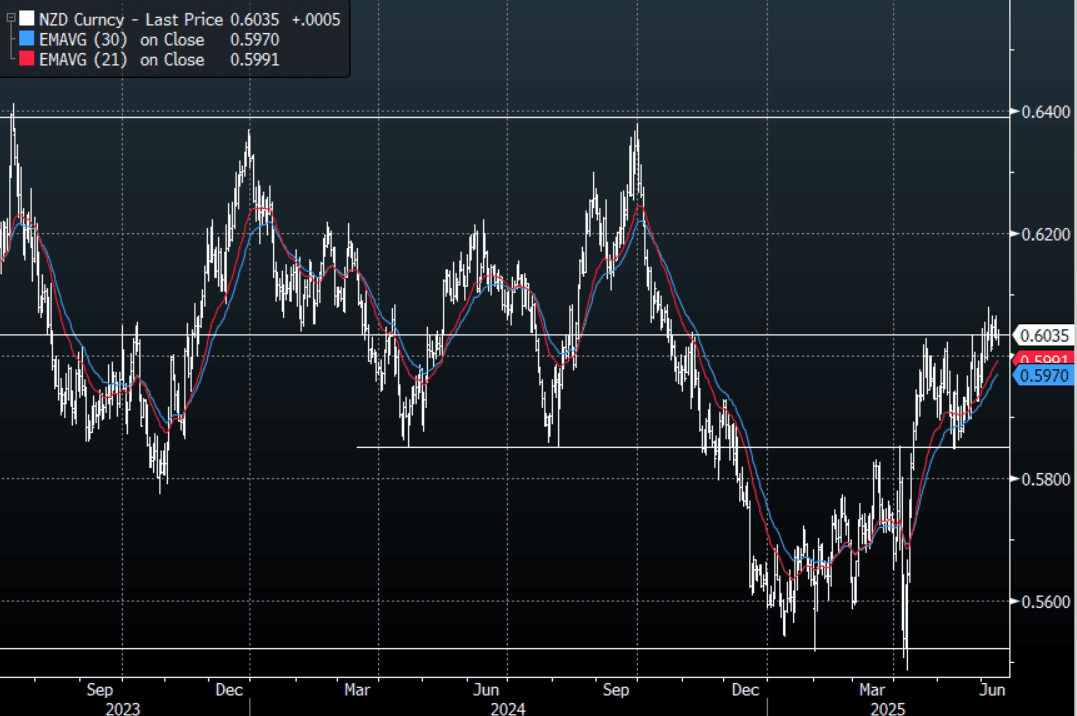

NZD: Asia Wrap - NZD/USD Holds Above 0.6000, Underperforms In The Crosses

The NZD/USD had a range of 0.6016 - 0.6040 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has bounced off support back towards the 0.6000 area as the USD remains under big pressure. The NZD/USD is struggling for direction as risk is turning lower at the same time, the crosses look a better place to express the NZD underperformance.

- Soft Q2 Retail Card Transactions. NZ card transactions remained soft in May with retail sales falling 0.2% m/m to be up 0.2% y/y after -0.6% y/y helped by positive base effects. While the total rose 0.3% m/m, it had declined the previous four months, and is now up 0.2% y/y. The 3-month momentum deteriorated for both series. Although the RBNZ doesn’t have a bias with rates in the neutral range, it is monitoring data and events very closely and this release is signalling weak Q2 consumption.

- Westpac Sees Gradual Consumption Recovery Later In 2025. Westpac notes that spending has moved sideways over the last three months but expects it to improve over H2 2025 with mortgages rolling over improving disposable incomes but the recovery in consumption is still likely to be gradual.

- The NZD’s inability to accelerate above 0.6050 has seen the move higher stall in the short term, first support is seen back towards the 0.5950 area. The NZD underperformance is being seen in the crosses.

- While the support around 0.5850 holds there should be buyers around on dips. A clear break above 0.6050/0.6100 is needed to provide the spark for the next leg higher.

AUD/NZD range for the session has been 1.0769 - 1.0794, currently trading 1.0770. A top looks in place now just above 1.0900, the cross topped out on Monday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBA Dated OIS Dec Meeting Pricing 35bps Firmer Than Pre-CPI Level

RBA-dated OIS pricing is 2–11bps firmer today, led by the late 2025 to early 2026 contracts. Pricing for individual meetings is now 4–35bps higher than levels observed prior to the release of Q1 CPI data on April 30.

- Q1 headline and underlying inflation printed 0.1pp higher than expected but the trimmed mean at 2.9% y/y was below the top of the RBA’s 2-3% target band for the first time since Q4 2021.

- A 25bp rate cut in May is currently given a 96% probability, with a cumulative 82bps (117bps before the CPI data) of easing priced by year-end (based on an effective cash rate of 4.09%).

Figure 1: RBA-Dated OIS – Post-CPI Vs. Pre-CPI

Source: MNI - Market News / Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Outperform Thanks To China

The S&P is down 0.39% this morning in the Asian session. Some intra-day retracement is to be expected but the broader risk-on move might still have a couple of days to play out as the price action shows the market was not expecting such a positive outcome so quickly. The Westpac May consumer sentiment report for Australia rose 2.2%m/m to put the index back at 92.10. We remain sub recent highs, with 95.9 recorded back in March of this year. The NAB Australian business survey saw conditions ease to +2 from a revised +3 reach in March. On the confidence front, the reading edged up to -1 from -3 prior. These headline measures aren't suggesting a sharp turnaround in domestic economic growth momentum in the near term. The USD/CNY fix was set at 7.1991. Today's fixing is sub the 7.2000 level for the first time since Apr 7. It comes despite the stronger USD index levels overnight, although some offset was from lower USD/CNY levels.

- AUD/USD - Asian range 0.6361 - 0.6393, the AUD is currently dealing around 0.6400. AUD has outperformed this morning benefitting from its close trading relationship with China. Good demand was seen again back towards the 0.6350 support area. A break below 0.6300 needed to reverse direction.

- AUD/JPY - Asian range 94.07 - 94.64, price goes into London trading around 94.60. While the support around 92.00 holds, price is likely to continue testing the Weekly resistance seen towards 96.00 where sellers should remerge.

- NZDUSD - Asian range 0.5847 - 0.5877, going into London trading around 0.5980. The NZD has found demand this morning after dipping overnight. Price is approaching the bigger support back towards 0.5800, this needs to hold for those who believe the USD is set to move lower.

AUD/NZD - Asian range 1.0869 - 1.0888, the Asian session is currently trading 1.0880. The Cross has not backed off once since making a low of 1.0654 on the 23 April, it is now challenging the pivot around 1.0900 a sustained break above would turn the focus higher.

Fig 1 : NZD/USD Spot Daily Chart

- Source: MNI - Market News/Bloomberg

US TSYS: Asia Wrap - Yields Drift Lower

TYM5 has traded slightly higher within a range of 110-02 to 110-08 during the Asia-Pacific session. It last changed hands at 110-07, up 0-02 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.983%, down 0.03 from its close.

- The US 10-year yield has drifted lower, dealing around 4.45%, down 0.02 from its close.

- “ The House tax committee released key details of the multi-trillion dollar tax-cut bill President Trump is seeking to enact as his signature legislative achievement this year.”(BBG) This would add to the easing if passed and provide another tailwind for risk.

- The 10-year Yield range seems to be 4.10% - 4.5%, price has bounced nicely off the 4.25/30 support, price is now testing the upper bound of the range around 4.45/50%. A sustained break above this level would see another round of selling targeting the 4.75% area.

- MNI US CPI Preview - The broad assumption is that April is too early to have seen the impact from sharp increases in tariffs in April, with summer months more likely as inventories are reduced after significant front-running.

- However, Monday’s significant cooling in US-China tensions - with US tariffs on China temporarily being cut from 145% to 30% and China tariffs on US from 125% to 10% for a 90-day period - will see this report viewed in a different light again.

- That said, while April’s data could be glossed over as unrepresentative of ongoing inflation dynamics, the risks to an outsized market reaction tilt to the hawkish side (albeit with Monday’s further hawkish readjustment likely limiting the magnitude). Weaker-than-expected data could be shrugged off as the calm before the storm. Stronger April inflation pressures could be a signal that firms are already raising prices.

- Data/Events : US CPI Tomorrow