back end leading. The 3 yr is up close to 3bps, last near 3.42%, while the 10 is +4bps, tracking above 4.31% .

- On the data front - Little Change In Q2 Inventories, Profits Remain Weak: Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday's Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1's 0.2% & 1.3%. July number of building approvals fell 8.2% m/m to be up 6.6% y/y after rising 12.2% m/m & 28% y/y in June.