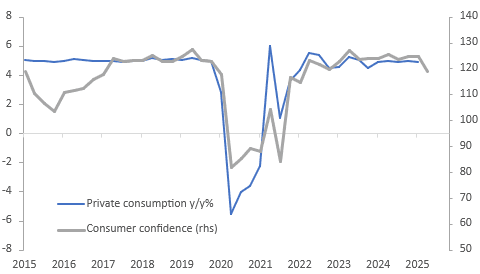

INDONESIA: Weak Q2 Sentiment Suggests Slowdown In Consumption

Consumer confidence fell sharply in May to its lowest since September 2022, Bank Indonesia’s tightening cycle had begun the month before. Despite a 25bp rate cut in May, sentiment fell to 117.5 from 121.7 with the weakness broad-based across current conditions and expectations. Subdued disposable income growth and cost-of-living pressures have weighed on sentiment which is signalling a slowdown in Q2 spending. The next BI decision is June 16 and it’s likely to be on hold.

Indonesia consumption

Source: MNI - Market News/LSEG

- Confidence fell 3.5% m/m in May with expectations also down 0.6% m/m likely impacted by current heightened global uncertainty related to US tariffs. The assessment of economic conditions was down 6.7% m/m, suggesting a difficult current environment which is likely due to both domestic and global developments.

- On the one hand, the S&P Global manufacturing PMI has printed below the breakeven 50-mark for two consecutive months, auto sales fell in three out of four months in 2025 and Q1 GDP showed a slowing in growth which is expected to continue.

- On the other hand, the PMI showed optimism around the outlook with a pickup in hiring, April tourist arrivals rose strongly with the annual rate at 14%, retail sales are recovering rising 5.5% y/y in March and export growth is holding up at about 7.5% y/y 3-mth average supported by solid growth to China. Import growth has risen over 2025 suggesting solid domestic demand.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Yields Drift Lower

TYM5 has traded slightly higher within a range of 110-02 to 110-08 during the Asia-Pacific session. It last changed hands at 110-07, up 0-02 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.983%, down 0.03 from its close.

- The US 10-year yield has drifted lower, dealing around 4.45%, down 0.02 from its close.

- “ The House tax committee released key details of the multi-trillion dollar tax-cut bill President Trump is seeking to enact as his signature legislative achievement this year.”(BBG) This would add to the easing if passed and provide another tailwind for risk.

- The 10-year Yield range seems to be 4.10% - 4.5%, price has bounced nicely off the 4.25/30 support, price is now testing the upper bound of the range around 4.45/50%. A sustained break above this level would see another round of selling targeting the 4.75% area.

- MNI US CPI Preview - The broad assumption is that April is too early to have seen the impact from sharp increases in tariffs in April, with summer months more likely as inventories are reduced after significant front-running.

- However, Monday’s significant cooling in US-China tensions - with US tariffs on China temporarily being cut from 145% to 30% and China tariffs on US from 125% to 10% for a 90-day period - will see this report viewed in a different light again.

- That said, while April’s data could be glossed over as unrepresentative of ongoing inflation dynamics, the risks to an outsized market reaction tilt to the hawkish side (albeit with Monday’s further hawkish readjustment likely limiting the magnitude). Weaker-than-expected data could be shrugged off as the calm before the storm. Stronger April inflation pressures could be a signal that firms are already raising prices.

- Data/Events : US CPI Tomorrow

CHINA: Bond Futures Remain Stable

- China bonds have been very stable over the last two weeks as the PBOC keeps a tight reign on liquidity with limited injections via the OMO.

- The 10YR bond future down -0.02 at 108.66 and is at the mid-point between the 20-day EMA of 108.81 and the 50-day EMA of 108.59.

- The 2YR bond future is up +0.03 at 102.35, yet remains below all major moving averages. The nearest is the 20-day EMA at 102.38

CGB's are stronger today with the 10YR at 1.66% (-1.5bp lower today).

JGBS AUCTION: 30Y Supply Shows Solid Demand Metrics

The 30-year JGB auction delivered solid results, suggesting stronger investor demand. The low price cleared at 91.10, aligning with dealer expectations per a Bloomberg survey. Moreover, the cover ratio rose to 3.0739x from 2.9582x, and the auction tail narrowed significantly to 0.30 from 0.75 (the longest since 2023), both indicating a marked improvement in bidding strength.

- This follows a weaker 10-year auction earlier this month, which showed subdued demand metrics.

- As highlighted in our preview, today's issuance arrived with an outright yield approximately 50–55 basis points higher than last month’s, just below the cycle high of 3.0%.

- The auction also took place against a backdrop of deteriorating sentiment toward longer-dated global bonds, driven by upbeat trade news, resilient U.S. economic data, and delayed expectations for Fed rate cuts.

- Given this uncertain environment, today’s strong result may be viewed as a reassuring sign of demand recovery, particularly following recent auction softness.

- The 30-year JGB is slightly richer than pre-auction levels in early afternoon trading.