MNI EUROPEAN MARKETS ANALYSIS: USD/JPY Higher Post Ueda

- The main focus today has been remarks by BoJ Governor Ueda, who hasn't given any hints of a Oct hike. USD/JPY is higher (challenging the 50-day EMA), while JGBs are higher, led by the back end. Earlier data showed softer Aug Japan labour market data as well.

- Elsewhere equity market sentiment was mostly positive, led by the tech side. US Tsy yields are slightly higher. Oil is up, but still tracking down sharply for the week.

- With the US government still shutdown, focus will be on the private sector releases this evening, with the services index out from ISM later. We also get the final PMI reads for services in the EU and US.

MARKETS

US TSYS: Slightly Cheaper As The Market Idles Through Shutdown

TYZ5 is dealing at 112-27+, -0-02 from closing levels in today's Asia-Pac session.

- According to MNI's technicals team, initial firm resistance to watch is at 113-00, the Sep 24 high. A break would be bullish with next levels to watch at: 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger).

- Cash bonds are dealing ~1bp cheaper in today's Aia-Pac session.

- US tsys saw small ranges on Thursday as US economic data began facing delays on the second day of the federal government shutdown, leaving investors without labour market readings for signals on the Federal Reserve's next steps.

- Friday's September employment report from the BLS most likely will NOT be released today despite Sen Warren (Dem) telling CNN the "labor data has been collected and is likely ready to be released". "Let's be clear," Warren added, "the jobs data scheduled to come out this Friday has undoubtedly been collected, and the President must release it."

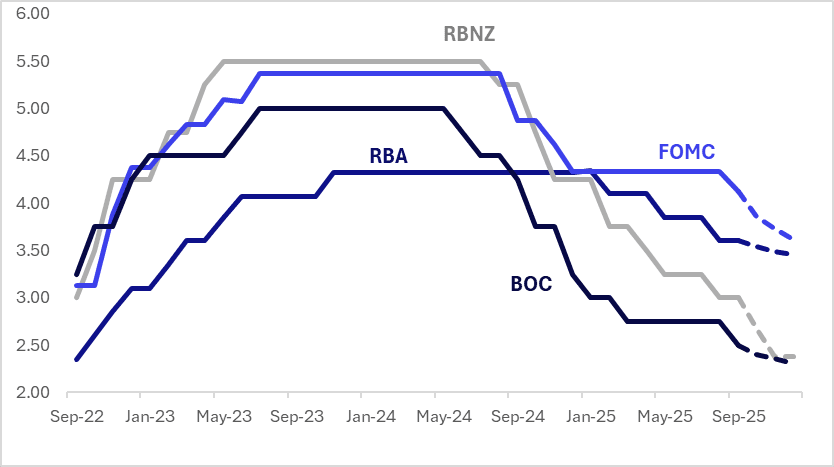

STIR: $-Bloc Pricing Little Changed Over Past Two Weeks, Except For AUS

Interest rate expectations across the $-bloc have shown little net change over the past two weeks, except in Australia, which firmed sharply (+15bps).

- In Australia, the RBA decided to leave rates at 3.6% in a unanimous vote, which was widely expected. Its tone was generally more cautious than in August and it is definitely keeping its options open regarding future decisions with Governor Bullock not committing to an easing or neutral bias.

- The Board is concerned that market services inflation could be sticky, as has occurred overseas, while there are “signs that private demand is recovering” and that the labour market is “stable”

- Given heightened uncertainty, the updated growth and inflation outlook in the November staff forecasts will be key for the next decision. The Board stated it will update “its view of the outlook as the data evolve” signalling that it is even more data dependent. Q3 CPI is published on 29 October and September jobs data on 16 October .

- Looking ahead, the next key regional event is the RBNZ’s policy decision on October 8, with market pricing indicating 33bps of easing.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing are as follows: US (FOMC): 3.62%, -51bps; Canada (BOC): 2.31%, -19bps; Australia (RBA): 3.45%, -15bps; and New Zealand (RBNZ): 2.39%, -61bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Long End Leads Rally, BOJ Ueda Fails To Signal Oct Hike

JGB futures are stronger, +12 compared to settlement levels.

