MNI EUROPEAN MARKETS ANALYSIS: USD Extends Lower

- Trump tariff comments (will set unilateral tariff rates within the next two weeks) has weighed on US equity futures and the USD.

- USD/JPY is back under 144.00, US Tsy yields are also down. Middle East tensions have kept oil prices close to recent highs.

- In Australia, Melbourne Institute consumer inflation expectations for June jumped to 5.0% from 4.1%, the highest and first print above 5% in almost two years.

- Later on, US May PPI & jobless claims and UK April IP/GDP print. ECB’s de Guindos, Schnabel and Elderson speak.

MARKETS

US TSYS: Asia Wrap - Yields Extend Lower

The TYU5 range has been 110-19+ to 110-26+ during the Asia-Pacific session. It last changed hands at 110-23, up 0-01 from the previous close.

- The US 2-year yield has edged lower, dealing around 3.937%, down 0.01 from its close.

- The US 10-year yield has moved lower, trading around 4.405%, down 0.2 from its close.

- CBS - “Israel informed U.S. officials that it is fully ready to launch an operation into Iran”. https://www.cbsnews.com/news/israel-is-poised-to-launch-operation-on-iran-sources-say/

- (Bloomberg) - Given the softer-than-expected May CPI report, investors are turning their focus to the forward reflationary impact of tariffs and long-end supply. The convergence of those factors points to continued steepening of the yield curve.

- “JD Vance said the Fed’s refusal to cut rates is “monetary malpractice.”(BBG)

- “Bessent: Removing SLR in Past Had Substantial Yield Effect.”(BBG)

- The 10-year yield has fallen overnight and could go back to test its 4.30/35% support, this area needs to hold if the shorts are to get their wish of a push higher in yields.

- Data/Events: PPI, Initial Jobless claims

JGBS: Modest Rally, Subdued Dealing, US 30Y Auction Later Today

JGB futures (JBU5) are stronger, +8 compared to settlement levels, hovering near Tokyo session highs.

- Japan’s bond futures had initially weakened after today’s enhanced liquidity auction of 15.5 - 39-year JGBs, but quickly reversed direction.

- (Bloomberg) -- Japan’s super-long bonds face the risk of higher volatility from rising foreign holdings, just as demand is absent from local life insurers, according to Morgan Stanley MUFG Securities. Foreign investors can sell to take profit when yields drop, and they can also choose to sell to cut losses, macro strategist Koichi Sugisaki told reporters at a briefing in Tokyo on Thursday.

- “Given that Ishiba could hold a summit with US President Donald Trump in Canada, he met with other party leaders to hear their opinions.” (BBG)

- Cash US tsys are ~2bps richer in today's Asia-Pac session with Middle East tensions in focus. US officials have been told Israel is fully ready to launch an operation into Iran. Investors will also be closely watching demand at today’s $22bn sale of 30-year bonds amid souring demand for that tenor.

- Cash JGBs are modestly richer across benchmarks, with the 5-year leading.

- Swap rates are ~1bp lower, with swap spreads wider.

- Tomorrow, the local calendar will see IP, Capu and Tertiary Industry data.

