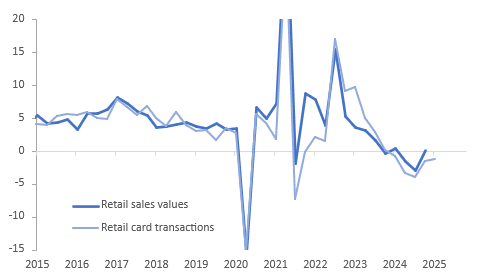

NEW ZEALAND: Soft Q2 Retail Card Transactions

NZ card transactions remained soft in May with retail sales falling 0.2% m/m to be up 0.2% y/y after -0.6% y/y helped by positive base effects. While the total rose 0.3% m/m, it had declined the previous four months, and is now up 0.2% y/y. 3-month momentum deteriorated for both series. Although the RBNZ doesn’t have a bias with rates in the neutral range, it is monitoring data and events very closely and this release is signalling weak Q2 consumption.

- Q2 average retail transactions are down 0.5% q/q to be up 0.2% y/y, strongest since Q4 2023, after -0.2% q/q & -1.2% y/y in Q1. Annual growth over April/May is suggesting the gradual recovery continued but remains soft. Nominal retail sales rose 1.5% q/q and 1.3% y/y in Q1.

- The weakness was impacted by lower fuel prices as the data is nominal. Fuel sales fell 2.4% m/m. There was a large rise in motor vehicle sales +2.6% m/m. Core retail transactions fell 0.2% m/m in May.

- Non-retail rose 1.5% m/m (including medical, travel and post), while services were down 0.2% m/m.

NZ retail sales y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Sharply Weaker Overnight On US-CH Tariff Pause

In post-Tokyo trade, JGB futures closed sharply weaker, -75 compared to settlement levels, after a heavy session for US tsys.

- US tsys gapped lower in early London trade and stocks surged to the pre-Liberation Day levels (April 2) after the US and China agreed to pause their retaliatory reciprocal tariffs for 90 days.

- After a collective sigh of relief, US tsys traded sideways, near session lows for much of the session. Today’s focus is on April US CPI figures at 0830ET.

- According to MNI technicals team, JGB 10-year futures are holding the bulk of the recent strong bullish reversal from early April, rejecting any test of fresh cycle lows for the M5 contract. This defies the bearish momentum studies drawn on the longer-term chart, clearing moving-average resistance to print 142.40 at the new upper level. To the downside, sights are on 136.57, a Fibonacci projection. 144.48 is the medium-term target on any recovery.

- “Japan life insurers could temporarily slow net selling of foreign assets following the US-China 90-day tariff truce, as it could provide greater visibility on their expectations for Japan's long-term bond yields.” (per BBG)

- Today, the local calendar will see BoJ Summary of Opinions (April MPM) and Money Stock data alongside 30-year supply.

BONDS: NZGBS: Cheaper With US Tsys After 90d US-CH Tariff Pause

In local morning trade, NZGB yields are 7-8bps higher, after US tsys finished sharply cheaper. US tsys gapped lower in early London trade, and stocks surged to the pre-Liberation Day levels (April 2), after the US and China agreed to pause their retaliatory reciprocal tariffs for 90 days.

- After a collective sigh of relief, US tsys traded sideways, near session lows for much of the session.

- The increase in risk appetite and the less dovish Fed outlook saw the 2-year bond cheapen 12bps to 4.01%, with the 10-year yield rising 9bps to 4.48%.

- Projected US rate cut pricing retreated from prior levels (*) as follows: Jun'25 at -2.0bp (-2.8bp), Jul'25 at -10.8bp vs. (-13.1bp), Sep'25 -27.0bp (-29.3bp), Oct'25 -40.3bp (-42.6bp).

- Today’s focus is on April US CPI figures at 0830ET.

- Swap rates are 10-12bps higher, with the 2s10s curve unchanged.

- RBNZ dated OIS pricing is little changed across meetings. 25bps of easing is priced for May, with a cumulative 69bps by November 2025.

- Today, the local calendar will be empty ahead of Card Spending and Net Migration data tomorrow.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond.

MNI: UK BRC APR BY VALUE SHOP SALES LFL +6.8% YY, TOTAL +7% YY

- MNI: UK BRC APR BY VALUE SHOP SALES LFL +6.8% YY, TOTAL +7% YY