BONDS: NZGBS: Closed Modestly Cheaper

NZGBs closed 1-2bps cheaper across benchmarks after a relatively subdued session.

- NZGBs underperformed the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials finishing 2bps wider.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- (Bloomberg) -- A La Niña watch is in effect with international guidance suggesting a 60% chance it will be established before Dec 31, Earth Sciences New Zealand says in an update.

- Swap rates closed flat to 4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. 34bps of easing is priced for October, with a cumulative 62bps by November 2025.

- Tomorrow, the local calendar will see Cotality Home Values.

- The NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 4.50% May-35 bond.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Lower, JGB Yields Edge Higher, BoJ Speech/10yr Supply Tomorrow

JGB futures have tracked lower in the first part of Monday trade. We were last at 137.34, -.20 versus settlement levels for the Sep future. We are close to session lows, while Aug 26 lows at 137.22 aren't too far away. Today's move reinforces the bearish bias for JGB futures.

- There is no US cash Tsy trading today, but futures have been tracking lower (10yr to 112-13, -03) and this follows a steeper end to last week for the 2/10s curve. The Fed's Daly struck a dovish tone, noting policy will have to be recalibrated soon late on Friday.

- On the data front, capex in y/y terms was above expectations, pointing to a resilient backdrop. However, the q/q outcome was up only 0.2%. The MOF survey, based on demand-side data, is a key input for calculating Q2 GDP revisions due Sept 8. It suggested capex will be revised lower from the preliminary +1.3%, which was based only on supply-side data. Other data showed softer sales and company profits momentum for Q2.

- In the cash JGB space, yields have ticked higher, with the belly of the curve leading. The 7yr yield is up 2.5bps to 1.395%, while the 10yr is around 1.62%, just off recent cycle highs. The 2/30s JGB curve is at +231bps so slightly flatter versus end August levels.

- Note tomorrow, we have BoJ Deputy Governor Himino speaking in Hokkaido, at 10:30am local time.

- A 10yr JGB debt sale also takes place.

FOREX: Asia FX Wrap - USD Heavy Just Above Support

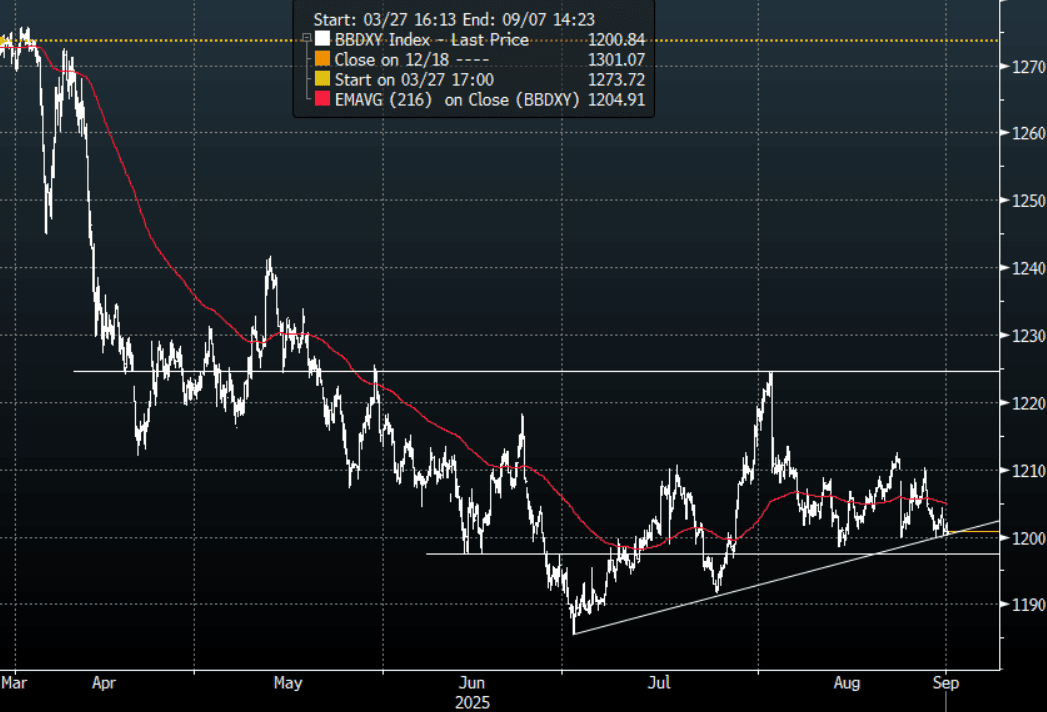

The BBDXY has had a range of 1200.08 - 1202.14 in the Asia-Pac session, it is currently trading around 1200, -0.05%. The USD remained broadly heavy on Friday night albeit still above its pivotal support. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is holding just above this support but continues to trade with a heavy tone. “Dollar to Drop More as Fed Independence Threats Deepen. The dollar is bearing the brunt of investor skepticism and is already adjusting to political and structural headwinds regardless of what the Fed does next.” - BBG

- EUR/USD - Asian range 1.1687 - 1.1714, Asia is currently trading 1.1710. The pair is trading sideways for the moment. First support is back towards 1.1550, a break back above 1.1850 needed to regain upward momentum.