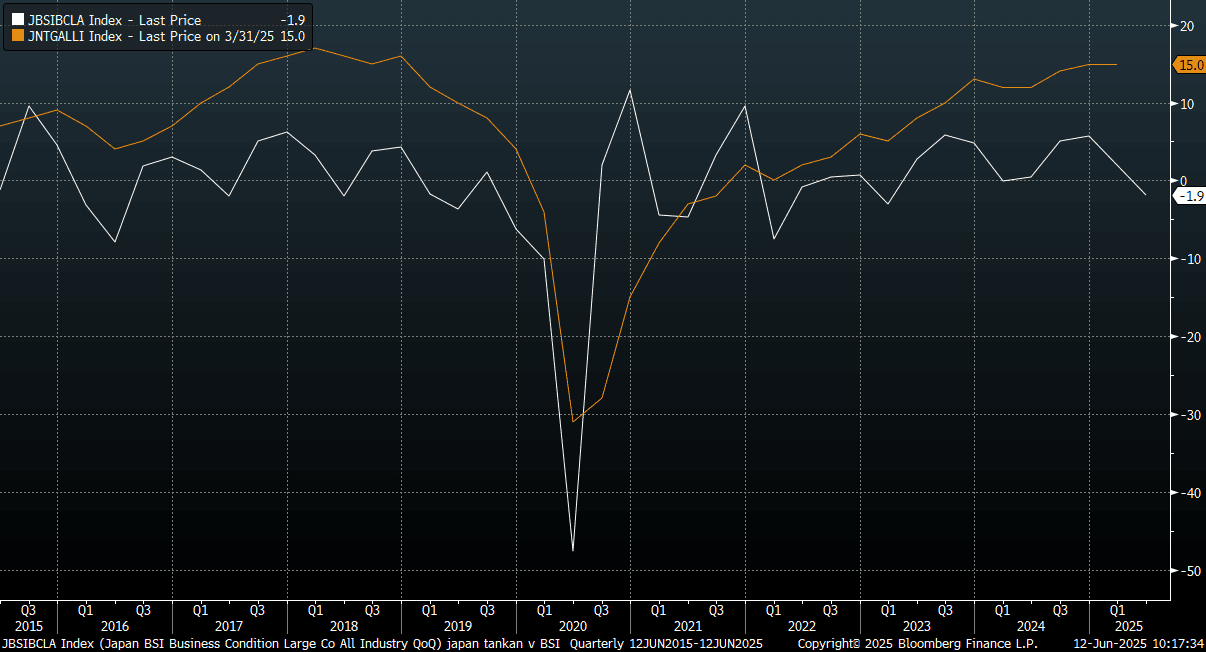

JAPAN DATA: BSI Q2 Survey Falls, Hinting At Softer Domestic Conditions

Japan's Q2 BSI gauge fell for both all industry and large manufacturing. The all industry reading was -1.9, from +2.0 in Q1. The large manufacturing read is now at -4.8 from -2.4 in Q1.

- For the all industry segment, we are now at lowest levels since early 2023. The reading tends to be more volatile than the more closely followed Tankan survey. The chart below plots the BSI all industry index against the Tankan all industry diffusion index (which is the orange line on the chart).

- Still, the BSI read is hinting at softer economic conditions. "Japan’s 2Q domestic economic conditions fell -6.2 ppt" (via BBG), versus +3.1 in Q1. This reading was for all industries.

Fig 1: Japan BSI All Industry Business Conditions & Tankan All Industry Index

Source: MNI - Market News/Bloomberg Finance L.P

JAPAN DATA: Local Investors Dump Offshore Equities

The most notable feature of last week's investment flows was strong selling by local Japan investors of offshore equities. At nearly -¥1.5trln in net selling, it was the largest outflow from this segment since early Nov 2022. It also marked the fourth straight week of selling for offshore equities. Still, including this period, since the start of 2025, cumulative inflows rest near +¥5trln YTD. Recent selling goes against the generally positive global equity trends since in recent weeks.

- Local investors also sold offshore bonds for a second straight week, however, this only partially offsets the strong net buying seen since early May.

- In terms of inbound flows to Japan, we had net buying of local stocks from offshore investors for the 10th straight week, albeit in reduced size compared to May weekly averages.

- We also saw further inflows into local bonds, but again this was at a reduced pace compared to end May.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending June 6 | Prior Week |

| Foreign Buying Japan Stocks | 180.2 | 336.1 |

| Foreign Buying Japan Bonds | 219.8 | 1165.4 |

| Japan Buying Foreign Bonds | -458.6 | -118.0 |

| Japan Buying Foreign Stocks | -1489.0 | -1144.1 |

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Holding Richer On A Subdued Data-Light Session

ACGBs (YM +5.0 & XM +5.0) remain stronger after dealing in narrow ranges in today's data-light Sydney session.

- (MNI) There has been a moderate improvement in housing affordability with prices soft in Q4 and Q1, a strong rise in Q1 disposable income and mortgage rates lower, which should fall further with more RBA easing expected.

- However, affordability remains 40% below trend, only slight progress from the worst at 42.8% in Q3 2024. Structural issues in the sector persist.

- Cash US tsys are ~2bps richer in today's Asia-Pac session with Middle East tensions in focus.

- Cash ACGBs are 5bps richer with the AU-US 10-year yield differential at -18bps.

- The bills strip has bull-flattened, with pricing +1 to +6.

- RBA-dated OIS pricing is 1-7bps softer across meetings today. A 25bp rate cut in July is given an 82% probability, with a cumulative 76bps of easing priced by year-end.

- Today, the local calendar was empty. A speech from RBA Jacobs, Head of Domestic Markets Department - Australia's Bond Market in a Volatile World - at the Australian Government Fixed Income Forum, Tokyo (1720 AEST).

- Tomorrow, the local calendar will be empty.

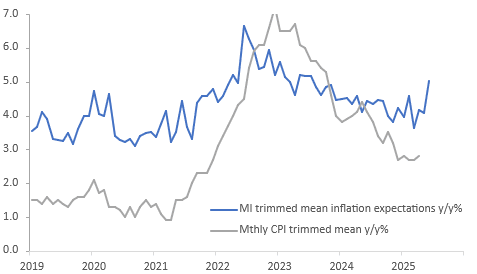

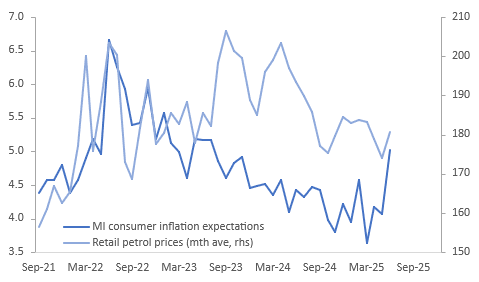

AUSTRALIA DATA: Inflation Expectations Highest Since 2023

Melbourne Institute consumer inflation expectations for June jumped to 5.0% from 4.1%, the highest and first print above 5% in almost two years. They were 4.4% in June 2024. They reached a trough in March of 3.6% and have been higher since likely boosted by concerns over the impact of US tariffs on inflation and higher petrol prices since then. The RBA will likely only be concerned if elevated inflation expectations and the causes persist and risk changing wage-setting behaviour.