- (MNI Brief) The BOJ will carefully weigh both upside and downside risks when judging the likelihood its baseline scenario will be realised, he added, stressing that decisions will be made "as appropriate and without any preconceptions." Bank of Japan Governor Kazuo Ueda on Friday highlighted three areas the central bank is closely monitoring when assessing Japan's economic activity and price trends, underscoring both upside and downside risks.

- "The first point concerns developments in overseas economies," Ueda told business leaders in Osaka. He noted that while global growth is expected to return to a moderate pace, the outlook could shift significantly depending on economic and policy developments in major economies, particularly the U.S.

- The second factor is how U.S. trade policies will affect Japanese firms' profits as well as their wage- and price-setting behaviour, Ueda said.

- Cash US tsys are cheaper in today's Asia-Pac session, with yields flat to 1bp higher.

- Cash JGBs are flat to 2.5bps richer across benchmarks. The benchmark 10-year yield is 0.4bp lower at 1.665% versus the cycle high of 1.674%, set yesterday following the poor auction.

- Swap rates are ~1bp lower.

- On Monday, the local calendar will be empty.

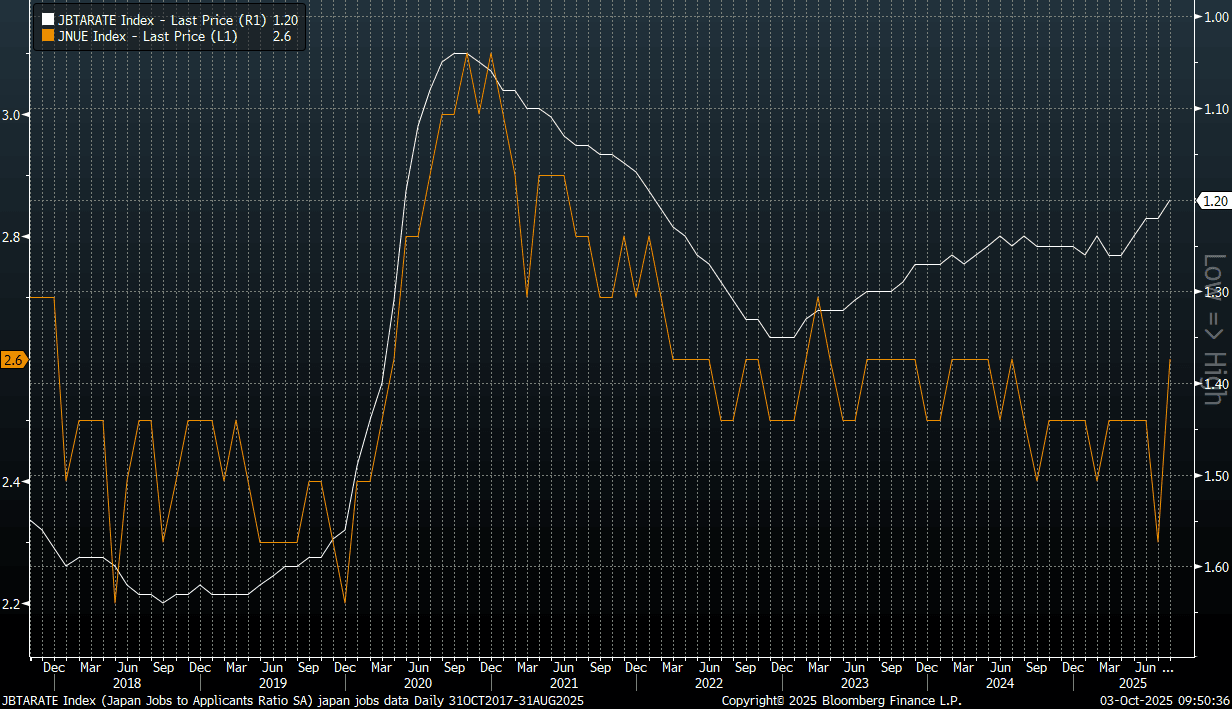

JAPAN DATA: Jobless Rate Pushes Up, Job To Applicant Ratio At Multi Yr Lows

The Japan August jobless rate rose more than forecast. It printed at 2.6% against a 2.4% forecast (while the July outcome was 2.3%). The 0.3ppt rise in m/m terms is notably, although it only takes us back to 2024 highs for the jobless rate. The job to applicant ratio eased to 1.20 form 1.22 in July (the market consensus had been for an unchanged 1.22 outcome).

