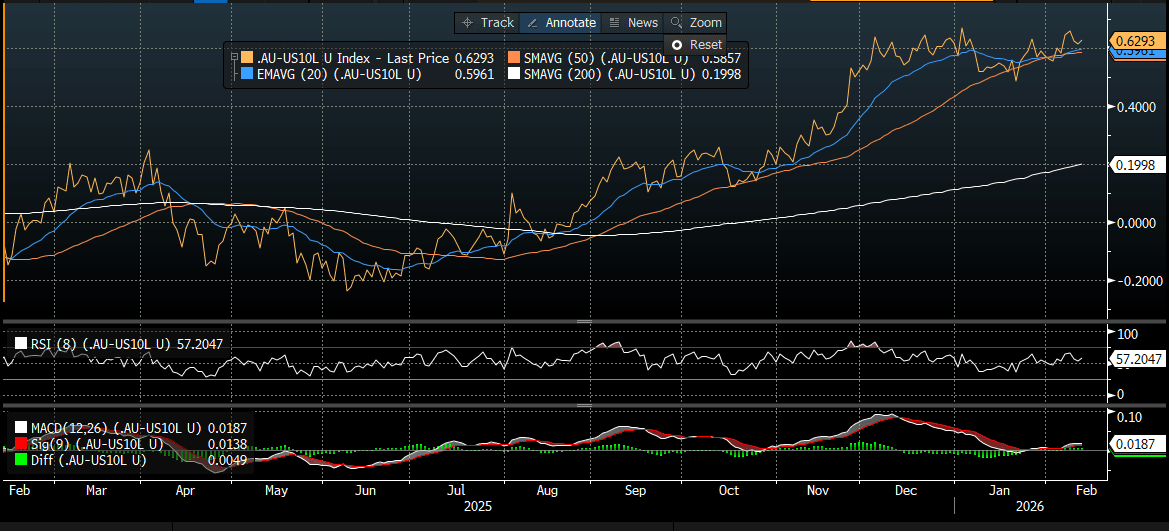

AUSSIE BONDS: Cheaper, RBA: Ready To Raise Rates Further, Infl Expns Up

ACGBs (YM -4.0 & XM -4.0) are weaker after dealing in relatively narrow ranges in today’s session.

- (Bloomberg) “Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said, stressing that the board remains cautious and is yet to decide whether further tightening is warranted. The Reserve Bank chief told a panel of senators on Thursday at Parliament House in Canberra that inflation running “with a three in front of it” is unacceptable."

- RBA Hunter is due to give a speech at a CEDA event in Perth (15:45 AEST).

- MI’s inflation expectations rose to 5% in February from 4.6% in January.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's post-payrolls sell-off.

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +63bps, just below its recent high.

- The bills strip has bear-steepened, with pricing -1 to -5.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 95% by June and 154% by December 2026.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 2.50% 21 May 2030 bond tomorrow.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: CNH/JPY To Fresh Highs, Vols, RRs Unmoved Post Trump Iran-Tariff News

USD/CNH is holding marginally higher, last near 6.9715/20, with some spill over higher from higher USD/JPY levels likely impacting. However, CNH/JPY continues to make fresh highs above 22.7700, with yen remaining the epicentre of FX weakness in the first part of Tuesday trade. We also had only a modest downtick in the USD/CNY fixing earlier, while the error term widen, which may also be curbing downside interest in the pair on the day. For USD/CNH we arguably need to see a shift back above 7.0000 to drive a re-assessment of near term bearish momentum.

- Trump's earlier headline around a 25% tariff on anyone doing business with Iran may also be impacting, although the market be awaiting more details before judging the impact of this measure.

- 25% is under the average tariff rate that China currently faces from the US (30.8% per BBG). This fell in 2025 as the two-sides hashed out a trade truce.

- The general bias around risk reversal levels is firmer since the start of the year (perhaps hedging the break under 7.00), although reaction today has been fairly muted, suggesting limited impact from the Iranian/US headlines. It's a similar backdrop across the vol space, 1 month around 2.53%, so still close to recent cycle lows.

MNI EXCLUSIVE: Leading Labour Market Expert On RBA's 2026 Strategy

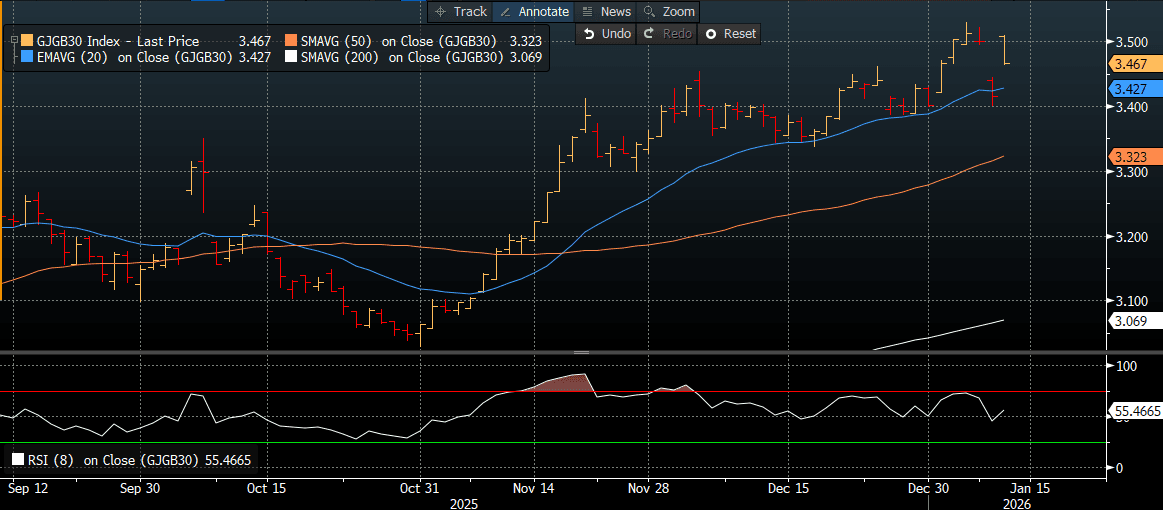

JGBS: Bear-Steeper Holding At Lunch But Long-End Yields Off Highs

At the Tokyo lunch break, JGB futures are weaker but above lows, -36 compared to settlement levels, as trading resumes after the long weekend.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s modest sell-off.

- Cash JGBs has bear-steepened across benchmarks, with yields 2-5bps higher. Long-end yields are, however, off session highs.

- (Bloomberg) “The 30-year government bond yield surges as much as 12 basis points to 3.52% on Tuesday, as speculation that Prime Minister Sanae Takaichi might dissolve the parliament as soon as next month grows following local media reports.”

- Nonetheless, today’s current move leaves the 2/10 curve around a fresh cycle, steepest since 2011.

- The benchmark 10-year yield is 4.4bps higher at 2.141% versus today’s fresh cycle high of 2.162%.

- Swap rates are mixed but little changed.

Source: Bloomberg Finance LP