Australia trimmed mean CPI vs MI consumer inflation expectations y/y%

- Factors that may have driven the jump in inflation expectations include April monthly CPI data printing higher than expected at the end of May. Also national petrol prices have risen in each of the last three weeks to their highest level since late March. The first week of June was 3.9% higher than the May average price.

Australia MI inflation expectations % vs retail petrol prices

Source: MNI - Market News/LSEG/Australian Institute of Petroleum

- However, the June Westpac consumer confidence report showed signs of less concern about price pressures with 63% assessing news reports around inflation as “unfavourable” down 2pp since March and 13pp since December.

- There are other signs of a stabilisation of disinflation with monthly core inflation not moderating since December and wage growth picking. The announcement of the 3.5% minimum wage increase on July 1 may have also boosted expectations even though it is the lowest since 2021.

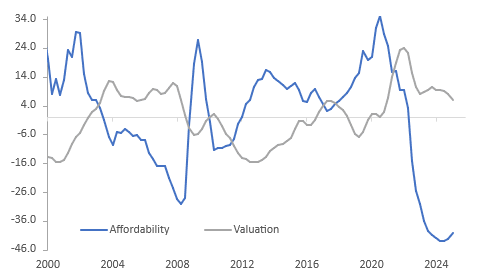

AUSTRALIA: Gradual Progress On Housing Affordability Helped By Numerous Factors

There has been a moderate improvement in housing affordability with prices soft in Q4 and Q1, a strong rise in Q1 disposable income and mortgage rates lower, which should fall further with more RBA easing expected. However, affordability remains 40% below trend, only slight progress from the worst at 42.8% in Q3 2024. Housing also remains overvalued but the degree has declined. Structural issues in the sector persist with working age population growth picking up again while building approvals have weakened.

- Housing affordability was up 4.5% y/y in Q1 and is currently on track to rise by around 7.5% y/y in Q2, which would see the index rise to around 38% below trend. The Q2 average of Cotality home values is up 1.0% q/q but the annual rate has moderated to 2.8% from 3.8% and the 11.1% peak in Q1 2024.

Australia housing affordability vs valuation % deviation from trend

- Rental growth has also moderated with Q1 at 5.5% y/y down from 6.4% y/y and the 7.8% y/y peak in Q1 2024. As home price inflation has slowed more than rents, valuation is down 1.6% y/y but still 6.1% above trend down from 24.1% in Q1 2022.

- Demand remains solid with working-age population rising around 50k/month in 2025 and growth rising 2.6% y/y in April up from 2.4% and the July/August 2024 trough of 1.7% y/y.

- Q1 real residential investment rose 2.6% q/q, the strongest quarterly rate since Q1 2021, to be up 5.6% y/y. But the number of dwelling building approvals fell for the third straight month in April driven by the volatile multi-unit component but growth in private houses has also slowed.

- This is consistent with the sales of new homes falling 10.6% y/y in April with only NSW seeing an increase.

Australia building approvals y/y%

BONDS: NZGBS: Bull-Flattener, Card Spend Weak, US Tsys Bid On M/E Tensions

NZGBs closed showing a bull-flattener, with benchmark yields 1-5bps lower, after soft retail card data.

- NZ card transactions remained soft in May with retail sales falling 0.2% m/m to be up 0.2% y/y after -0.6% y/y helped by positive base effects. Although the RBNZ doesn’t have a bias with rates in the neutral range, it is monitoring data and events very closely, and this release is signalling weak Q2 consumption.

- Today’s supply was greeted with solid bid-to-cover ratios: 4.30x (May-30) and 3.22x (May-36).

- Nevertheless, the NZ-US 10-year yield differentials closed 2bps wider. At +17bps, the differential sits in the top half of the -20bp to +40bps range seen this year.

- Cash US tsys are ~2bps richer in today's Asia-Pac session with Middle East tensions in focus. US officials have been told Israel is fully ready to launch an operation into Iran.

- Swap rates closed showing a twist-flattener, with rates 1bp higher to 1bp lower.

- RBNZ dated OIS pricing closed flat to 2bps softer across meetings, with early 2026 leading. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- Tomorrow, the local calendar will see BusinessNZ Manufacturing PMI data, ahead of the Performance Services Index on Monday.