- The chart below plots the job to applicant ratio (the white line), which is inverted on the chart, against the jobless rate. This is the lowest level for the job to applicant ratio since early 2022. There has been some divergence between the two series, with the job to applicant ratio generally painting a softer labor market picture in recent months. That wedge has now moderated to some degree.

- Job offers were down 3.6% in y/y terms, while new job offers fell by 6.2%y/y. The new jobs to applicant ratio fell to 2.15, just above recent lows.

- The number of people employed fell by 210k in m/m terms.

- The data points to some softening in labor market conditions, which at the margin may temper Oct hawkish BOJ expectations. Still, the jobless rate is low from an historical standpoint and therefore may still continue to support wage gains.

Fig 1: Japan Jobless Rate (Orange Line) & Job To Applicant Ratio (White Line, Inverted)

Source: Bloomberg Finance L.P./MNI

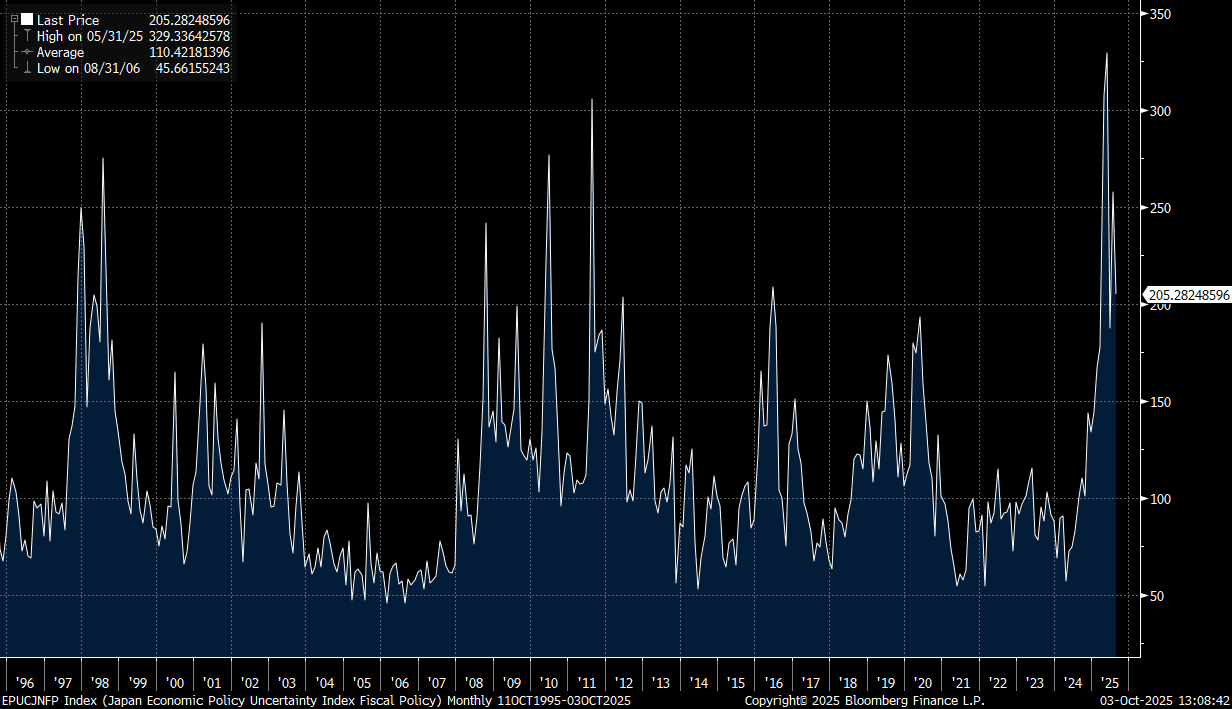

JAPAN: Markets Odds Favor Koizumi Victory, Policy Uncertainty Remains Elevated

Japan's LDP leadership election is held tomorrow. Market expectations appeared skewed towards Shinjiro Koizumi (current Agriculture, Forestry and Fisheries Minister) being elected as leader of the party. Per Polymarket, his election odds sit over 80, against those of Sanae Takaichi, the other potential candidate. Her odds have tracked lower from earlier highs (last 12).

