BONDS: NZGBS: Modestly Cheaper, Subdued Session As Markets Monitor US Lockdown

NZGBs closed 2bps cheaper after a relatively subdued data-light session.

- NZGBs have once again underperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 2-3bpswider on the day.

- US tsys are dealing ~1bp cheaper in today's Asia-Pac session.

- (Bloomberg) -- New Zealand and Australia are seeking to accelerate plans for a more ambitious Single Economic Market, Trade Minister Todd McClay says in an emailed statement ahead of a meeting with his Australian counterpart Don Farrell.

- Swap rates are flat.

- RBNZ dated OIS pricing is little changed across meetings. 33bps of easing is priced for October, with a cumulative 61bps by November 2025.

- The local calendar will see ANZ Commodity Prices on Monday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

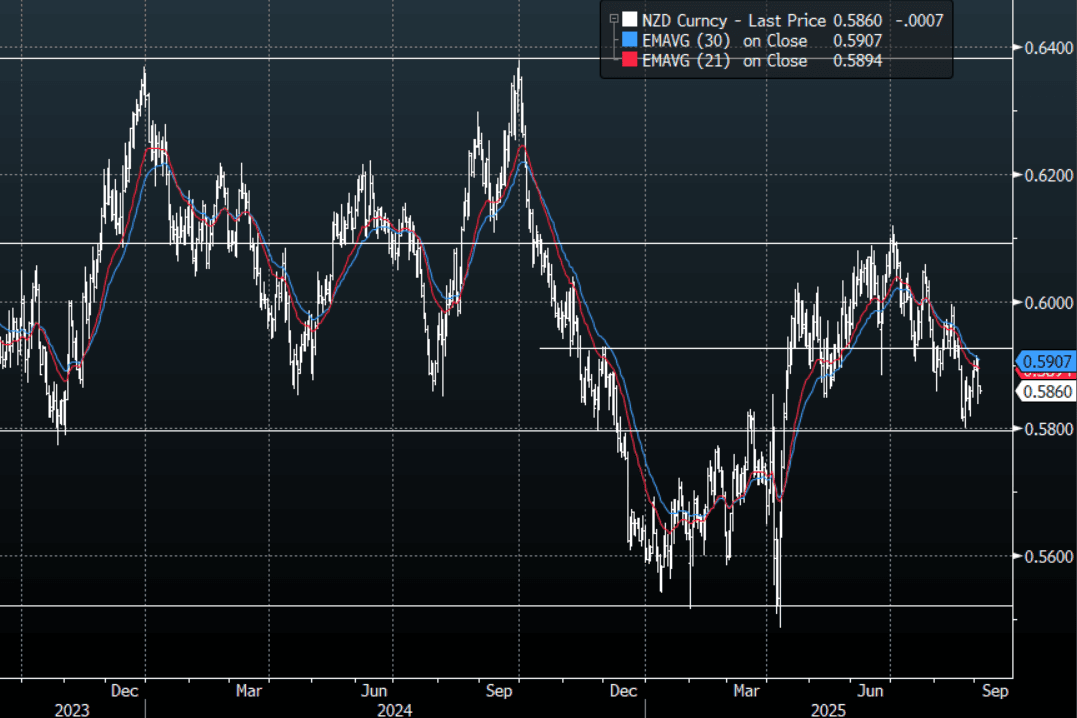

NZD: Asia Wrap - NZD/USD Drifts Lower After Rejecting 0.5900

The NZD/USD had a range of 0.5854 - 0.5867 in the Asia-Pac session, going into the London open trading around 0.5860, -0.12%. The NZD topped out above 0.5900 and moved lower with risk overnight. The NZD sellers should continue to be around looking to fade any bounce back towards the 0.5950 area initially. The USD finding some demand finally has helped put a top in above 0.5900 for now, though NFP on Friday will have a say in if that remains the case.

- Milk Power Auction Price Falls, Back To Late 2024 Levels : Overnight the average price for whole milk powder fell to $3809 versus $4036 at the previous auction, per GDT . This was a 5.3% drop. The whole milk powder price is now at fresh lows for 2025. The terms of trade proxy has matched this fall recently.

- "S&P Is Watching New Zealand’s Current Account, Budget Deficits. S&P Global Ratings is “comfortable” with New Zealand’s sovereign rating outlook, though it’s closely watching the nation’s current account and budget deficits." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD384m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1112 - 1.1138, currently trading 1.1125. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

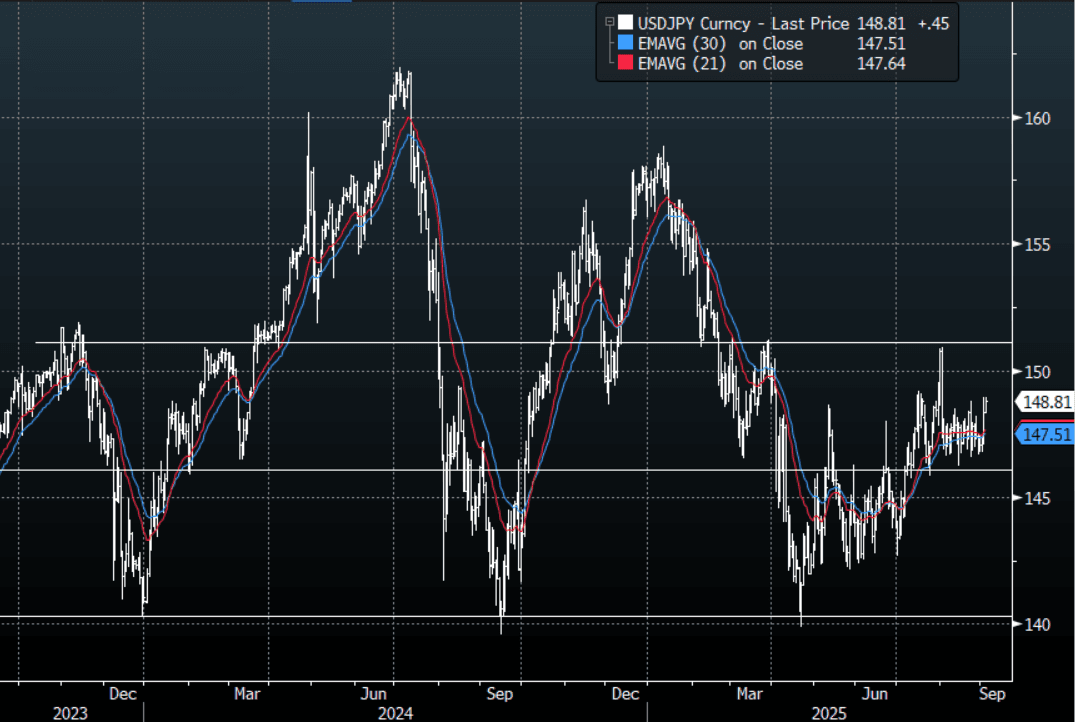

JPY: Asia Wrap - USD/JPY Back To Overnight Highs On A Potential Early Election

The Asia-Pac USD/JPY range has been 148.36-148.92, Asia is currently trading around 148.85, +0.32%. USD/JPY was bid all session moving back toward the overnight highs on a potential early election and 30-Year JGB’s blowing out to 3.28%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. The price action looks pretty constructive but I would not be expecting any major extensions until the market has had a look at the NFP on Friday unless we get some other catalyst, could an early election be that ?

- Bloomberg - “Japan’s Long Bonds Join Global Slide as Politics Adds to Jitters. Yields on 20-year government bonds rose to 2.69%, the highest level since 1999, while those on the 30-year maturity jumped to 3.28%, the highest since debut.”

- "USD/JPY’s Upward Tilt Encouraged With LDP Early Election Report. USD/JPY is ticking higher after a report the LDP’s Aso is set to call for an early election. This comes as PM Ishiba’s tenure is looking vulnerable following news of a key ally’s intention to step down." - BBG

- “JAPAN LDP'S ASO SET TO CALL FOR EARLY PARTY ELECTION: MAINICHI" - BBG

- “S&P Global Japan Aug. Services PMI 53.1 vs 53.6 in July, S&P Global Japan Aug. Composite PMI 52 vs 51.6 in July" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.15($870m), 146.50($1.39b).Upcoming Close Strikes : 147.10($970m Sept 4), 146.00($2.16b Sept 5) - BBG.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Gold Retreats From New Record, Benefiting From Risk Appetite Pullback

Gold prices reached a new record high of $3546.96/oz during today’s APAC trading as risk appetite deteriorated. They usually move in the opposite direction to the US dollar but today (BBDXY +0.1%) and yesterday (BBDXY +0.5%) they have rallied despite USD strength. Expectations of Fed easing and concerns over attacks on central bank independence from the US administration have driven bullion higher, while the greenback appears to be normalising with its risk premium declining (calculated by Bloomberg).

- US yields are also higher again which would normally weigh on non-interest bearing gold but currently it appears that markets are nervous regarding rising government debt levels not just in the US, but also the UK and France.

- Gold is currently little changed on the day at $3533.5/oz. It broke above resistance at $3539.7 earlier today.

- Silver in contrast to gold is down 0.4% to $40.72/oz off the intraday low of $40.642.

- Equities are mixed with the S&P e-mini up 0.1% and TAIEX +0.3% but CSI 300 down 0.9% and ASX -1.6%. Oil prices are lower with WTI -0.3% to $65.41/bbl. Copper is 0.3% lower.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.