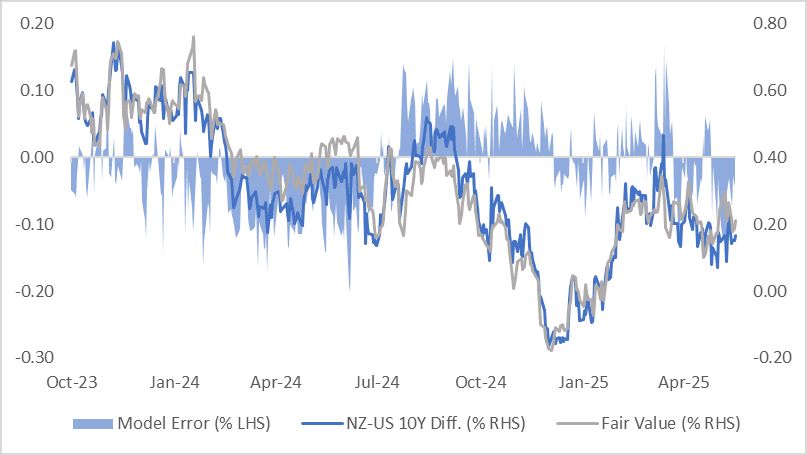

BONDS: NZ-US 10Y Diff In Top Half Of 2025's Range

NZGBs are currently showing a bull-flattener, with benchmark yields 3-5bps lower. The NZGB 10-year has slightly underperformed the US 10-year since yesterday’s close, with the NZ-US yield differentials 3bps wider.

- At +17bps, the NZ-US 10-year differential is in the top half of the -20bp to +40bps range seen this year.

- Moreover, a simple regression analysis of the 3-month forward swap rate spread (1Y3M) over the past 18 months indicates the 10-year yield differential is around 4bps below its estimated fair value of +21bps.

- Notably, the regression error has fluctuated within a range of ±15bps over the past year, highlighting some variability in the relationship.

- The 1Y3M differential continues to be a key driver of market expectations for long-term yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

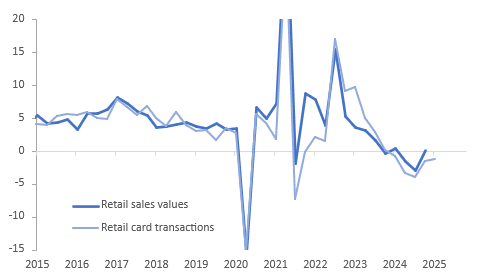

NEW ZEALAND: Soft Q2 Retail Card Transactions

NZ card transactions remained soft in May with retail sales falling 0.2% m/m to be up 0.2% y/y after -0.6% y/y helped by positive base effects. While the total rose 0.3% m/m, it had declined the previous four months, and is now up 0.2% y/y. 3-month momentum deteriorated for both series. Although the RBNZ doesn’t have a bias with rates in the neutral range, it is monitoring data and events very closely and this release is signalling weak Q2 consumption.

- Q2 average retail transactions are down 0.5% q/q to be up 0.2% y/y, strongest since Q4 2023, after -0.2% q/q & -1.2% y/y in Q1. Annual growth over April/May is suggesting the gradual recovery continued but remains soft. Nominal retail sales rose 1.5% q/q and 1.3% y/y in Q1.

- The weakness was impacted by lower fuel prices as the data is nominal. Fuel sales fell 2.4% m/m. There was a large rise in motor vehicle sales +2.6% m/m. Core retail transactions fell 0.2% m/m in May.

- Non-retail rose 1.5% m/m (including medical, travel and post), while services were down 0.2% m/m.

NZ retail sales y/y%

FOREX: Asia FX Wrap - The USD Extends Move Lower

The BBDXY has had a range of 1203.48 - 1205.99 in the Asia-Pac session, it is currently trading around 1204. CBS - “Israel informed U.S. officials that it is fully ready to launch an operation into Iran”. The USD has extended its losses in Asia and is testing some long term levels against a broad basket of currencies.

- EUR/USD - Asian range 1.1487 - 1.1529, Asia is currently trading 1.1515. EUR has continued to push higher during the Asian session in response to the move lower in US stocks. Dips should continue to find demand, first support around 1.1400 then the 1.1100/1200 area. EUR/USD is challenging the pivotal 1.1500 area, a sustained break could signal a larger move higher. see graph below.

- GBP/USD - Asian range 1.3547 - 1.3593, Asia is currently dealing around 1.3580. The GBP found solid demand towards 1.3450 and is now again attempting to gain some momentum to push above the pivotal 1.3500/1.3600 weekly pivot.

- USD/CNH - Asian range 7.1804 - 7.2002, the USD/CNY fix printed 7.1803. Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.35%, Gold $3372, US 10-Year 4.406%, BBDXY 1204, Crude oil $67.94

