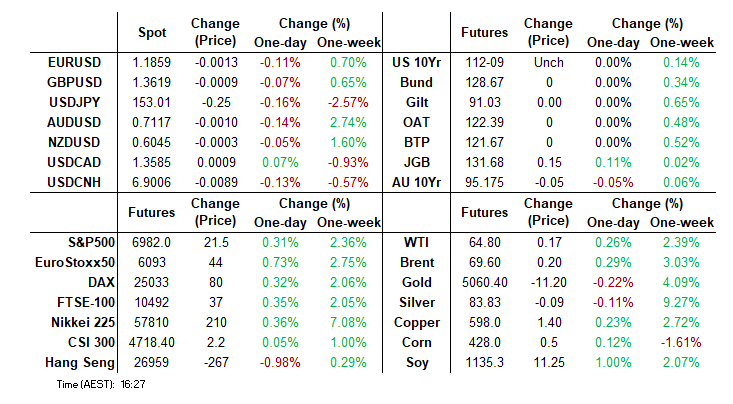

MNI EUROPEAN MARKETS ANALYSIS: USD Dips Before Recovering

EXECUTIVE SUMMARY

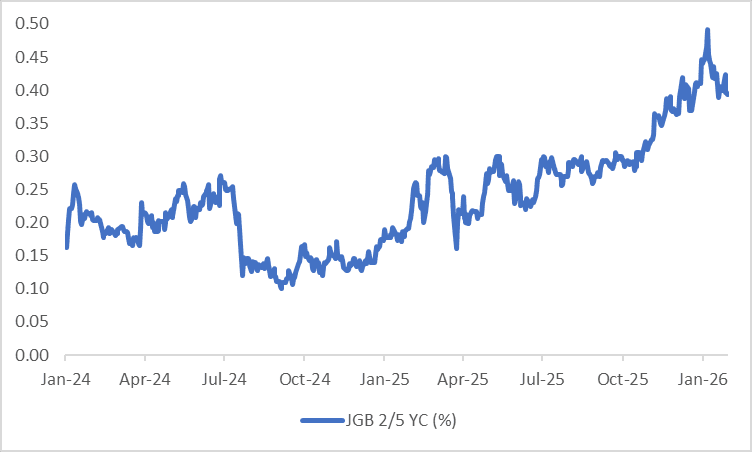

- After reaching a record steepness in mid-January, the 2/40 yield curve is now testing the lower bound of the well-defined range.

- Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said.

- The USD has drifted lower for most of our session as the market tries to interpret its inability to react to the better Payrolls data, although losses have been pared as we approach the London cross over. USD/CNH has tested under 6.9000, while USD/JPY got to 152.27, before rebounding.

- Looking ahead, we have UK GDP, while in the US we have initial jobless claims, before the focus turns to Friday’s release of US CPI.

MARKETS

US TSYS: Yields Range Bound, US CPI Friday Next Focus

A quiet day post NPF with US futures barely moving and yields range bound. TYH6 has traded in a 112-07 to 112-11 range today, but remains unchanged at 112-09.

Cash was marginally better in the front end with yields modest lower, though volumes were extremely light.

- The 2-yr is down -0.6bps to 3.508%

- The 5-Yr is down -0.5bps to 3.739%

- The 10-Yr is down -0.2bps to 4.172%

- The 30-Yr is up +0.3bps to 4.811%

There is more jobs data out tonight with Initial Jobless Claims (est. 223k, prior 231k), continuing claims (est. 1850k, est 1844k prior) and existing home sales. Friday's CPI will be the next major release for bond markets with January CPI forecast to moderate to 2.5% from 2.7% in December. Yields are highly reactive to data at present given very little priced in in terms of rate moves and a miss either way could see decent swings in yields.

The auction schedule tonight sees US$95bn 8-week, US$105bn 4-week and US$25bn 30-Yr.

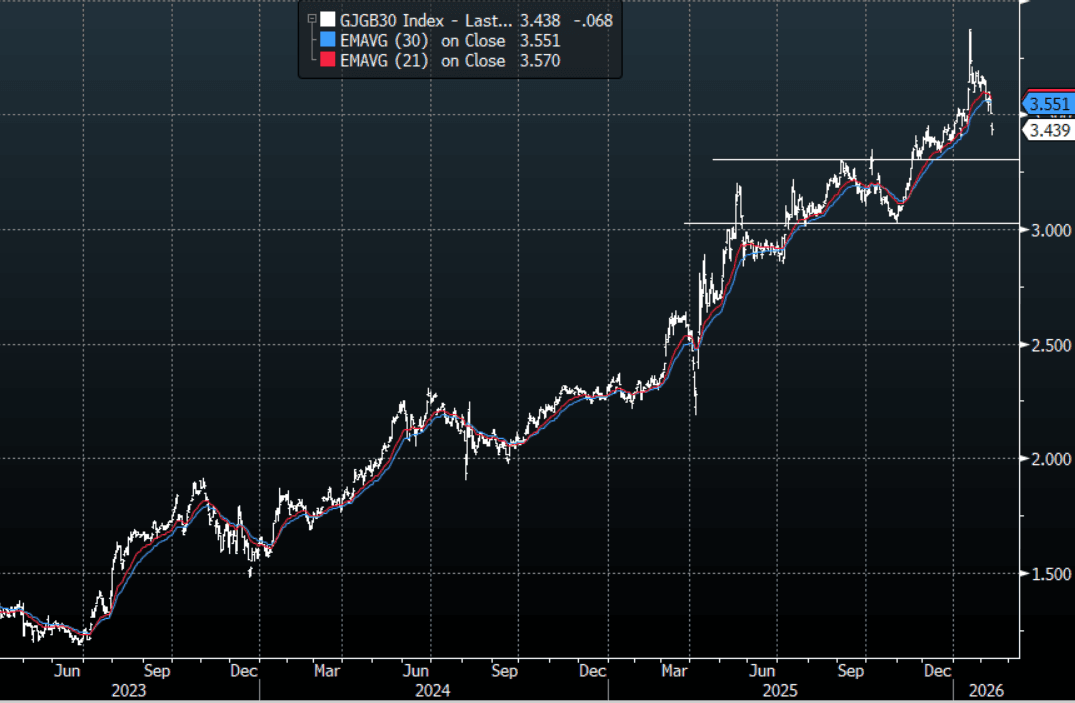

JGBS: Yield Curve Breaking Flatter As Fiscal Concerns Fade

JGB futures are stronger, +20 compared to settlement levels, but at session lows.

- The Japan Jan PPI was in line with market forecasts.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's post-payrolls sell-off.

- Cash JGBs have bull-flattened, with yields 1-9bps lower across benchmarks.

- After reaching a record steepness in mid-January, the 2/40 yield curve is now testing the lower bound of the well-defined range that has contained price action since mid-year.

- Since late last year, steepening has been most pronounced in the 2/5 segment, leaving the 5-year sector relatively unattractive on the curve. Into the recent election, expectations of fiscal expansion under a Takaichi administration implied heavier debt supply, reinforcing pressure on intermediates.

- In recent days, however, those fiscal concerns appear to have moderated following Prime Minister Sanae Takaichi's historic election victory.

- Notably, while the 2/5 segment has flattened, it is the 5/40 curve which has broken through the bottom of the range it has traded in since June last year.

- Swap rates are flat to 5bps lower, with a flatter curve.

- Tomorrow, the local calendar will see Weekly International Investment Flow data alongside an Auction for Enhanced-Liquidity 5-15.5 YR and BOJ Board Member Tamura Speech in Kanagawa.

Source: Bloomberg Finance LP

JGBS: Yield Curve Under Flattening Pressure

After reaching a record steepness in mid-January, the 2/40 yield curve is now testing the lower bound of the well-defined range that has contained price action since mid-year.

- Since late last year, steepening has been most pronounced in the 2/5 segment, leaving the 5-year sector relatively unattractive on the curve. Into the recent election, expectations of fiscal expansion under a Takaichi administration implied heavier debt supply, reinforcing pressure on intermediates.

- In recent days, however, those fiscal concerns appear to have moderated following Prime Minister Sanae Takaichi’s historic election victory.

- Notably, while the 2/5 segment has flattened, it is the 5/40 curve which has broken through the bottom of the range it has traded in since June last year.

- This likely reflects two dynamics. First, renewed yen weakness could bring forward expectations of additional BOJ rate hikes, placing upward pressure on 5-year yields relative to the long end. Second, the 5-year sector has emerged — and is likely to remain — a preferred short among more tactical accounts. In particular, positioning in 5s30s flatteners appears to have scope to extend as the BOJ edges closer to another tightening step.

Bloomberg Finance LP

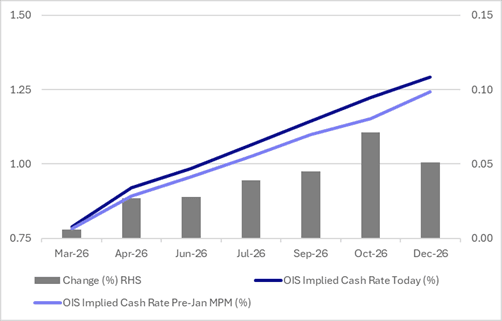

STIR: BOJ Dated-OIS Firmer Than Pre-Jan MPM Levels

Currently, BOJ-dated OIS is 1-8bps firmer than pre-January MPM levels.

- Current pricing assigns a 26% (22% pre-BOJ) probability of a 25bp hike in March, rising to 108% (92% pre-BOJ) by June, 200% (170% Pre-BOJ) by October, signalling expectations for two hikes by late 2026.

- This pricing is consistent with a MNI Policy note earlier in the week: Japanese Prime Minister Sanae Takaichi has been taking market concerns over inflation and fiscal sustainability seriously and will not interfere with the Bank of Japan’s gradual policy tightening from the current 0.75%, MNI understands.

- Despite her preference for low interest rates, she is likely to support further BOJ rate hikes not only to fight inflation but also to achieve the 2% target, as households continue to suffer from high living costs.

Figure 1: BoJ-Dated OIS – Today Vs. Pre-Jan MPM

Source: Bloomberg Finance LP / MNI

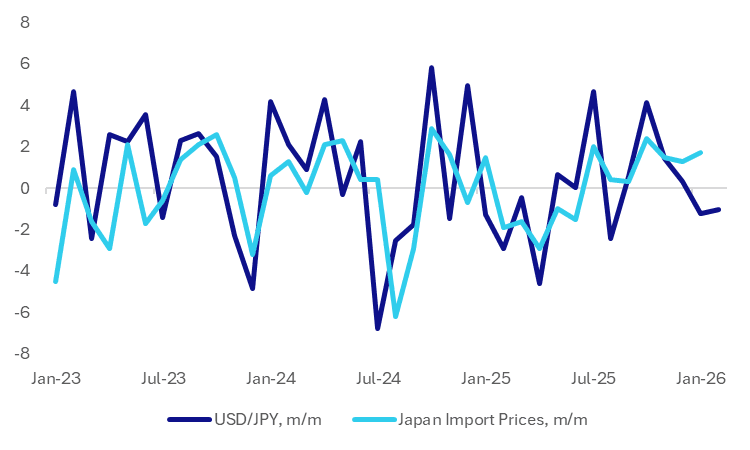

JAPAN DATA: Yen Rise Could Curb Rising Import Prices, But Y/Y May Stay Positive

Japan import prices rose, in m/m terms, for the seventh straight month in Jan. The chart below plots USD/JPY m/m changes against import prices m/m. USD/JPY fell m/m in Jan and if current levels hold to the end of Feb, we will also see a m/m decline for this month. This may help curb upside momentum in monthly import price rises, or at least bring us back closer to flat. Such trends are likely to remain a key BoJ focus point through 2026, as it decides around the timing of its next hike.

- In y/y terms import prices are +0.5%, well up from the July 2025 low of -10.6%. Given the negative y/y base effects through the first half of 2025 it will likely require sharp m/m falls in coming months to not see y/y import price momentum rise. For a given level of global commodity prices, this is likely to require further strong gains in yen versus the USD.

Fig 1: USD/JPY M/M & Japan Import Prices M/M

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Cheaper, RBA: Ready To Raise Rates Further, Infl Expns Up

ACGBs (YM -4.0 & XM -4.0) are weaker after dealing in relatively narrow ranges in today’s session.

- (Bloomberg) “Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said, stressing that the board remains cautious and is yet to decide whether further tightening is warranted. The Reserve Bank chief told a panel of senators on Thursday at Parliament House in Canberra that inflation running “with a three in front of it” is unacceptable."

- RBA Hunter is due to give a speech at a CEDA event in Perth (15:45 AEST).

- MI’s inflation expectations rose to 5% in February from 4.6% in January.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's post-payrolls sell-off.

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +63bps, just below its recent high.

- The bills strip has bear-steepened, with pricing -1 to -5.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 95% by June and 154% by December 2026.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 2.50% 21 May 2030 bond tomorrow.

Bloomberg Finance LP

RBA - Labour Mkt Expected To Remain Tight - Jan Jobs Data Feb 19

RBA Hunter's speech today focuses on defining full employment. See the full speech at this link. Hunter stated: “ The recent acceleration of demand growth beyond our estimate of trend, at a time when the economy is already showing signs of being capacity constrained, means we expect the labour market will remain tight and inflation will remain above target for some time, as outlined in our recent Statement. Moving forward, we’ll be closely assessing capacity pressures in the economy and conditions in the labour market, and this will help us assess the extent to which the recent rise in inflation is temporary; and, in turn, inform our advice to the Monetary Policy Board about the outlook in inflation.”

- Earlier today, RBA Governor Bullock stated: "Our models' estimate of NAIRU have risen a bit, but we don't take a model approach only, we also use a bit of judgment," she said, noting the most recent set of forecasts showed how the Bank considered full employment." and "...has lifted its NAIRU estimate by around 10 basis points to 4.6%, Governor Michele Bullock told a Senate estimates hearing Thursday.

- The current unemployment rate is 4.1%. The next jobs print is due on Feb 19 (next Thursday).

- The labour market data will be important to gauge capacity constraints, but inflation will be the deciding factor around further RBA tightening. Governor Bullock is not committing to a pre-determined outlook, but given the starting point for headline/trimmed mean inflation, we are likely to need to see meaningful downside surprises to prevent further hikes.

BONDS: Modestly Cheaper Ahead Of Heavy Local Calendar Tomorrow

NZGBs closed showing a modest bear-steepener, with benchmark yields 2-3bps higher.

- NZ-US and NZ-AU 10-year yield differentials closed little changed.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s post-payrolls sell-off. US jobless claims highlight a lighter calendar on Thursday, before the focus turns to Friday’s release of US CPI.

- Nevertheless, today’s weekly supply auction exhibited solid demand characteristics, with cover ratios ranging from 3.77x (May-35) to 4.12x (May-31).

- Swap rates closed 3-4bps higher, with wider implied swap spreads.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 44bps.

- The local calendar has been light this week ahead of tomorrow’s release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

Bloomberg Finance LP

FOREX: USD - Trades Heavy Even After A Strong Payrolls

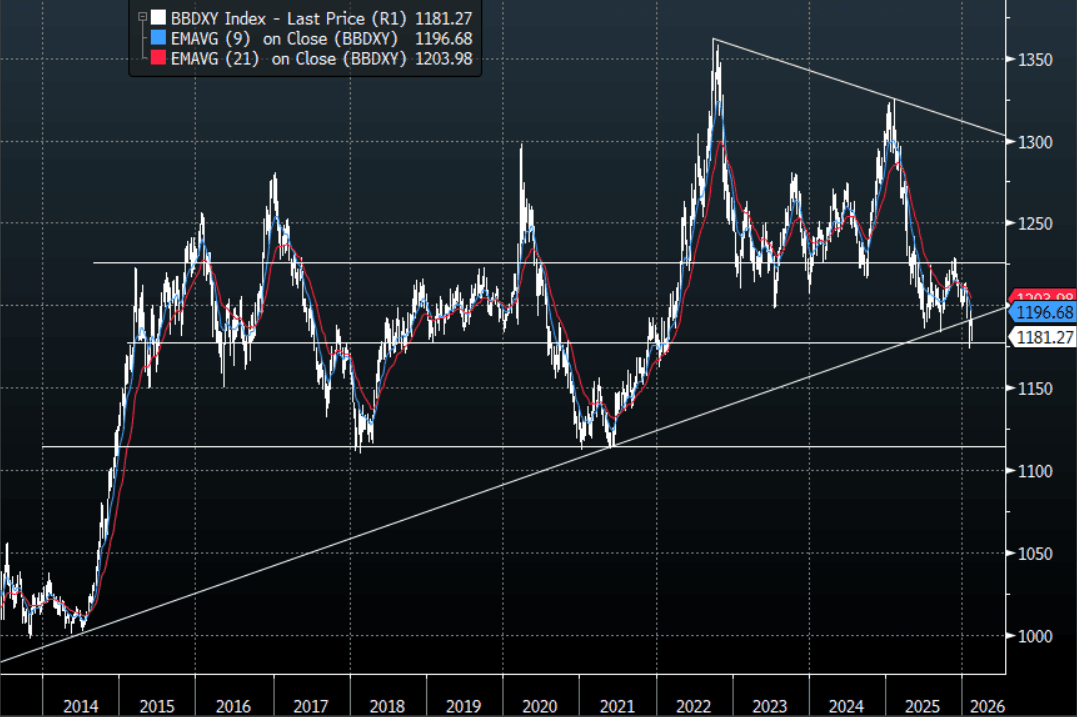

The BBDXY has had a range today of 1180.12 - 1182.72 in the Asia-Pac session; it is currently trading around 1181. The USD has drifted lower for most of our session as the market tries to interpret its inability to react to the better Payrolls data. The market is very bearish the USD and it does not take a lot for the sellers to come back to market as nobody wants to miss out on this trade. Even the significant bounce in US yields as cuts were priced out did little to aid it. On the day, the first resistance is toward the 1185-1187 area and then 1195 where I suspect we could see buyers return. A sustained break below 1175-1180 could potentially signal the start of another leg lower targeting 1150 first and then potentially 1115, see graph below.

- EUR/USD - Asian range 1.1864-1.1885, Asia is currently trading 1.1865. The pair found buyers back toward 1.1800 as the USD initially got bought, but unlike other currencies the EUR has not quite got back to its highs from yesterday. Price action remains constructive, can it now build some momentum from that base to push on? On the day, the first support is back toward 1.1820-1.1850 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 could give it the thrust it needs to have another look toward the 1.2000 area.

- GBP/USD - Asian range 1.3616-1.3642, Asia is currently dealing around 1.3625. The pair is trading pretty poorly considering how weak the USD is. GBP continues to look like 1.3580-1.3730 to me for now as we wait to see if the big USD could potentially break lower, could CPI Friday give it the nudge it needs ?

- Cross asset : SPX +0.30%, Gold $5055, US 10-Year 4.175%, BBDXY 1181, Crude Oil $65.01

- Data/Events : Germany Current Account Balance

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY-Moves Through Overnight Lows As USD Struggles & JGB Yields Sink

The USD/JPY range today has been 152.27-153.45 in the Asia-Pac session, it is currently trading around 152.55, -0.45%. USD/JPY has remained under pressure all through our session as JGB long-end yields came crashing lower, putting in a nice bearish shadow on the daily chart. USD/JPY tried higher overnight as US yields spiked but very quickly reversed and made new lows. Is this just a case of short-term positioning still getting squeezed or does the FX market just not believe the data? Regardless of the reasons, leveraged Yen shorts are being pressured and no doubt are once again being pared back. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.50-154.00 and then 154.80-155.20 area as the market pares back its overextended USD longs and looks for another base to form from which to move higher again.

- "JAPAN TOP CURRENCY DIPLOMAT MIMURA: CLOSELY WATCHING MARKETS WITH A HIGH SENSE OF URGENCY. WON'T COMMENT ON FOREX LEVELS. WILL KEEP COMMUNICATING WITH US AUTHORITIES, WE'RE NOT LOWERING OUR GUARD AT ALL" - RTRS

- Bloomberg - “JGB Yields Falling More About BOJ Hike Bets Than Fiscal Stance. Long-end JGB yields are extending their decline, with the move looking far more about Bank of Japan’s policy expectations than the government’s fiscal restraint.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($735m), 154.00($2.4b). Upcoming Close Strikes : 156.00($1.87b Feb 17), 159.00($1.91b Feb 13),160.00($3.06b Feb 13) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 164 Points

Fig 1 : JGB 30-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

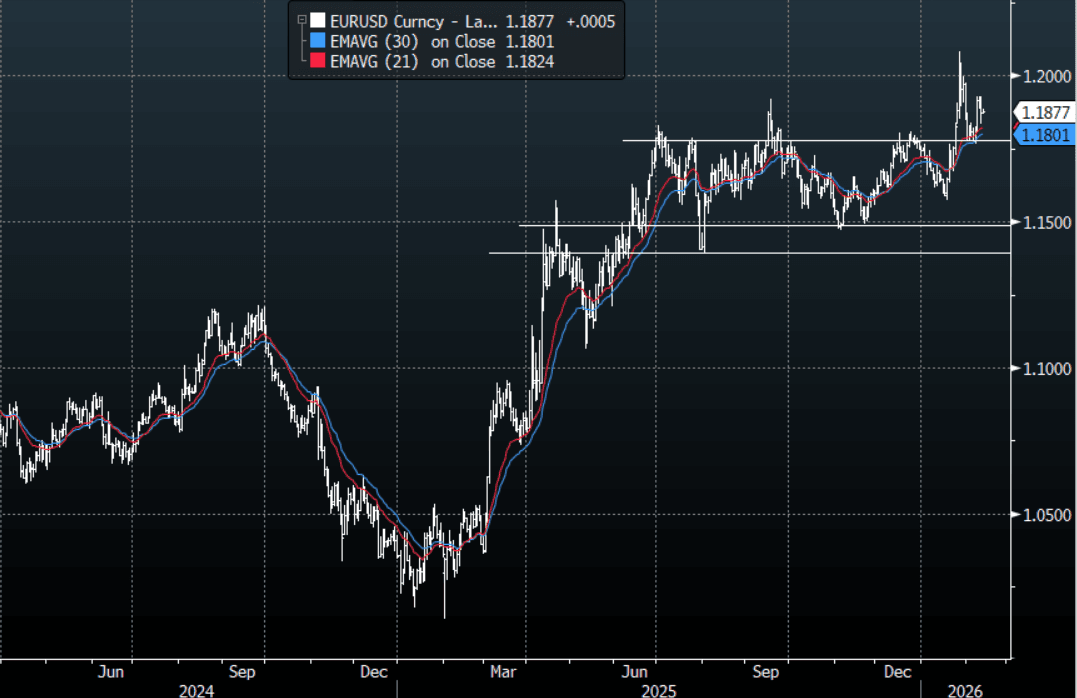

EURUSD: EUR/USD-Bounces Off 1.1830, But The Move Lags Other Currencies For Now

The EUR/USD range overnight was 1.1833 - 1.1927, Asia is currently trading around 1.1880. The pair found buyers back toward 1.1800 as the USD initially got bought, but unlike other currencies the EUR has not quite got back to its highs from yesterday. Price action remains constructive, can it now build some momentum from that base to push on? On the day, the first support is back toward 1.1820-1.1850 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 could give it the thrust it needs to have another look toward the 1.2000 area.

- MNI: Draghi's 'Pragmatic Federalism' Gains Support- Official. Mario Draghi's call for "pragmatic federalism" among varying subsets of European Union states in order to accelerate the completion of the Single Market is finding support among some EU leaders ahead of Thursday's "brainstorming" session in Belgium.

- “Bundesbank President Joachim Nagel told Politico that he supports more joint EU debt to increase the region’s appeal to investors.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.1750(EU1.51b), 1.1760(EU777m), 1.1880(EU461m). Upcoming Close Strikes : 1.1800(EU3.18b Feb 13), 1.1850(EU4.39b Feb 13), 1.1950(EU2.76b Feb 13) - BBG

- The EUR/USD Average True Range for the last 10 Trading days: 67 Points

Fig 1 : EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

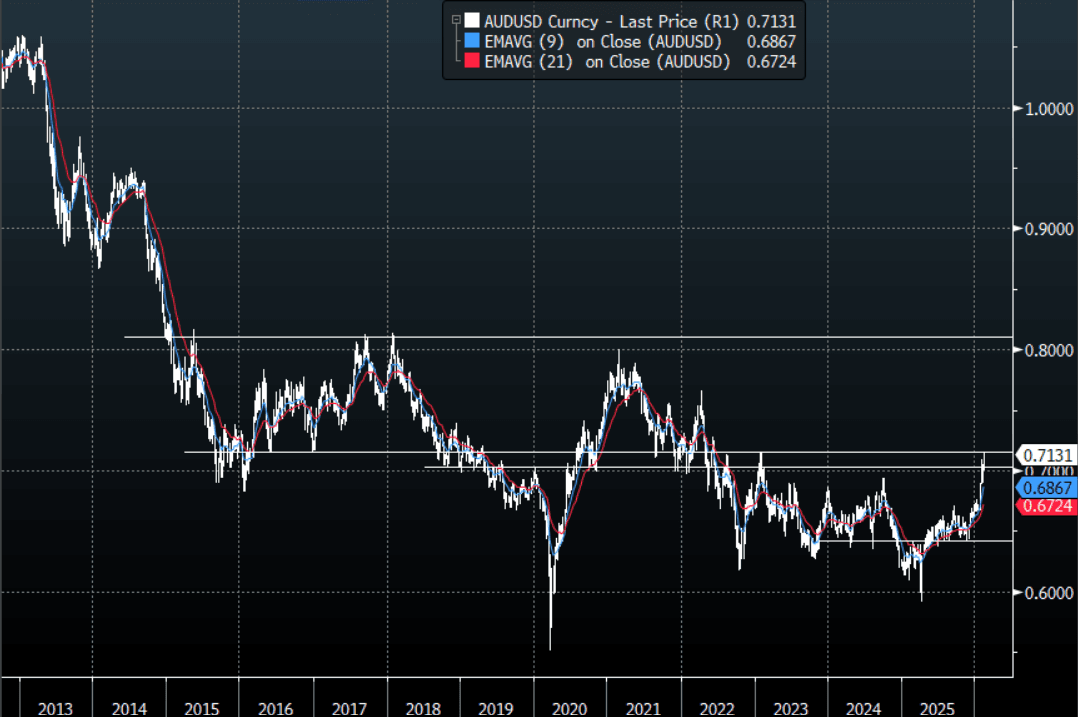

AUD/USD - Drifts Higher As The USD Continues To Struggle

The AUD/USD has had a range today of 0.7119 - 0.7147 in the Asia- Pac session, it is currently trading around 0.7130. The AUD has remained well supported in our session as the USD continues to struggle. The AUD after a brief drop overnight is back above its recent highs, the AUD remains a favourite vehicle to express a long at the moment. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7060–0.7090 area, and then the 0.7000 area. The bulls will be looking for dips to remain supported in order to regain the momentum to challenge the pivotal 0.7100-0.7200 area. A sustained break above here targets 0.7600-0.7800 first and then 0.8000-0.8200.

- MNI BRIEF: RBA's Bullock Sees NAIRU At 4.6%. Bullock said returning inflation to the 2.5% midpoint target may or may not require further hikes, adding that a stronger Australian dollar and higher interest rates will help dampen demand. Australia's unemployment rate tightened to 4.1% in December.

- Bloomberg - “Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said, stressing that the board remains cautious and is yet to decide whether further tightening is warranted.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7080(AUD342m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6825(AUD791m Feb 13) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 79 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

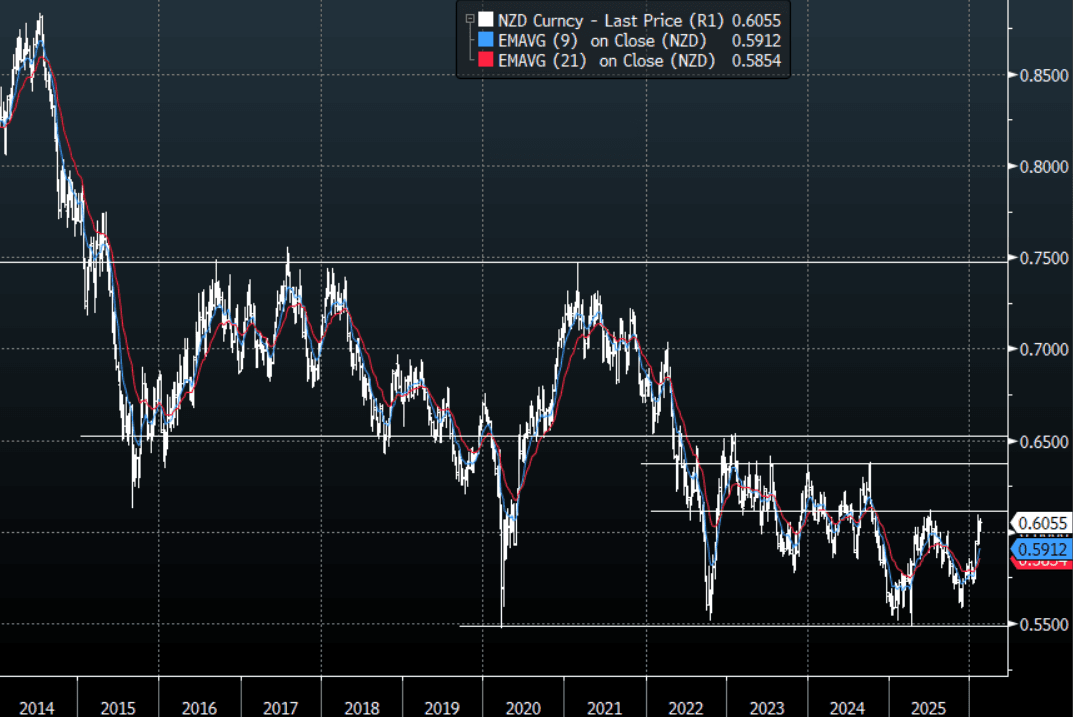

NZD/USD - Consolidating Around 0.6050, Eyes 0.6100 As USD Trades Heavy

The NZD/USD had a range today of 0.6044-0.6062 in the Asia-Pac session, it is currently trading around 0.6055, +0.12%. The NZD is consolidating its recent gains around the 0.6050 area. The NZD is back around where it started the day yesterday. I am a little surprised by the lack of reaction to the strong payrolls, but the bulls will be very happy with the constructive price action. On the day, the NZD bulls will be hoping the pair can regain its upward momentum to test the pivotal 0.6100 area. The first support is back toward 0.5990-0.6020 and then the 0.5900-0.5950 area. A sustained break back above 0.6100 could potentially open up a move back toward the 0.6400-0.6600 area and then beyond.

- MNI AU - USD/CNH Breaks Under 6.9000, Fresh Lows Since 2023, Onshore CNY Gains Aid Move.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5900(NZD301m Feb16), 0.6000(NZD308m Feb 16), 0.6200(NZD430m Feb 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 59 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Taiwan Inflows Surge Pre LNY Break, Mostly Positive Trends Elsewhere

Taiwan remains a standout from an inflow standpoint, with a further +$1.8bn in net inflows yesterday. This has seen the 5-day sum and 2026 to date net inflows improve further. Still if we go back to the end of Jan, net inflows since then are close to flat, hence there is still scope for further upside momentum in flows. This will have to wait though with local equities now shut for the lunar new year break. They re-open on Feb 23rd. Familiar drivers remain in play for Taiwan stocks amid tech/AI, domestic growth, optimism.

- South Korean inflows continue to recover from recent outflow pressures. The Kospi has surged towards 5500, up 2.65%, to fresh record highs today. Per the NBUY function on BBG, we have seen nearly $1bn in more additional inflows today.

- In Indian, position inflow momentum persists, but the large chunky inflows seen post US-India trade headlines recently slowed somewhat. Indeed recent US statements which appear to change the fact sheet around the trade deal has created fresh uncertainty.

- In South East Asia, Indonesia remains the main negative, generally positive flow outcomes are evident elsewhere, consistent with positive local equity market trends.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2026 To Date | |

| South Korea (USDmn) | 599 | -4813 | -6040 |

| Taiwan (USDmn) | 1835 | 1930 | 3139 |

| India (USDmn)* | 35 | 808 | -1738 |

| Indonesia (USDmn)* | -42 | -142 | -742 |

| Thailand (USDmn) | 35 | 944 | 1192 |

| Malaysia (USDmn) | 72 | 133 | 379 |

| Philippines (USDmn) | 14 | 41 | 280 |

| Total (USDmn) | 2549 | -1099 | -3530 |

| * Data Up To Feb 10 |

Source: Bloomberg Finance L.P./MNI

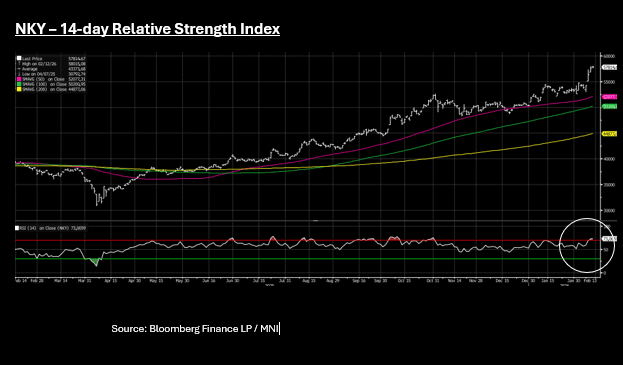

ASIA STOCKS: KOSPI & NKY Hit New Highs; NKY Reaches Overbought on 14RSI

The Nikkei returned from holiday today but couldn't replicate the gains from earlier in the week. Up just +0.25% today it takes the index to over 6% higher for the week on a day when the long end of the JGB curve rallied strongly, retracing losses from January February. Currently at 57,800 the NKY has reached yet another new high, having delivered year to date gains over 10%. The gains have seen the NKY reach Overbought on the 14RSI - which could dampen near term further gains.

News that a potential rescue package could be announced by the Shenzhen government to the tune of CNY80bn did little to impact China's major equity markets Thursday with the HSI down -0.85 and onshore bourses posting only modest gains. Other key real estate names in HK did however receive a boost with Sun Hung Kai Properties one of the main gainers for the index.

Ongoing strength of inflows is a fundamental support for the TAIEX in Taiwan with gains of +1.6% today ahead of LNY, as TSMC rose over 2% to a new record of TWD1,915. The KOSPI had a strong day also with key AI names SK Hynix up +2.5% and Samsung up +6.00% contributing to the KOSPI's gain of +2.6%. Earlier the KOSPI hit a new high of 5,515 only to moderate back to 5,498

The JCI sits on gains of over 4% for the week despite modest falls Thursday, as President Prabowo's heads to the US where it is intended he signs the US trade deal.

Oil Tight Ranges in Near Term, Pending Further News from US Iran Talks

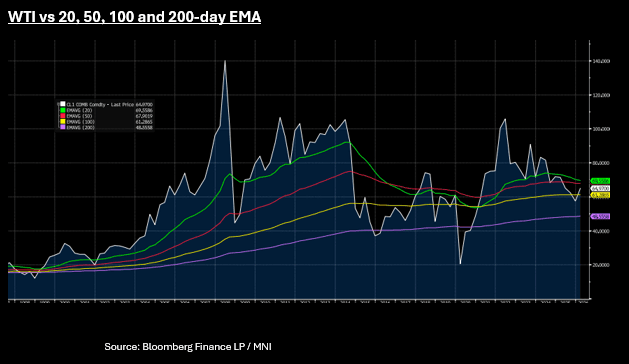

- Oil's steady ascent continued in Asia today with WTI up +0.5%, nearing $65. WTI has traded in a $64.78 - $65.10 range, currently at US$64.97bbl. WTI is at the mid point of its upper resistance via the 50-day EMA of $67.90 and downside via the 100-day EMA at 61.28. Momentum indicators are weak, leaving oil susceptible to US Iran headlines. This suggests prices are likely to stay rangebound in the near term as political progress remains slow.

- Brent is up +0.4% at US$69.70bbl - having traded in a very tight range of $69.54 - 69.85.

- Oil markets continue to wait for further new on the next US Iran meeting whilst digesting the myriad of news out on stockpiles and potential new oil sources.

- Chevron, Eni , QatarEnergy, Repsol won rights to explore for oil in Libya, the latest sign that the nation that holds Africa's largest crude reserves is opening up for investments following years of civil war. (per BBG)

The well known longer term oversupply issue is not a key driver in the short term as uncertainty remains as to any outcome of US Iran talks. The bar is high for a clear outcome with both sides stoic in their views as to their preferred outcome.

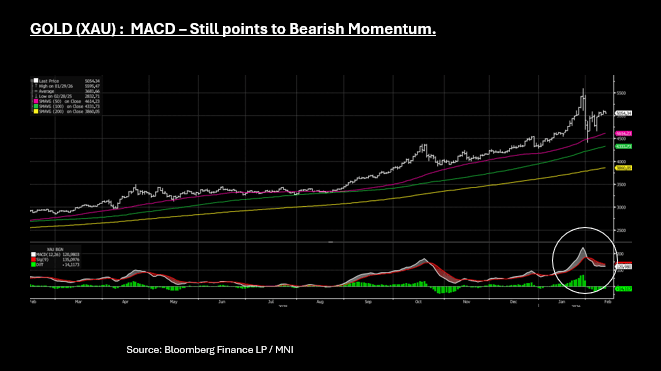

GOLD: Bearish Momentum Remains in Prices, $5,000 Could be Re-Tested

- Demand for Chinese gold ETFs is expected to continue robust growth in 2026 despite official concern over the exposure of retail investors to volatility and speculation, local analysts told MNI.

https://www.mnimarkets.com/articles/mni-china-gold-demand-robust-despite-volatility-1770859956330 - Geopolitical risk, persistent domestic growth challenges and continued weakness in the property sector are likely to keep Chinese investors drawn to the metal’s safe-haven appeal following a record-breaking 2025, said Ray Jia, Research Head APAC (ex-India) and Deputy Head of Trade Engagement, China, at the World Gold Council.

- This follows news out earlier this week showing that even during the time of volatility for gold, the PBOC still added to its holdings.

- This underpins the narrative that many investors now hold that gold's rise is a function of the long term decline in the US, suggesting it could hit US$6,000 sooner rather than later.

- Gold has traded below the opening price of US$5,095.35 all day, touching lows of $5,045.54 currently, for losses of -0.6%. Today's moves re-affirm the MACD which shows the MACD line (white) below the Signal line (red), which suggests that bearish momentum remains in the price action.

CHINA: 10-Yr CGB Resets Near Term Range to 1.70-1.80%

- CGB bond yields have moved lower Thursday, following another day of sizeable liquidity injections. With injections tipped to be significant this week ahead of the lunar new year holiday, we noted in recent posts that the risks were skewed to the downside for 10-yr bond yields. https://cms.mnimarkets.com/news/edit/story/317098, especially given the CPI miss.

- Week to date the PBOC has injected over CNY1tn of liquidity, utilizing a variety of maturities and with equity markets mixed currently, we anticipated some found find its way into the 10-Yr CGB.

- The 10-Yr is down -1.8bps to 1.781% its lowest since September 2025. Back in September expectations for for GDP growth was 4.5-4.7%, in line with the 2026 forecast of 4.5%.

- As we approach the March NPC meeting, expectations are growing for monetary action with RRR cuts favoured, whilst some suggest a rate cut could be forthcoming.

- Either will provide good support for bonds and could see the 10-Yr range shift down to 1.70-1.80% in the near term.

- Bond futures are only up modestly Thursday with the 10-Yr up +.04 at 108.605 - but taking it to overbought on the RSI. Whilst China bond futures may not react necessarily to tech levels, it is important to note the change in momentum.

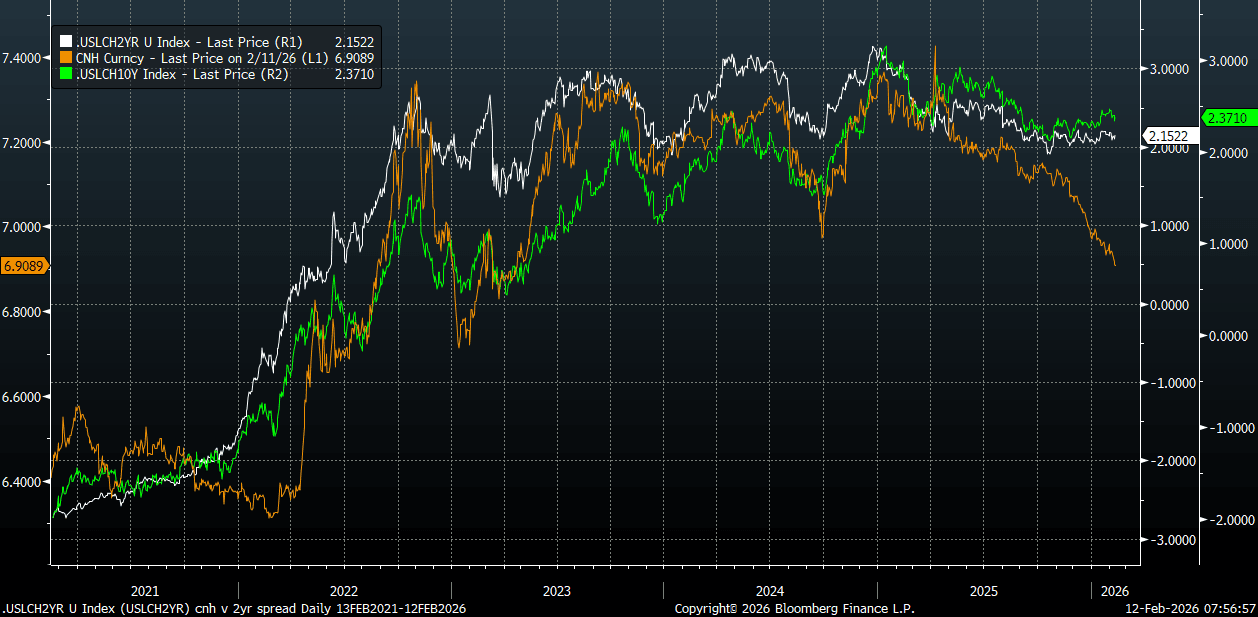

CNH: Wedge With US-CH Yield Differentials Widen, SCMP Says Trade Truce To Extend

Spot USD/CNH sits near 6.9060 in early Thursday dealings, after being little changed in aggregate for Wednesday's session. We saw a spike towards 6.9200 post the better than expected US NFP print, but this was quickly reversed. Recent cycle lows at 6.9049 remain intact, albeit just, while broader technical risks are still skewed lower (the 20-day EMA is around 6.9430 on the upside). Headlines also crossed from SCMP earlier today that: "TRUMP AND XI EXPECTED TO EXTEND TRADE TRUCE AT BEIJING SUMMIT-SCMP - [RTRS], "TRUMP AND XI MAY ROLL BACK TARIFFS FOR UP TO A YEAR- SCMP - [RTRS]". This may be helping CNH sentiment early in Thursday trade.

- Focus is likely to remain on whether we can test 6.9000 ahead of the lunar new year, which kicks off next Monday. Spot USD/CNY ended at 6.9121 on Wednesday, while the CNY CFETS basket tracker was little changed around 97.90.

- The pick up in US Tsy yields post the NFP release helped curb recent downside momentum. US-CH yield differentials have stabilized and drifted a little higher over recent months, the 2yr spread around +215bps. The chart below shows a widening divergence between such spreads and the break lower in USD/CNH.

- We have seen divergences in the past but usually the series realign with each other over the medium term. China yields have drifted lower and likely have limited upside. Still, US Tsy yield shifts are likely to dictate US-CH yields trends over coming months.

- China efforts to globalize CNY use (efforts to step up its reserve status etc), along with a consistent downtrend in the USD/CNY fixing (even during periods of USD strength) have played into USD/CNH downside. So far there hasn't been strong push back from the authorities around yuan gains, although the CNY CFETS basket remains under recent highs.

Fig 1: Spot USD/CNH Versus 2yr and 10yr US-CH Yield Differentials

Source: Bloomberg Finance L.P/MNI

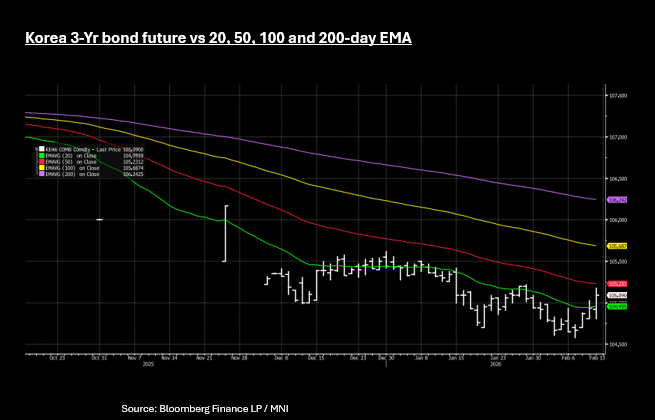

SOUTH KOREA: 3-Yr Rally on JGB Boost as Futures Above Key Tech Level

- The front end in Korea is seeing a strong move lower in yield today, following 3-Yr KTBs / IRS near 1-year highs recently.

- The BOK last cut rates in May 2025 and in January 2026 moved to a neutral bias, (from an easing bias) giving little steer for bond investors in the near term.

- Currently swaps models suggest little to no movement in rates for the first half of 2026, yet 3-Yr yields are almost +100bps higher from the lows of April last year.

- The short end in KTBs has been under pressure with significant amount of issuance in the 1-3Yr maturity bucket for KTBs. Today alone there is a KRW1.2tn 1-Year government bond being issued and impacts the front of the curve.

- Year to date issuance estimates are around 10-12% of total government issuance budgeted for the year is already done by mid February and focused in the 1-3-Yr. This has been the driver for the move higher

- Three year NDIRS are down -5bps in yield today on no news domestically. Correlations with JGBs have been strong post the election result in Japan and short end JGBs are down today - whilst short end USTs are doing very little.

- KTB bond futures didn't react initially to the rally in JGBs but once the orders at open were done, are strong today with the 3-Yr up +.16 to 105.10 and for the first time in February is back above the 20-day EMA of 104.95. Above is the 50-day EMA of 105.23 as topside resistance.

- KTB moves at present are very technically driven, given the limited expectation for interest rates in the near term investors are looking for catalysts elsewhere. Watch closely ongoing JGB moves for guides, with correlations up over +.35 at present .

ASIA FX: CNH Tests Under 6.9000, USD/KRW Following USD/JPY Lower

In North East Asia, the bias has been for softer USD/Asia trends, with USD/CNH breaking sub 6.9000. USD/JPY has continued to fall, getting under Wednesday lows, while broader USD sentiment is mostly weaker. The equity tone is mixed, with Taiwan's stock market already closed for the lunar new year break. The Kospi has rallied strongly, up near 5500, (+2.5%), to fresh record highs.

- The break under 6.9000 for USD/CNH came after the onshore spot open, with USD/CNY tracking lower (although onshore spot hasn't broken under 6.9000 yet). Follow through downside for USD/CNH has been limited, with lows so far of 6.8965 (last near 6.8995). These are levels last seen in 2023, with Apr lows from that year near 6.8300. Next week onshore markets are out for the Lunar New Year break. When we return focus will be on if we see continued conversion of offshore earnings into local FX and whether the authorities push back more on CNY gains (the CNY CFETS basket is still under recent highs though, off by around 1.1%).

- Spot USD/KRW continues to retrace off recent highs, the pair back close to 1441, up a further 0.40% in won terms so far today. We are under the 100-day EMA support point, with a break under 1440 likely to see the 1420 region targeted, which marked late Jan lows. Spill over from yen gains is evident, with recent correlations firm between the two currencies.

- USD/TWD continues to track lower, but TWD is only up a further 0.20% to be just under 31.40. Onshore FX markets trade tomorrow before being out next week for the lunar new year break. Downside focus for USD/TWD will be at 31.27 (late Jan lows). the 100-day EMA rests near 31.21. Inflow momentum from offshore investors surged prior to the LNY break for onshore equities.

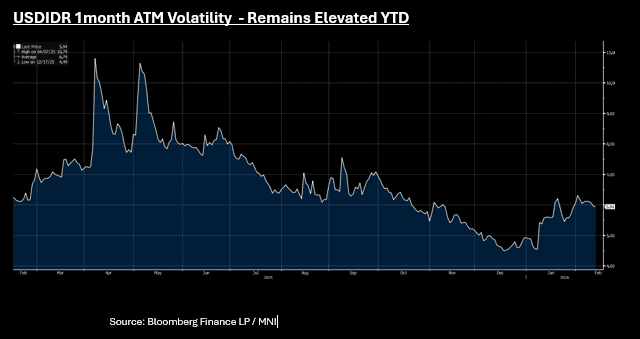

IDR: USDIDR Back Above 16,800 - Could Retest Recent Highs

- Despite strength across the board for regional currency peers, USDIDR skipped the rally and is higher today by +47. Currently near 16,827 / 16,837 USDIDR has climbed back above 16,800 giving back much of yesterday's gains. The rupiah holding onto losses of +0.27% for the day Thursday and back above the 20-day EMA of 16,810, whilst remaining neutral on most momentum indicators. Yesterday we got close to the 50-day EMA but couldn't break lower.

- Following three days of strong gains for the JCI, it is down -0.50% today on profit taking; a possible contributor to the decline in IDR.

- There is little in the calendar for Indo data and with the impending LNY holiday in China slowing everything down, the USDIDR could be vulnerable here and retest February highs of 16,877. IDR is seeing very little positive spill over from broader USD weakness.

- A key metric for the BI is USDIDR Vol which remains elevated relative to January lows, supporting the idea that February highs could be re-visited in a risk off environment. BI is likely to remain on guard against IDR weakness.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/02/2026 | 0700/0700 | *** | UK Monthly GDP | |

| 12/02/2026 | 0700/0700 | ** | Trade Balance | |

| 12/02/2026 | 0700/0700 | ** | Index of Production | |

| 12/02/2026 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/02/2026 | 0700/0700 | ** | Index of Services | |

| 12/02/2026 | 0700/0700 | *** | GDP First Estimate | |

| 12/02/2026 | 0900/1000 | ECB's Cipollone At Commissione Europa Conference | ||

| 12/02/2026 | - | BOE MPG Meeting | ||

| 12/02/2026 | - | *** | New Loans | |

| 12/02/2026 | - | *** | Money Supply | |

| 12/02/2026 | - | *** | Social Financing | |

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers panel talk on productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR existing home sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane At The World Ahead 2026 Gala Dinner | ||

| 12/02/2026 | 0000/1900 | Fed's Lorie Logan, Stephen Miran | ||

| 13/02/2026 | 0700/0800 | * | Wholesale Prices | |

| 13/02/2026 | 0730/0830 | *** | CPI | |

| 13/02/2026 | 0800/0900 | *** | HICP (f) | |

| 13/02/2026 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 13/02/2026 | 1000/1100 | * | Employment | |

| 13/02/2026 | 1000/1100 | * | Trade Balance | |

| 13/02/2026 | 1000/1100 | ECB's de Guindos Lecture At Academia Europea Leadership | ||

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event |