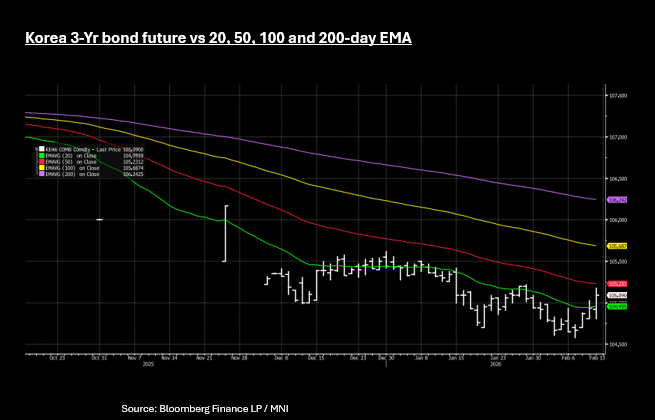

SOUTH KOREA: 3-Yr Rally on JGB Boost as Futures Above Key Tech Level

- The front end in Korea is seeing a strong move lower in yield today, following 3-Yr KTBs / IRS near 1-year highs recently.

- The BOK last cut rates in May 2025 and in January 2026 moved to a neutral bias, (from an easing bias) giving little steer for bond investors in the near term.

- Currently swaps models suggest little to no movement in rates for the first half of 2026, yet 3-Yr yields are almost +100bps higher from the lows of April last year.

- The short end in KTBs has been under pressure with significant amount of issuance in the 1-3Yr maturity bucket for KTBs. Today alone there is a KRW1.2tn 1-Year government bond being issued and impacts the front of the curve.

- Year to date issuance estimates are around 10-12% of total government issuance budgeted for the year is already done by mid February and focused in the 1-3-Yr. This has been the driver for the move higher

- Three year NDIRS are down -5bps in yield today on no news domestically. Correlations with JGBs have been strong post the election result in Japan and short end JGBs are down today - whilst short end USTs are doing very little.

- KTB bond futures didn't react initially to the rally in JGBs but once the orders at open were done, are strong today with the 3-Yr up +.16 to 105.10 and for the first time in February is back above the 20-day EMA of 104.95. Above is the 50-day EMA of 105.23 as topside resistance.

- KTB moves at present are very technically driven, given the limited expectation for interest rates in the near term investors are looking for catalysts elsewhere. Watch closely ongoing JGB moves for guides, with correlations up over +.35 at present .

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

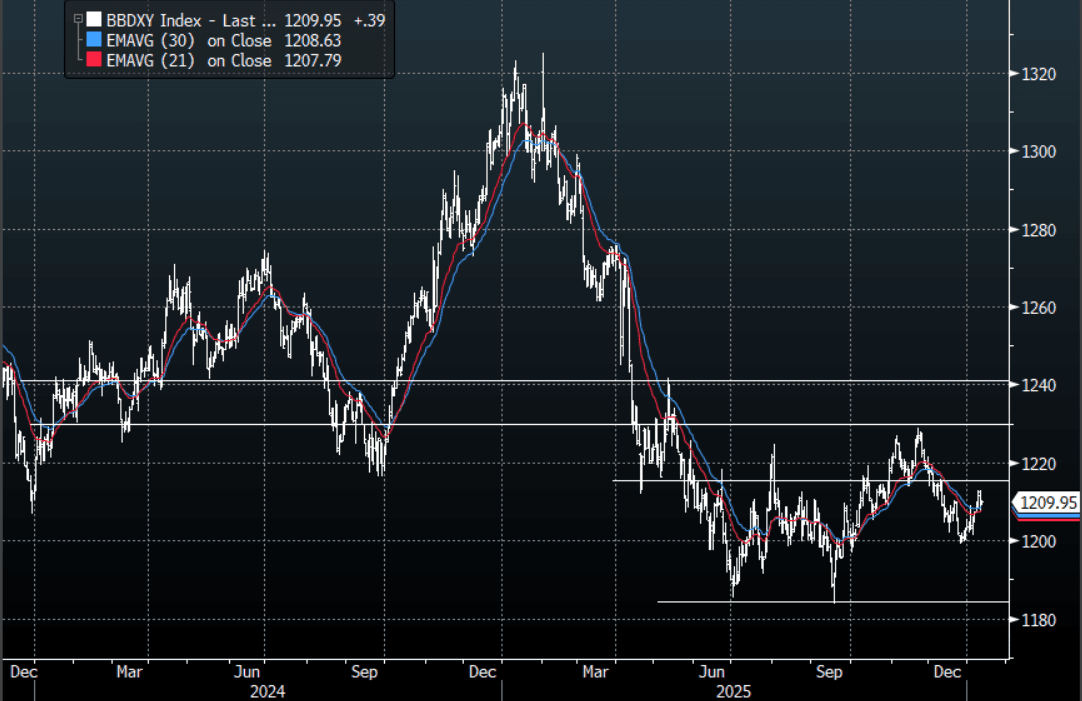

USD: BBDXY - Looks Directionless Within 1205-1215 For Now

The BBDXY range overnight was 1207.54 - 1210.11, Asia is currently trading around {BBDXY Index}. The USD found some support around the 1208 area after the initial knee-jerk lower. This leaves the USD in the middle of its recent range without any clear direction. On the day, it looks like 1205-1215 should cover it for now, watch for any ruling from the Supreme court as well as a potential incursion into Iran to maybe shake it up a little. This lack of a trend is being reflected in the CFTC data which shows very little positioning in the USD Index to start the year.

- MNI INTERVIEW: Fed Could Cut Around 100BP This Year-Bell. The Federal Reserve has ample room to keep cutting interest rates despite a robust economic backdrop because inflation excluding factors like shelter is already near target and the job market is effectively stalled, former IMF economist Gerwin Bell told MNI. {NSN T8R4IB6QRTHC <GO>}

- The BBDXY Average True Range for the last 10 Trading days: 339 Points

Fig 1: BBDXY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

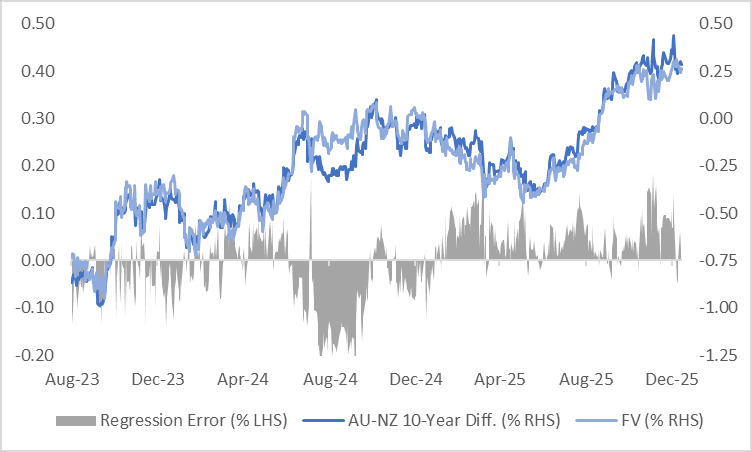

AUSSIE BONDS: AU-NZ10Y Diff Hovering Just Below Highs

The AU–NZ 10-year yield differential currently sits at +29bps, around 10bps below its recent peak of approximately +40bps, the widest since October 2020.

- The widening in the long-end spread has been mirrored by shifts in market expectations for the policy rate differential over the next year, as reflected in the AU–NZ 1-year forward 3-month swap (1Y3M) spread.

- Markets are presently pricing a 10-15bp narrowing of the AU–NZ 3-month rate spread over the next 12 months.

- Our Economics team’s central view is that both the RBA and the RBNZ are most likely to leave policy rates unchanged over the coming year.

- A simple regression analysis of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past two years shows that the 10-year differential is around 2bps above fair value based on the regression model.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. FV

Source: Bloomberg Finance LP / MNI

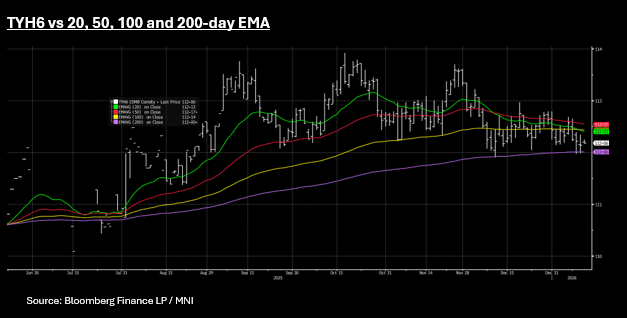

US TSYS: UST Flows Limited, TYH6 Wedged between Key Tech Levels

US bond futures are all modestly higher in the Asia trading day today. The 10-Yr is up +01+ to 112-06, having fallen modestly during the US trading day. TYH6 remains near to the mid-point from its topside resistance in the 100-day EMA at 112-14+ and the downside resistance from the 200-day EMA at 112-00+. Futures are have traded in relatively tight ranges in recent days as expectations for the January FED meeting diminish.

Cash is relatively unchanged Tuesday with turnover muted.

- The 2-Yr is at 3.537%

- The 5-Yr is at 3.7596% up +0.3bps

- The 10-Yr is at 4.179%

- The 30-yr is at 4.827% down -0.2bp.

The upcoming CPI will be the last major data report ahead of the Fed's end-January meeting, but is very unlikely to sway the FOMC away from holding rates as is heavily priced (only about 1bp of cuts implied by futures), yet a strong reading will unlikely be taken as an early warning given data quality questions remain.

Overnight there was a US$86bn 13-week, US$77bn 26-week, a US$58bn 3-Yr and a re-opening of 10-Yr notes auction. With the exception of the 3-Year which was flat, the other auctions a saw modestly stronger bid to cover relative to the last auction of same maturity.

Tonight there is a US$75bn 6-week auction and a US$22bn 30-Year reopening.