- GBP/USD - Asian range 1.3497 - 1.3529, Asia is currently dealing around 1.3520. The pair is consolidating around the 1.3500 area. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1212-7.1296, the USD/CNY fix printed 7.1072, Asia is currently dealing around 7.1270. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.10%, Gold $3475, US TYZ5 112-13, BBDXY 1200, Crude Oil $63.73

- Data/Events : Italy HCOB Manf. PMI/Unemployment, EZ HCOB Manf. PMI/Unemployment, Germany HCOB Manf. PMI, France HCOB Manf. PMI, Spain HCOB Manf. PMI

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Grinding Above 0.5900

The NZD/USD had a range of 0.5890 - 0.5914 in the Asia-Pac session, going into the London open trading around 0.5905, +0.20%. The USD can’t catch a break and continues to trade heavy helping the NZD grind higher. The NZD has bounced off its support toward 0.5800, sellers should continue to be around looking to fade the move back towards the 0.5950 area initially. Should the USD break lower and gain momentum this would complicate this trade and then it would be prudent to rotate the NZD shorts into the crosses.

- Bloomberg - “New Zealand Opens Luxury Home Market to Golden-Visa Holders: New Zealand will loosen its ban on foreigners buying houses, opening the door for wealthy investors to purchase luxury properties as part of a push to revive its sluggish economy.”

- “The coalition government on Monday said it will allow holders of so-called golden visas to buy houses worth at least NZ$5 million ($3 million).”

- "NZ'S LUXON: I'VE GOT EVERY CONFIDENCE IN RBNZ, WAS RIGHT DECISION FOR RBNZ CHAIR QUIGLEY TO GO" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD500m Sept 2), 0.5700(NZD384m Sept 3) - BBG

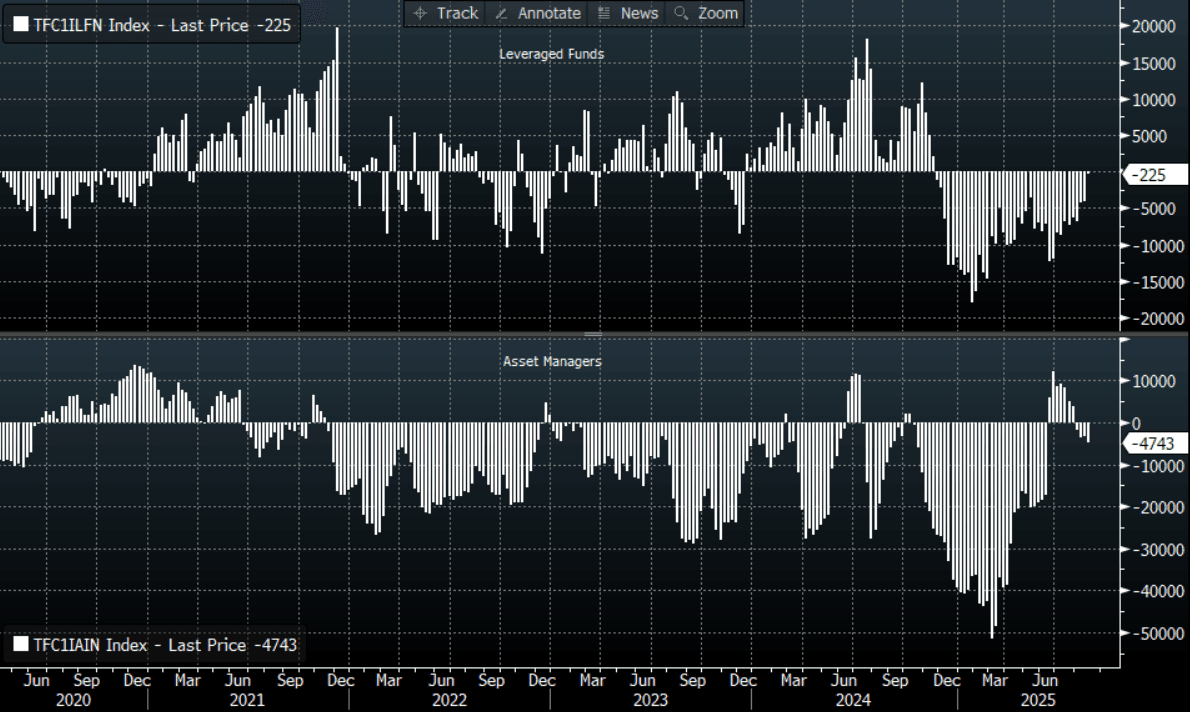

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1072 - 1.1110, currently trading 1.1080. Momentum higher looks to have stalled above 1.1100 for now, look for demand to return on a dip back towards the 1.1000 area.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P