- In a recent interview with Nikkei, Shinjiro Koizumi says that "It is important for the government and the Bank of Japan to share the same overall direction", and that "the government's economic policy and the Bank of Japan's monetary policy will work together to realise a virtuous cycle in the economy."

- Koizumi is seen as more of a centralist relative to Takaichi, who is a fiscal/BOJ dove (although has softened her BOJ stance).

- Still, Koizumi will look to pass the supplementary budget for 2025 as soon as possible if he wins the election (per Nikkei). This would be aimed combating inflation for households. Given the LDP doesn't have a majority in either house, coalition partners will be needed.

- This is likely to see fiscal policy uncertainty remain elevated to some degree. The chart below plots Japan economic policy uncertainty related to fiscal policy. We are off highs but still quite elevated from an historical standpoint. There is some relationship between such uncertainty and the shape of the JGB yield curve.

- The 2/30s JGB curve is off highs, but remains above +220bps, so still elevated from an historical standpoint. It may be markets are already factoring in a Kozimui victory to some extent.

- On the FX side, similar arguments could be made for USD/JPY, although this pair is up 0.30% so far today, last near 147.75, putting it above its 50-day EMA. Little commitment to an Oct hike by BoJ Governor Ueda earlier today has weighed on yen.

- J.P. Morgan note re the election around yen risks: "That the FX market currently appears to be pricing in little “Takaichi risk” suggests that the possibility of JPY-selling following a Takaichi victory could be relatively large, but...compared to last September, Takaichi is seen as less opposed to the BoJ hikes, which should limit JPY-selling. On net, if Takaichi wins, we think the knee-jerk USD/JPY rally is likely to be similar to or less than the+1% rise seen after the 1st round vote in last September’s presidential election. Since a victory by Koizumi (or Hayashi) seems to be largely expected by market participants, the knee-jerk JPY-buying in this case is likely to be much smaller than when Ishiba unexpectedly reversed the outcome in the 2nd round vote last year. "

Fig 1: Japan Fiscal Policy Uncertainty - Off Highs But Still Elevated

Source: Bloomberg Finance L.P/MNI

AUSSIE BONDS: Little Changed, Markets In A Wait & See Mode

ACGBs (YM -0.5 & XM -0.5) are little changed on a data light session.

- (Bloomberg) "Australia's official data out Friday showed the federal government's budget deficit came in at A$11.6b over the first two months of the 2025-26 financial year, some 21% narrower than forecast. That adds to the air of prudence when compared with data at the start of this week showing the measure at only 0.4% of GDP in the fiscal year ended June 2025, rather than the 1% forecast. That's a stark contrast to the US, which is running a 6.3% shortfall."

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after modest gains.

- Cash ACGBs are unchanged with the AU-US 10-year yield differential at +24bps.

- The latest ACGB May-32 supply achieved a weighted average yield that printed 0.58bp through prevailing mids. Moreover, the cover ratio increased significantly, falling to 3.3850x from 2.9267x.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 40% probability, with a cumulative 14bps of easing priced by year-end.

- On Monday, the local calendar will see Melbourne Institute Inflation.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday.

BONDS: NZGBS: Modestly Cheaper, Subdued Session As Markets Monitor US Lockdown

NZGBs closed 2bps cheaper after a relatively subdued data-light session.

- NZGBs have once again underperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 2-3bpswider on the day.

- US tsys are dealing ~1bp cheaper in today's Asia-Pac session.

- (Bloomberg) -- New Zealand and Australia are seeking to accelerate plans for a more ambitious Single Economic Market, Trade Minister Todd McClay says in an emailed statement ahead of a meeting with his Australian counterpart Don Farrell.

- Swap rates are flat.

- RBNZ dated OIS pricing is little changed across meetings. 33bps of easing is priced for October, with a cumulative 61bps by November 2025.

- The local calendar will see ANZ Commodity Prices on Monday.

FOREX: USD/JPY Rebounds As Ueda Doesn't Give Oct Hike Hint, Steady Elsewhere

Outside of some modest yen losses, the G10 FX backdrop has been relatively steady in the first part of Friday trade. The BBDXY index is little changed last near 1202.

- USD/JPY is back above 147.60, while session highs rest at 147.77. Current levels are close to the 50-day EMA (near 147.60), which we broke under earlier this week. Earlier data showed a softer tone to Japan's August labor market figures. The jobless rate rose by 0.3ppts to 2.6%, while the job to applicant ratio fell to fresh multi year lows.

- The bigger shift from USD/JPY came as BoJ Governor Ueda spoke. He stated the central bank will raise its policy interest rate if the outlook for economic activity and prices materialises as expected, while stopping short of signaling an imminent move. With about a month until the next policy meeting, Ueda gave no indication the BOJ was preparing to raise rates in October. The MNI Policy team reported this week better than expected September Tankan results raised the chances of a move at the Oct 29-30 meeting.

- For USD/JPY, holding above the 50-day EMA, could refocus attention on resistance at 149.69, the Sep 26 high and a bull trigger.

- Note as well we have the LDP leadership election tomorrow, where Koizumi is the firm favorite.

- Elsewhere, news and data flow has been quite light. EUR/USD sits near 1.1720/25, up a touch on end Thursday levels.

- AUD/USD remains under 0.6600, while NZD/USD is near 0.5820.

- Looking ahead, with the US government still shut (and therefore no payrolls release), the focus may rest with private sector surveys with the ISM services print out.

ASIA STOCKS: South Korea Inflows Surge On AI/Chip Optimism

Yesterday's standout from an inflow perspective was the +$2.2bn of net buying of South Korean stocks by offshore investors. This looks to be the strongest daily inflow on record (per BBG exchange data). It followed a +2.7% gain in the Kospi, to comfortably reach fresh cycle highs, with the index finishing up near 3550. Chip/AI sentiment surged for Samsung and SK Hynix, which came after a deal with OpenAI to supply chips for its Stargate project. For South Korea, net inflows are now back in positive territory for 2025 to date. Note South Korean markets are now out until next Friday.

- Taiwan also saw positive inflows, but in lower aggregate terms compared to South Korea. It's net flow picture for the past 5 trading days is just back into positive territory. It still leads South Korea from a 2025 inflow standpoint.

- Elsewhere, Indian flow momentum was very poor towards the end of Sep (with nearly $2bn in outflow in the last 5 trading days of the month). This matched the sharp retreat of local equity indices through this period, but we did start Oct better.

- Elsewhere trends were mixed in South East Asia. Indonesia and Thailand generally seeing outflow over the past week. Malaysia saw stronger inflows yesterday though, as offshore investors joined in on the local equity rise (+1%).

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 2271 | 2716 | 2089 |

| Taiwan (USDmn) | 779 | 8 | 8760 |

| India (USDmn)* | -453 | -1840 | -17453 |

| Indonesia (USDmn) | -85 | -163 | -3437 |

| Thailand (USDmn) | -6 | -118 | -2844 |

| Malaysia (USDmn) | 120 | 146 | -3586 |

| Philippines (USDmn) | -13 | -82 | -682 |

| Total (USDmn) | 2613 | 667 | -17153 |

| * Data Up To Sep 30 |

Source: Bloomberg Finance L.P./MNI

ASIA STOCKS: Most Markets Higher Led By Tech, China & South Korea Out

Most Asia Pac equity markets are trading with a positive tone in the first part of Friday trade. Note that China remains out, returning next Thursday, while South Korean markets are also closed today, returning next Friday. US equity futures have ticked higher, up 0.15-0.20%, with tech slightly outperforming. We remain close to benchmark highs for Eminis and Nasdaq futures. The US government shutdown has done little to upset sentiment in this space so far.

- Japan equities have been among the better performers in Friday trade. Both the Topix and Nikkei 225 are up over 1%. We are off recent record highs from Sep for both markets, but sentiment has likely been aided today by a BoJ speech from Governor Ueda, who didn't give any hints rates would be raised in Oct. USD/JPY has risen in response, although only by 0.30%. We also have the LDP leadership election tomorrow, with Koizumi, the current Agriculture, Forestry and Fisheries Minister the firm favorite. He is seen largely continuing Ishiba's tone around fiscal and monetary policy.

- A partnership for local tech company Hitachi with OpenAI has also boosted local tech related sentiment today.

- The surge higher in the US SOX index has provided further positive impetus to Taiwan's Taiex, which has risen a further 0.90% so far today. This puts the index at fresh record highs. Offshore investors added strongly to Taiwan stocks yesterday (although inflows into South Korea were stronger).

- Hong Kong is bucking these broader trends, with the HSI down 0.90%, although this follows a strong run up in late Sep/early Oct.

- In South East Asia, the tone is less positive, with Malaysia down slightly so far today. This follows a solid gain yesterday though. The index couldn't sustain earlier highs above 1650. Indonesian stocks are up modestly, while Thailand is close to flat.

COMMODITIES: Oil Set For Large Weekly Fall Ahead Of OPEC Meeting, Gold Off Highs

Benchmark oil prices have pared Thursday losses, but only marginally in the first part of Friday dealings. We sit comfortably lower for the week, with OPEC expected to continue to unwind previous output reductions when it meets. Gold is also lower, but still up for the week.

- The front month Brent contract was last near $64.40, up close to 0.50% so far today, but still down (over 8% at this stage). Current levels last prevailed in early June of this year (lows then were at $63/bbl).

- OPEC, which meets on Sunday, increased the October target by 137kb/d and at least that amount is likely in November although with conflicting reports on the size of a potential hike. Following the G7 finance ministers meeting, meanwhile, an agreement on substantial additional sanctions on Russia’s means to finance its war in Ukraine is close, Bloomberg said.

- WTI was last at $60.80/bbl. We haven't tested sub $60/bbl yet, but a clear break of this level would reinstate the downtrend, opening $57.50, the May 30 low.

- Gold is down around 0.4% at this stage, last near $3841. We look to be consolidating after breaking to fresh record highs yesterday ($3896.85). A steadier USD backdrop may be encouraging some short term profit taking in bullion.

ASIA FX: USD/PHP Back Under 58.00, Military Chief Pushes Back On Marcos Removal

Asian currencies have been mixed in the first part of Friday trade. Note China and South Korea are out until late next week, which has impacted liquidity throughout the region. Data flow has been light other than the Singapore PMI, and retail sales. Equity sentiment has been positive, but South East Asia has lagged stronger tech led gains in North Asia.

- USD/CNH has drifted a little higher, last above 7.1370, but is likely to remain range bound with no onshore anchor (absent a sharp broader USD move). USD/TWD is a little lower, last under 30.40, but remains within recent ranges. The currency continues to lag the stronger local/globally led tech equity tone.

- In South East Asia, USD/PHP is back under 58.00, fresh multi week lows. We have seen resistance above 58.30 in recent sessions. Domestic politics remains in focus, with earlier headlines that the head of the military rejected calls to unset President Marcos (via BBG). "The Philippines’ military chief said he rejected calls by some retired officers for the armed forces to remove President Ferdinand Marcos Jr." This comes amid on-going corruption concerns around projects in flood impacted areas.

- USD/IDR has edged a little higher, but remains close to 16600. USD/THB is firmer, but at 32.45/50 remains under recent highs (32.52). USD/MYR is also higher, last around 4.2150.

- USD/SGD is firmer, last around 1.2900. Earlier the PMI rose to 56.4 from 51.2 in Aug. Retail sales also just printed, slightly better than expected at 5.2%y/y, versus 4.8% forecast. This follows a softer run of data since mid Sep, when exports, IP and CPI were below expectations.

- The MAS policy announcement is scheduled soon, with BBG noting the release window from the start of next week to the 14th of Oct.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/10/2025 | 0645/0845 | * | Industrial Production | |

| 03/10/2025 | 0700/0300 | * | Turkey CPI | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0800/1000 | * | Retail Sales | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/10/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/10/2025 | 0900/1100 | ** | EZ PPI | |

| 03/10/2025 | 0940/1140 | ECB Lagarde Speech At Knot Farewell Symposium | ||

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson |