US TSYS: Slightly Cheaper As The Market Idles Through Shutdown

TYZ5 is dealing at 112-27+, -0-02 from closing levels in today's Asia-Pac session.

- According to MNI's technicals team, initial firm resistance to watch is at 113-00, the Sep 24 high. A break would be bullish with next levels to watch at: 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger).

- Cash bonds are dealing ~1bp cheaper in today's Aia-Pac session.

- US tsys saw small ranges on Thursday as US economic data began facing delays on the second day of the federal government shutdown, leaving investors without labour market readings for signals on the Federal Reserve's next steps.

- Friday's September employment report from the BLS most likely will NOT be released today despite Sen Warren (Dem) telling CNN the "labor data has been collected and is likely ready to be released". "Let's be clear," Warren added, "the jobs data scheduled to come out this Friday has undoubtedly been collected, and the President must release it."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

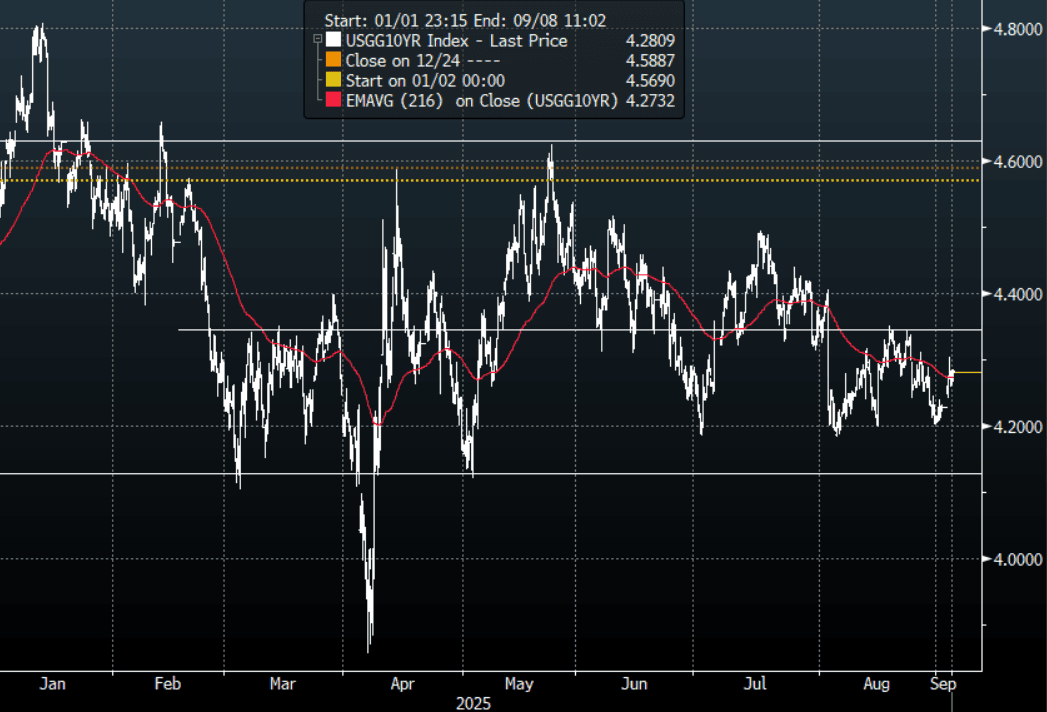

US TSYS: Yields Edge Higher

The TYZ5 range has been 112-03 to 112-08+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-00+ from the previous close.

- The US 2-year yield has edged higher trading around 3.65%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.281%, up 0.02 from its close.

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. The price action in the long-end looks pretty dire, the 4.35/4.40% area needs to hold for the longs to remain in control.

- Bessent to Start Fed Chair Interviews on Friday -- WSJ. "There are 11 contenders for the job, according to Bessent and his advisers. Among them are Fed governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett and former Fed governor Kevin Warsh. Following the interviews, Bessent plans to recommend a final list of candidates to President Trump.”

- Bob Elliott on X: “If you shift to easing when inflation is nearly 4% and rising, there are consequences(the UK). JP & the FOMC should take note.”