Data/Events : Italy Unemployment, Ger Current Account

Fig 1: EUR/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

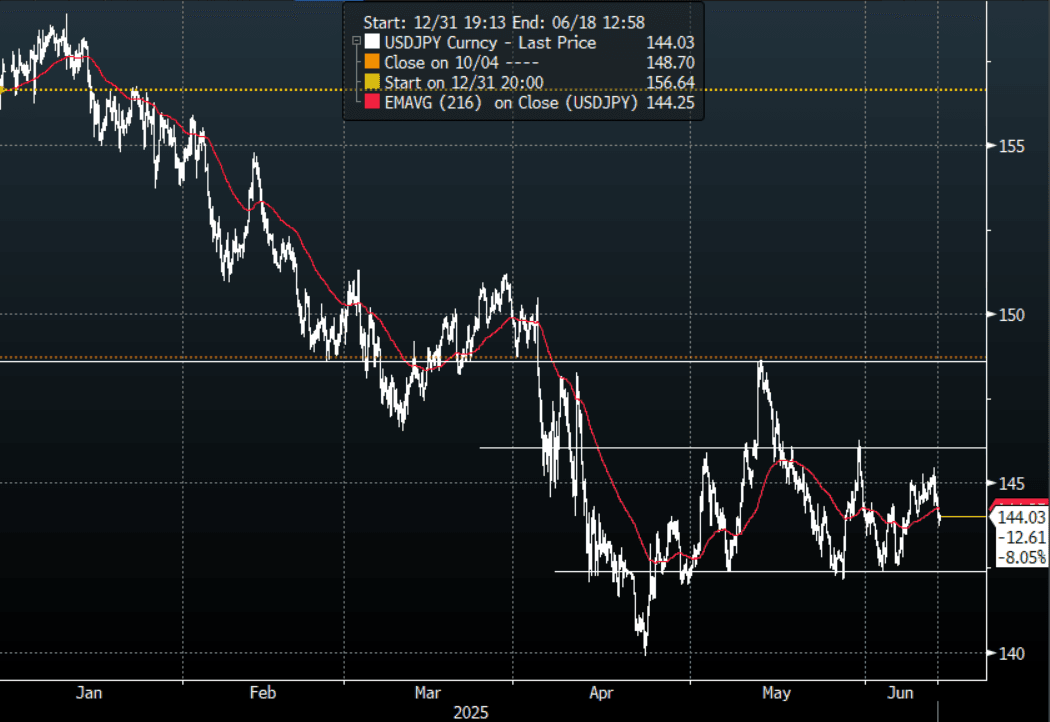

JPY: Asia Wrap - USD/JPY Back Under Pressure

The Asia-Pac USD/JPY range has been 143.73 - 144.56, Asia is currently trading around 144.00. USD/JPY has been under pressure for most of the Asian session as US yields and Stocks both continue to drift lower.

- Local Investors Dump Offshore Equities: The most notable feature of last week's investment flows was strong selling by local Japan investors of offshore equities. At nearly -1.5trln in net selling, it was the largest outflow from this segment since early Nov 2022. It also marked the fourth straight week of selling for offshore equities.

- (Bloomberg) - “Pimco said long-dated JGBs look “really interesting” as a tactical trade after 30-year yields topped 3.2% for the first time in May.”

- Overnight USD/JPY collapsed after the CPI print and has continued to trade heavy in our session straight from the open. With US yields under pressure and the risk backdrop souring you would think the path of least resistance would be a move lower.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. Price action does suggest 142.00 is likely to be tested first.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.00($1.28bm). Upcoming Close Strikes : 144.00($1.27b June 13), 145.00($4.87b June 16).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD Under Pressure, Best Expressed In The Crosses

The AUD/USD has had a range of 0.6484 - 0.6511 in the Asia- Pac session, it is currently trading around 0.6500. The AUD has been under pressure for most of our session as the move higher in risk seems to be stalling. Some good demand was seen today back towards the 0.6480 area once more. The AUD/USD is struggling for direction as the USD continues to be put under pressure at the same time, the AUD though is a clear underperformer against the crosses.

- RBA: VIEW: Softer Inflation Outlook Drives Westpac’s Rate Forecast Down. While Westpac continues to expect the RBA to be on hold in July with the next cut in August coinciding with updated staff forecasts, it is now forecasting the trough in the cash rate at 2.85% in May although it could be March if inflation and the labour market disappoint.

- “The arguments in favor of doing more than 50bps more (two cuts) are building. In particular, the outlook for inflation is shifting in the face of slowing population growth and a handover from public to private sector demand growth that is looking shakier”

- “It is possible that some of these cuts come a bit faster than the ‘cautious’ path we currently have penciled in”

- The AUD continues to see demand just below the 0.6500 area, but the inability to break above 0.6550 on multiple occasions will have the bulls a little concerned.

- Price remains in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend. AUD underperformance continues to be better expressed against the crosses.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD643m). Upcoming Close Strikes : 0.6500(AUD 447m June 13), 0.6450(AUD426m June 16)

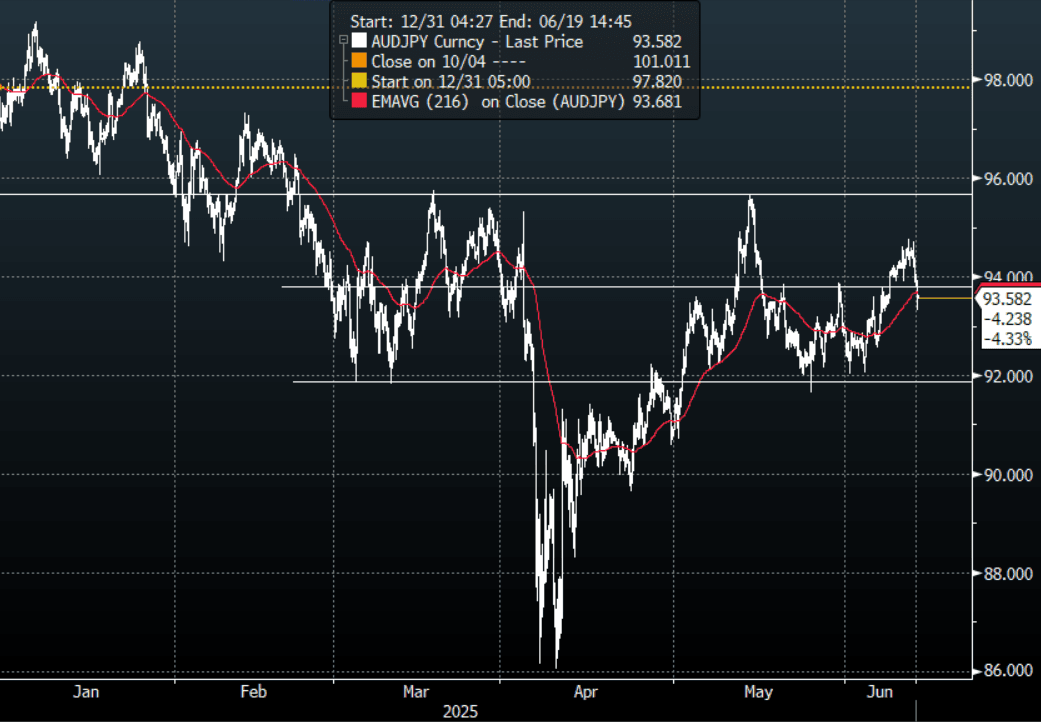

AUD/JPY - Today's range 93.31 - 94.06, it is trading currently around 93.60. Price has turned quickly lower again with the first whiff of risk turning down. We are back below the level it was trading pre NFP, if this pair closes down here it will put in a lower high. A break back below 91.50/92.00 is needed to reignite the momentum lower.

Fig 1: AUD/JPY spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

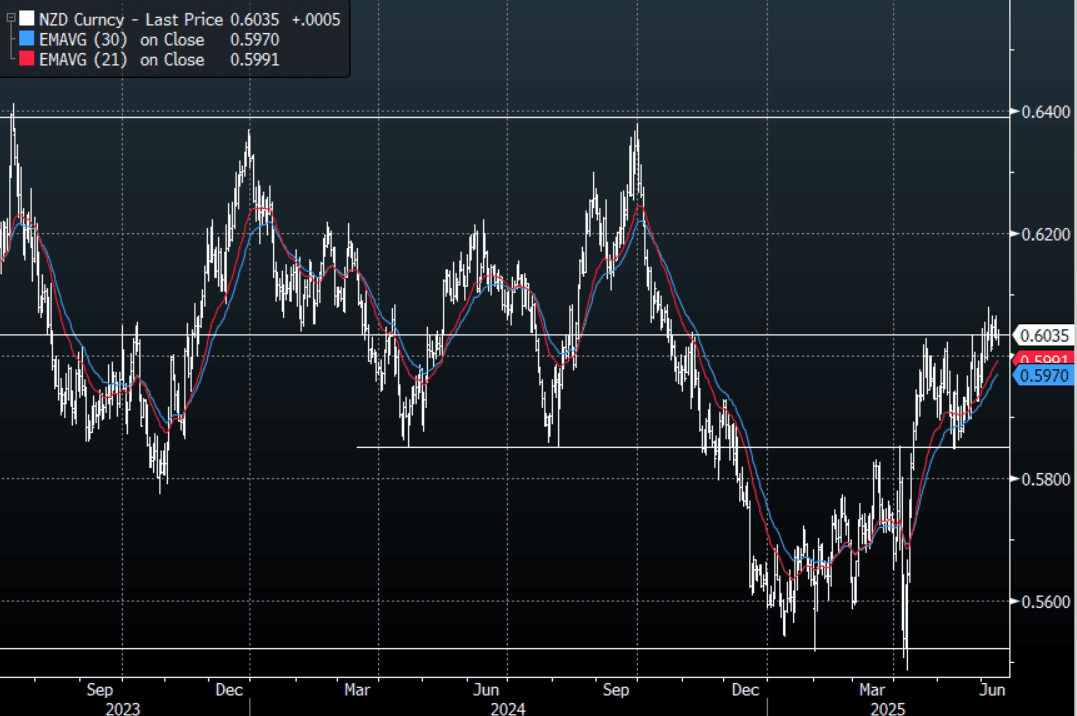

NZD: Asia Wrap - NZD/USD Holds Above 0.6000, Underperforms In The Crosses

The NZD/USD had a range of 0.6016 - 0.6040 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has bounced off support back towards the 0.6000 area as the USD remains under big pressure. The NZD/USD is struggling for direction as risk is turning lower at the same time, the crosses look a better place to express the NZD underperformance.

- Soft Q2 Retail Card Transactions. NZ card transactions remained soft in May with retail sales falling 0.2% m/m to be up 0.2% y/y after -0.6% y/y helped by positive base effects. While the total rose 0.3% m/m, it had declined the previous four months, and is now up 0.2% y/y. The 3-month momentum deteriorated for both series. Although the RBNZ doesn’t have a bias with rates in the neutral range, it is monitoring data and events very closely and this release is signalling weak Q2 consumption.

- Westpac Sees Gradual Consumption Recovery Later In 2025. Westpac notes that spending has moved sideways over the last three months but expects it to improve over H2 2025 with mortgages rolling over improving disposable incomes but the recovery in consumption is still likely to be gradual.

- The NZD’s inability to accelerate above 0.6050 has seen the move higher stall in the short term, first support is seen back towards the 0.5950 area. The NZD underperformance is being seen in the crosses.

- While the support around 0.5850 holds there should be buyers around on dips. A clear break above 0.6050/0.6100 is needed to provide the spark for the next leg higher.

AUD/NZD range for the session has been 1.0769 - 1.0794, currently trading 1.0770. A top looks in place now just above 1.0900, the cross topped out on Monday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends, US Futures Lower, Kospi Outperformance Continues

Asian equities are mixed in the first part of Thursday trade. Aggregate moves are not beyond 1% at this stage, with pockets of strength and weakness evident in both North East and South East Asia.

- US equity futures are weaker since markets re-opened. Eminis were last down around 0.30%. We saw a brief dip sub the 6000 level, but that was supported. Earlier headlines from US President Trump that he will decide on unilateral tariff rates within the next two weeks has been a headwind for sentiment. Some sell-side analysts see this a negotiating tactic to hasten trade deals. Trump added (via RTRS): "He said the U.S. would send out letters in one to two weeks outlining the terms of trade deals to dozens of other countries, which they could embrace or reject."

- The other focus point for markets is Middle East tensions, with US personnel being moved out of parts of the Middle East, including Iraq. Iran threatens to target US bases if nuclear talks fail, heightening fears of military conflict, Reuters said.

- Japan markets are down modestly, the Topix off 0.20%, the NKY 225 down 0.50%, with a firmer yen backdrop evident on market risk aversion.

- The Hang Seng is down around 0.50%, while the CSI 300 is close to flat in onshore China markets.

- The Kospi continues its outperformance, the benchmark index up a further 0.80%, which is fresh highs back to early 2022 (last near 2930). Optimism remains strong around new President Lee's ambitions to boost value, while the BOK is also encouraging fresh fiscal stimulus, stating it won't impact inflation.

- In Taiwan, the Taiex is off around 0.65%, ending a recent strong run higher.

- In SEA, we are seeing weakness in Thailand and Indonesian stocks. Consumer sentiment readings for both economies fell in May, while in Thailand growth concerns remain amid the tariff threat and slower tourism backdrop. The SET was last down around 0.55%.

ASIA STOCKS: Equity Inflows Continue For South Korea/Taiwan

The table below outlines offshore Asia equity flows for yesterday, the past week and 2025 to date. We continued to see net inflows into South Korea and Taiwan.

- Taiwan has played catch up in recent sessions, aided by Taiex gains, with TSMC sales for May boosting optimism around broader tech/AI sentiment.

- For South Korea, yesterday's visit by President Lee to the Korea Exchange underscores the important of stock market outcomes for the new government.

- Indeed today, with North East Asia equities struggling amid weaker US futures, the Kospi continues to rally, making fresh multi year highs. With still around -$8bn in net outflows in 2025 to date, we could see further catch up in this space.

- Indian flows were positive on Tuesday, while trends in other markets were close to flat yesterday.

Table 1: Asian Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 273 | 3205 | -8001 |

| Taiwan (USDmn) | 577 | 3043 | -10545 |

| India (USDmn)* | 360 | 588 | -10178 |

| Indonesia (USDmn) | 5 | -175 | -2946 |

| Thailand (USDmn) | -7 | 0 | -2135 |

| Malaysia (USDmn) | 2 | -65 | -2539 |

| Philippines (USDmn) | -1 | -14 | -527 |

| Total (USDmn) | 1208 | 6582 | -36869 |

| * Data Up To June 10 |

Source: Bloomberg Finance L.P. / MNI

OIL: Crude Holds Most Of Yesterday’s Gains But Worried About Trade Again

Oil has held onto most of Wednesday’s gain declining only slightly during today’s APAC session. WTI is down 0.3% to $67.92/bbl following a low of $67.62, while Brent is -0.4% to $69.49/bbl after falling to $69.22, back below resistance at $70.08. The USD index is down 0.3% providing some support to dollar-denominated crude.

- Oil prices surged on Wednesday driven by the lower-than-expected May US CPI, likely US-China trade deal, a large US crude drawdown and rising geopolitical tensions in the Middle East. The US has reduced staff at its Iraqi embassy in the face of threats from Iran to attack US bases in the Middle East if there is a conflict.

- While President Trump doesn’t think he can persuade Iran to give up on its nuclear ambitions, talks are due to continue in Oman on Sunday. Iran is believed to be preparing a new proposal ahead of the summit. An easing in tensions would likely see a material decline in oil prices.

- The market is focusing on trade tensions again, which it has feared for some time would weigh on global energy demand. Trump said that tariff letters with unilateral duties would be sent in the next fortnight, which has increased trade nerves. The current delay ends on July 8.

- US May PPI & jobless claims and UK April IP/GDP print. ECB’s de Guindos, Schnabel and Elderson speak.

Gold Benefits From Geopolitical Worries & Weaker US Dollar

Gold prices rose a further 0.5% to $3372.2/oz as geopolitical worries continued to drive safe haven flows. They are off the intraday high of $3377.82, which remained below resistance at $3403.5. The weaker US dollar (USD BBDXY -0.3%) and yields continued to support non-interest bearing gold after data showed lower-than-expected US inflation in May.

- The US withdrawal of some of its embassy staff in Baghdad due to security concerns and President Trump’s statement that tariff letters would be sent in the next fortnight drove an increase in flight-to-quality flows.

- Silver is up 0.3% to $36.36, in line with today’s move in bullion and close to the intraday high of $34.40. Initial resistance is at $36.89, 9 June high.

- Equities have been mixed today with KOSPI up 0.8%, CSI 300 flat but Hang Seng down 0.5% and S&P e-mini -0.3%. Oil prices are lower with WTI -0.3% to $67.93/bbl and copper is up 0.1%.

- Later the focus will be on the 30-year US Treasury auction with a face value of $22bn. Weak demand will signal reduced confidence in longer-dated US debt and likely increase flows into gold. The US’ fiscal position in the face of tax cuts has worried markets recently.

- US May PPI & jobless claims and UK April IP/GDP print. ECB’s de Guindos, Schnabel and Elderson speak.

INDONESIA: Weak Q2 Sentiment Suggests Slowdown In Consumption

Consumer confidence fell sharply in May to its lowest since September 2022, Bank Indonesia’s tightening cycle had begun the month before. Despite a 25bp rate cut in May, sentiment fell to 117.5 from 121.7 with the weakness broad-based across current conditions and expectations. Subdued disposable income growth and cost-of-living pressures have weighed on sentiment which is signalling a slowdown in Q2 spending. The next BI decision is June 16 and it’s likely to be on hold.

Indonesia consumption

Source: MNI - Market News/LSEG

- Confidence fell 3.5% m/m in May with expectations also down 0.6% m/m likely impacted by current heightened global uncertainty related to US tariffs. The assessment of economic conditions was down 6.7% m/m, suggesting a difficult current environment which is likely due to both domestic and global developments.

- On the one hand, the S&P Global manufacturing PMI has printed below the breakeven 50-mark for two consecutive months, auto sales fell in three out of four months in 2025 and Q1 GDP showed a slowing in growth which is expected to continue.

- On the other hand, the PMI showed optimism around the outlook with a pickup in hiring, April tourist arrivals rose strongly with the annual rate at 14%, retail sales are recovering rising 5.5% y/y in March and export growth is holding up at about 7.5% y/y 3-mth average supported by solid growth to China. Import growth has risen over 2025 suggesting solid domestic demand.

ASIA FX: SEA FX Firmer, But Lags Parts Of NEA

In South East Asia FX markets, the skew has been towards USD losses, but we haven't seen moves to the same extent compared with KRW and TWD gains. Both Thailand and Indonesia have seen dips in consumer confidence for May.

- For Thailand, confidence in terms of the headline measure and for economic conditions, are back to early 2023 levels. This continues to place a cloud of the domestic outlook. The SET equity index is struggling so far today, but this isn't impacting THB. USD/THB is back to 32.45/50, up around 0.5% in baht terms. This is back close to recent lows near 32.39. Broader USD softness, coupled with gold price gains, have been clear THB positives.

- For USD/IDR we are down around 0.20%, last near 16225/30. late May lows were close to 16150 in the pair, so we remain above those levels at this stage. The consumer sentiment read for Indonesia fell to its lowest since September 2022 and points to slowing consumption growth.

- USD/MYR is tracking lower, last at 4.2260, up around 0.25% in MYR terms. Like other pairs in the region, we remain above recent lows, which were marked just under 4.2000. USD/SGD is closer to such a test, last near 1.2820 (late May lows were close to 1.2800).

- Philippines markets have been off today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/06/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 12/06/2025 | 0600/0700 | ** | Trade Balance | |

| 12/06/2025 | 0600/0700 | ** | Index of Services | |

| 12/06/2025 | 0600/0700 | *** | Index of Production | |

| 12/06/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/06/2025 | 0900/1100 | ECB Schnabel Visits "House of the Euro" | ||

| 12/06/2025 | - | *** | Money Supply | |

| 12/06/2025 | - | *** | New Loans | |

| 12/06/2025 | - | *** | Social Financing | |

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI | |

| 12/06/2025 | 1400/1000 | * | Services Revenues | |

| 12/06/2025 | 1415/1615 | ECB Elderson At Senior Supervisors Conference | ||

| 12/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 12/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/06/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/06/2025 | 2301/0001 | ** | KPMG/REC Jobs Report | |

| 13/06/2025 | 0430/1330 | ** | Industrial Production | |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade |