FOREX: USD/JPY Rebounds As Ueda Doesn't Give Oct Hike Hint, Steady Elsewhere

Outside of some modest yen losses, the G10 FX backdrop has been relatively steady in the first part of Friday trade. The BBDXY index is little changed last near 1202.

- USD/JPY is back above 147.60, while session highs rest at 147.77. Current levels are close to the 50-day EMA (near 147.60), which we broke under earlier this week. Earlier data showed a softer tone to Japan's August labor market figures. The jobless rate rose by 0.3ppts to 2.6%, while the job to applicant ratio fell to fresh multi year lows.

- The bigger shift from USD/JPY came as BoJ Governor Ueda spoke. He stated the central bank will raise its policy interest rate if the outlook for economic activity and prices materialises as expected, while stopping short of signaling an imminent move. With about a month until the next policy meeting, Ueda gave no indication the BOJ was preparing to raise rates in October. The MNI Policy team reported this week better than expected September Tankan results raised the chances of a move at the Oct 29-30 meeting.

- For USD/JPY, holding above the 50-day EMA, could refocus attention on resistance at 149.69, the Sep 26 high and a bull trigger.

- Note as well we have the LDP leadership election tomorrow, where Koizumi is the firm favorite.

- Elsewhere, news and data flow has been quite light. EUR/USD sits near 1.1720/25, up a touch on end Thursday levels.

- AUD/USD remains under 0.6600, while NZD/USD is near 0.5820.

- Looking ahead, with the US government still shut (and therefore no payrolls release), the focus may rest with private sector surveys with the ISM services print out.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Retreats From New Record, Benefiting From Risk Appetite Pullback

Gold prices reached a new record high of $3546.96/oz during today’s APAC trading as risk appetite deteriorated. They usually move in the opposite direction to the US dollar but today (BBDXY +0.1%) and yesterday (BBDXY +0.5%) they have rallied despite USD strength. Expectations of Fed easing and concerns over attacks on central bank independence from the US administration have driven bullion higher, while the greenback appears to be normalising with its risk premium declining (calculated by Bloomberg).

- US yields are also higher again which would normally weigh on non-interest bearing gold but currently it appears that markets are nervous regarding rising government debt levels not just in the US, but also the UK and France.

- Gold is currently little changed on the day at $3533.5/oz. It broke above resistance at $3539.7 earlier today.

- Silver in contrast to gold is down 0.4% to $40.72/oz off the intraday low of $40.642.

- Equities are mixed with the S&P e-mini up 0.1% and TAIEX +0.3% but CSI 300 down 0.9% and ASX -1.6%. Oil prices are lower with WTI -0.3% to $65.41/bbl. Copper is 0.3% lower.

- Today the Fed’s Musalem speaks and the Beige Book is published. US July JOLTS job openings & orders, European August services/composite PMIs and July euro area PPI print. Also, ECB President Lagarde, RBA Governor Bullock and BoE Breeden speak.

AUD: Asia Wrap - AUD/USD Fails To Push Higher On GDP

The AUD/USD has had a range of 0.6513 - 0.6525 in the Asia- Pac session, it is currently trading around 0.6520, +0.02%. The AUD tried to bounce on the better GDP data but could not follow through and has drifted back to its open. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Q2 Boosted By Special Factors, H1 Averaged 0.4% q/q. Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook

- "S&P Global Australia Aug. Composite PMI 55.5 vs 53.8 Prior (pre 54.9), S&P Global Australia Aug. Services PMI 55.8 vs 54.1 in July(pre 55.1).” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD569m). Upcoming Close Strikes : 0.6400(AUD1.12b Sept 5), 0.6500(AUD974m Sept 5), 0.6600(AUD1b Sept 5) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

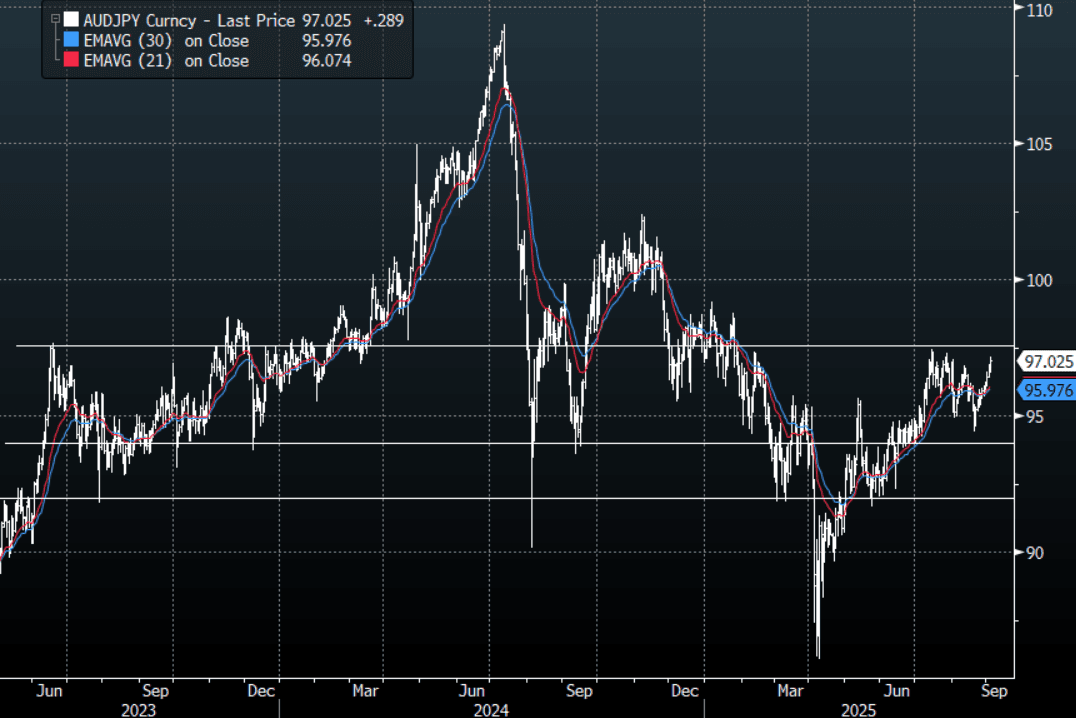

- AUD/JPY - Asia-Pac range 96.59 - 97.15, Asia is trading around 97.00. The pair has broken back above 96.50 which starts to negate the downward direction, a sustained break above 97.50 is needed to reignite the upward trend. Until then looks to be 94.50 - 97.50.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

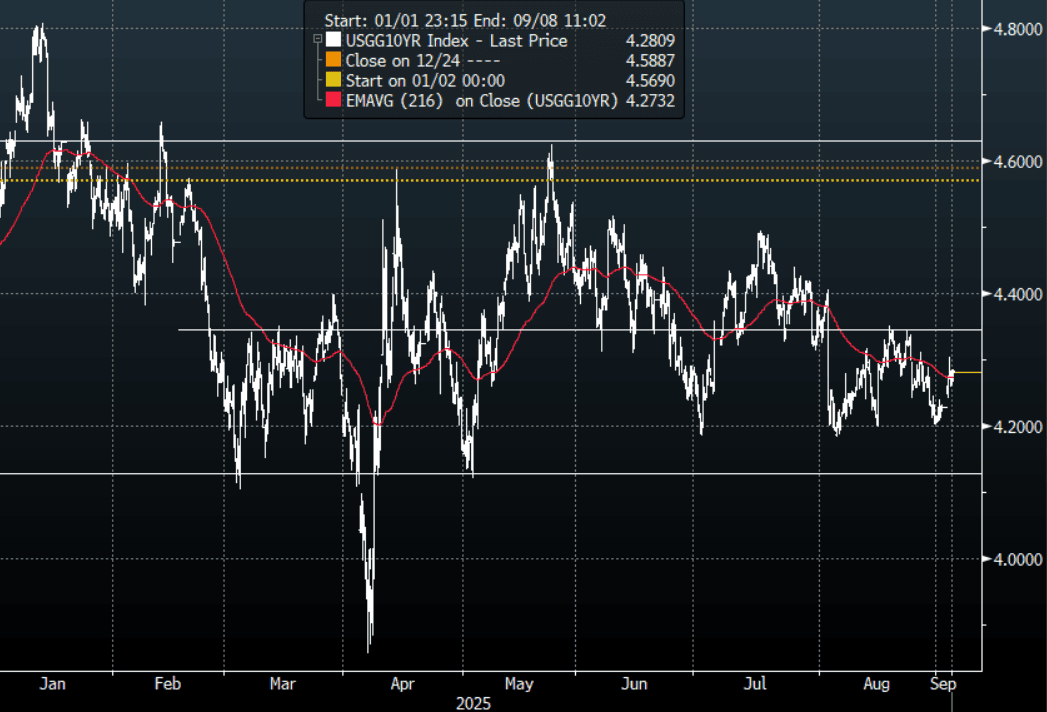

US TSYS: Yields Edge Higher

The TYZ5 range has been 112-03 to 112-08+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-00+ from the previous close.

- The US 2-year yield has edged higher trading around 3.65%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.281%, up 0.02 from its close.

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. The price action in the long-end looks pretty dire, the 4.35/4.40% area needs to hold for the longs to remain in control.

- Bessent to Start Fed Chair Interviews on Friday -- WSJ. "There are 11 contenders for the job, according to Bessent and his advisers. Among them are Fed governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett and former Fed governor Kevin Warsh. Following the interviews, Bessent plans to recommend a final list of candidates to President Trump.”

- Bob Elliott on X: “If you shift to easing when inflation is nearly 4% and rising, there are consequences(the UK). JP & the FOMC should take note.”

- Robin Brook on X: “The 30-year yield is rising everywhere, even though the world's central banks are in an easing cycle. That's the best indication that rising long yields are due to a global debt glut, the answer to which is to get lax fiscal policy under control. Not lean on your central bank...”

- Data/Events: MBA Mortgage Applications, Wards total Vehicle Sales, JOLTS, Factory Orders, Durable Goods Orders, Fed Beige Book

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P