- Robin Brook on X: “The 30-year yield is rising everywhere, even though the world's central banks are in an easing cycle. That's the best indication that rising long yields are due to a global debt glut, the answer to which is to get lax fiscal policy under control. Not lean on your central bank...”

- Data/Events: MBA Mortgage Applications, Wards total Vehicle Sales, JOLTS, Factory Orders, Durable Goods Orders, Fed Beige Book

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

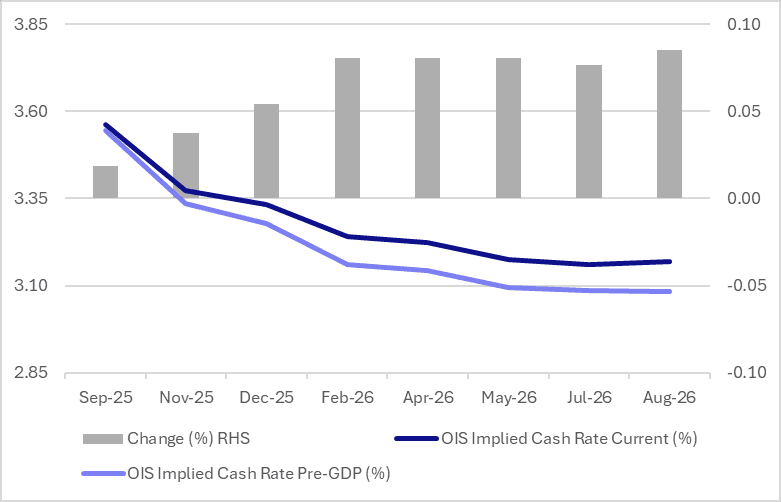

AUSSIE BONDS: Yields Surge, Led By Front End, Q2 GDP Beats, RBA Gov Speaks Later

ACGB yields are higher across the benchmarks. The move started with the back end when onshore markets opened, which was consistent with global developments. However, as the session progressed, front end yields have outperformed, aided by the Q2 GDP beat. A better China services PMI read has also likely aided these moves.

- The 2 and 3yr bond yields are both up around 9bps. This puts the 3yr benchmark close to 3.54%, which is close to mid July highs. Beyond this region note that mid May highs were around 3.69%.

- The 10yr yield is up 7bps to 4.425%, which is also tracking towards mid July highs. The ACGBS 3/10s curve is slightly flatter at +89bps though, bucking the generally steeper trends seen globally.

- Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook.

- RBA dated OIS contracts have shunted higher, led by 2026 dates. We are 2-9 bps firmer versus pre GDP levels, see the chart below. A Sep cut has little chance priced in while a Nov cut is around 75% priced in.

- For futures we have sunk to fresh lows, 3yr (YM) to 96.44, off 9.5bps, while 10yr futures (XM) are down 7.5bps to 95.54.

- Coming up in a few hours at 6pm AEST we have RBA Governor Bullock speaking.

Fig 1: RBA Dated OIS Higher Post Q2 GDP

Source: Bloomberg Finance L.P./MNI

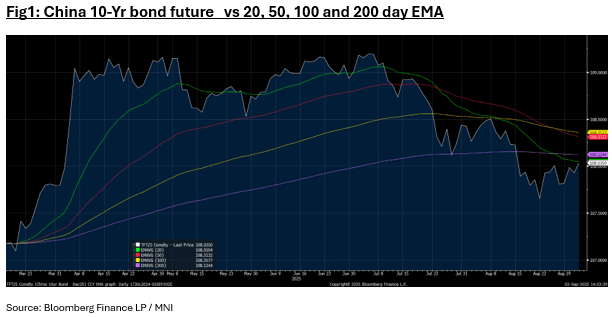

CHINA: Bond Futures Regain Yesterday's Losses

- China's bond futures are up strongly this morning to recoup yesterday's losses.

- The 10-Yr is up +0.10 at 108.03 following yesterday's losses of -0.05

- The rally sees the 10-Yr near to the 20-day EMA of 108.05, which it hasn't trade above since early July.

- The 2-Yr bond future is up +0.03 to 102.43 and is near to the 50-day EMA of 102.44 which it last traded above in early July.

- Bonds are stronger today with the 10-Yr lower by -1bp to 1.76%