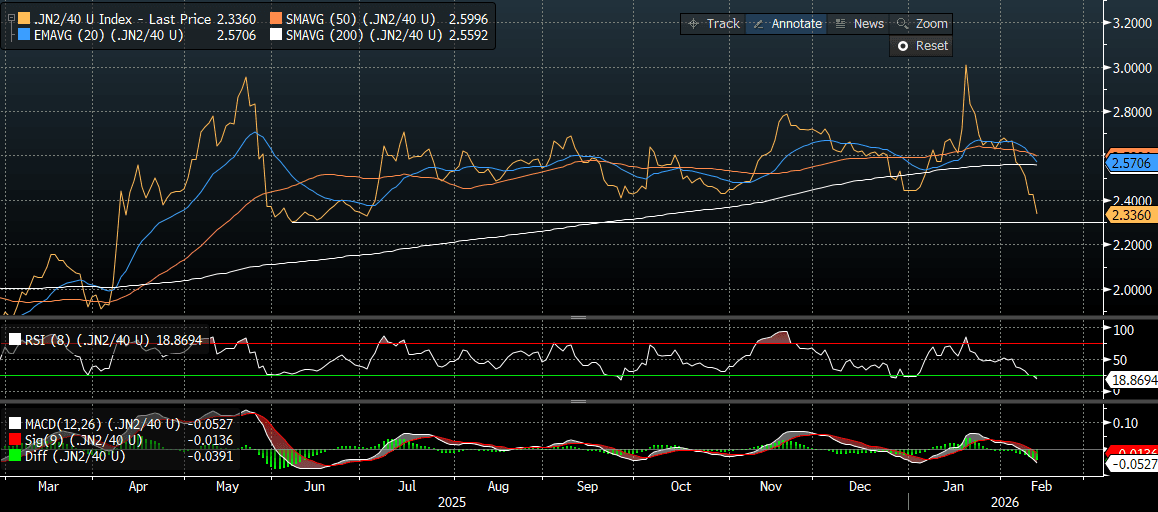

JGBS: Yield Curve Under Flattening Presure

After reaching a record steepness in mid-January, the 2/40 yield curve is now testing the lower bound of the well-defined range that has contained price action since mid-year.

- Since late last year, steepening has been most pronounced in the 2/5 segment, leaving the 5-year sector relatively unattractive on the curve. Into the recent election, expectations of fiscal expansion under a Takaichi administration implied heavier debt supply, reinforcing pressure on intermediates.

- In recent days, however, those fiscal concerns appear to have moderated following Prime Minister Sanae Takaichi’s historic election victory.

- Notably, while the 2/5 segment has flattened, it is the 5/40 curve which has broken through the bottom of the range it has traded in since June last year.

- This likely reflects two dynamics. First, renewed yen weakness could bring forward expectations of additional BOJ rate hikes, placing upward pressure on 5-year yields relative to the long end. Second, the 5-year sector has emerged — and is likely to remain — a preferred short among more tactical accounts. In particular, positioning in 5s30s flatteners appears to have scope to extend as the BOJ edges closer to another tightening step.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

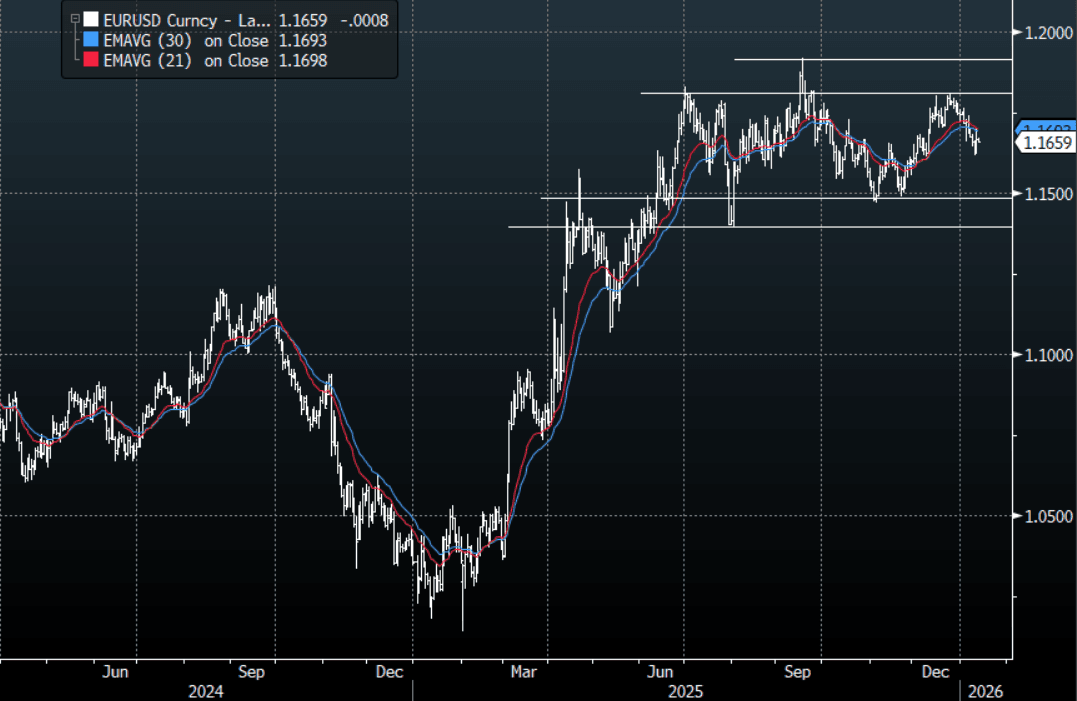

EUR: EUR/USD - 1.1700 Caps Move, Looks Like We Tread Water For Now

The overnight range was 1.1663 - 1.1699, Asia is currently trading around {EURUSD Curncy}. The pair found sellers again back toward 1.1700 capping the knee-jerk reaction to the Fed news. We are firmly back in the wider 1.1450-1.1850 range which dominated the last 6 months of the year and we need a catalyst to get a break and some sort of a trend going again. On the day it looks likely we tread water within a narrower 1.1600-1.1725 range as the market looks for a trigger to regain some momentum.

- The EUR/USD Average True Range for the last 10 Trading days: 43 Points

Fig 1 : EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

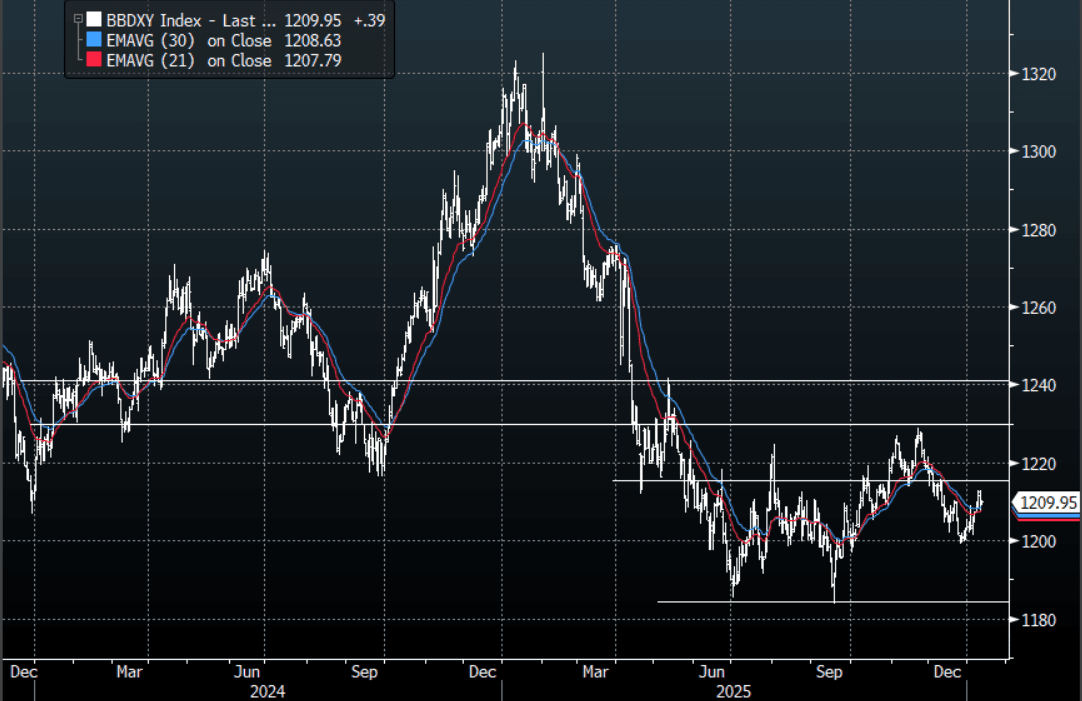

USD: BBDXY - Looks Directionless Within 1205-1215 For Now

The BBDXY range overnight was 1207.54 - 1210.11, Asia is currently trading around {BBDXY Index}. The USD found some support around the 1208 area after the initial knee-jerk lower. This leaves the USD in the middle of its recent range without any clear direction. On the day, it looks like 1205-1215 should cover it for now, watch for any ruling from the Supreme court as well as a potential incursion into Iran to maybe shake it up a little. This lack of a trend is being reflected in the CFTC data which shows very little positioning in the USD Index to start the year.

- MNI INTERVIEW: Fed Could Cut Around 100BP This Year-Bell. The Federal Reserve has ample room to keep cutting interest rates despite a robust economic backdrop because inflation excluding factors like shelter is already near target and the job market is effectively stalled, former IMF economist Gerwin Bell told MNI. {NSN T8R4IB6QRTHC <GO>}

- The BBDXY Average True Range for the last 10 Trading days: 339 Points

Fig 1: BBDXY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

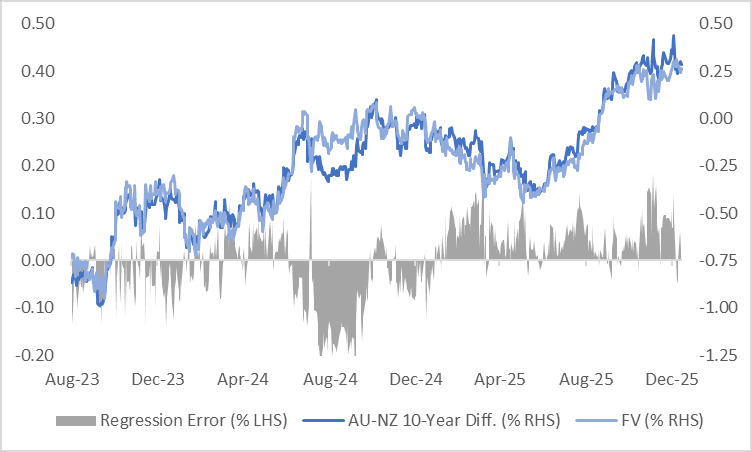

AUSSIE BONDS: AU-NZ10Y Diff Hovering Just Below Highs

The AU–NZ 10-year yield differential currently sits at +29bps, around 10bps below its recent peak of approximately +40bps, the widest since October 2020.

- The widening in the long-end spread has been mirrored by shifts in market expectations for the policy rate differential over the next year, as reflected in the AU–NZ 1-year forward 3-month swap (1Y3M) spread.

- Markets are presently pricing a 10-15bp narrowing of the AU–NZ 3-month rate spread over the next 12 months.

- Our Economics team’s central view is that both the RBA and the RBNZ are most likely to leave policy rates unchanged over the coming year.

- A simple regression analysis of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past two years shows that the 10-year differential is around 2bps above fair value based on the regression model.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. FV

Source: Bloomberg Finance LP / MNI