ASIA STOCKS: Taiwan Inflows Surge Pre LNY Break,Mostly Positive Trends Elsewhere

Taiwan remains a standout from an inflow standpoint, with a further +$1.8bn in net inflows yesterday. This has seen the 5-day sum and 2026 to date net inflows improve further. Still if we go back to the end of Jan, net inflows since then are close to flat, hence there is still scope for further upside momentum in flows. This will have to wait though with local equities now shut for the lunar new year break. They re-open on Feb 23rd. Familiar drivers remain in play for Taiwan stocks amid tech/AI, domestic growth, optimism.

- South Korean inflows continue to recover from recent outflow pressures. The Kospi has surged towards 5500, up 2.65%, to fresh record highs today. Per the NBUY function on BBG, we have seen nearly $1bn in more additional inflows today.

- In Indian, position inflow momentum persists, but the large chunky inflows seen post US-India trade headlines recently slowed somewhat. Indeed recent US statements which appear to change the fact sheet around the trade deal has created fresh uncertainty.

- In South East Asia, Indonesia remains the main negative, generally positive flow outcomes are evident elsewhere, consistent with positive local equity market trends.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2026 To Date | |

| South Korea (USDmn) | 599 | -4813 | -6040 |

| Taiwan (USDmn) | 1835 | 1930 | 3139 |

| India (USDmn)* | 35 | 808 | -1738 |

| Indonesia (USDmn)* | -42 | -142 | -742 |

| Thailand (USDmn) | 35 | 944 | 1192 |

| Malaysia (USDmn) | 72 | 133 | 379 |

| Philippines (USDmn) | 14 | 41 | 280 |

| Total (USDmn) | 2549 | -1099 | -3530 |

| * Data Up To Feb 10 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: CNH/JPY To Fresh Highs, Vols, RRs Unmoved Post Trump Iran-Tariff News

USD/CNH is holding marginally higher, last near 6.9715/20, with some spill over higher from higher USD/JPY levels likely impacting. However, CNH/JPY continues to make fresh highs above 22.7700, with yen remaining the epicentre of FX weakness in the first part of Tuesday trade. We also had only a modest downtick in the USD/CNY fixing earlier, while the error term widen, which may also be curbing downside interest in the pair on the day. For USD/CNH we arguably need to see a shift back above 7.0000 to drive a re-assessment of near term bearish momentum.

- Trump's earlier headline around a 25% tariff on anyone doing business with Iran may also be impacting, although the market be awaiting more details before judging the impact of this measure.

- 25% is under the average tariff rate that China currently faces from the US (30.8% per BBG). This fell in 2025 as the two-sides hashed out a trade truce.

- The general bias around risk reversal levels is firmer since the start of the year (perhaps hedging the break under 7.00), although reaction today has been fairly muted, suggesting limited impact from the Iranian/US headlines. It's a similar backdrop across the vol space, 1 month around 2.53%, so still close to recent cycle lows.

MNI EXCLUSIVE: Leading Labour Market Expert On RBA's 2026 Strategy

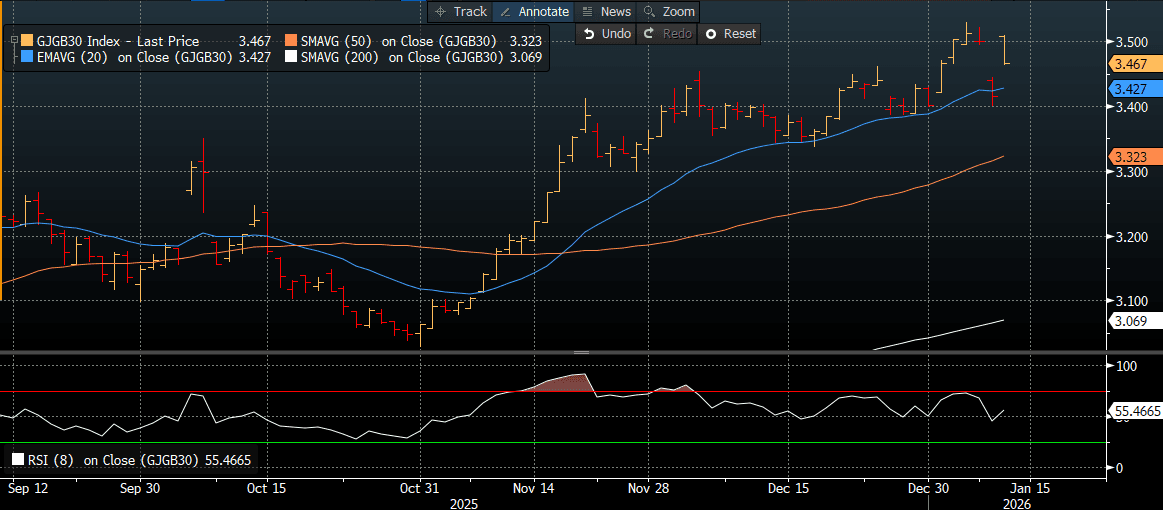

JGBS: Bear-Steeper Holding At Lunch But Long-End Yields Off Highs

At the Tokyo lunch break, JGB futures are weaker but above lows, -36 compared to settlement levels, as trading resumes after the long weekend.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s modest sell-off.

- Cash JGBs has bear-steepened across benchmarks, with yields 2-5bps higher. Long-end yields are, however, off session highs.

- (Bloomberg) “The 30-year government bond yield surges as much as 12 basis points to 3.52% on Tuesday, as speculation that Prime Minister Sanae Takaichi might dissolve the parliament as soon as next month grows following local media reports.”

- Nonetheless, today’s current move leaves the 2/10 curve around a fresh cycle, steepest since 2011.

- The benchmark 10-year yield is 4.4bps higher at 2.141% versus today’s fresh cycle high of 2.162%.

- Swap rates are mixed but little changed.

Source: Bloomberg Finance LP