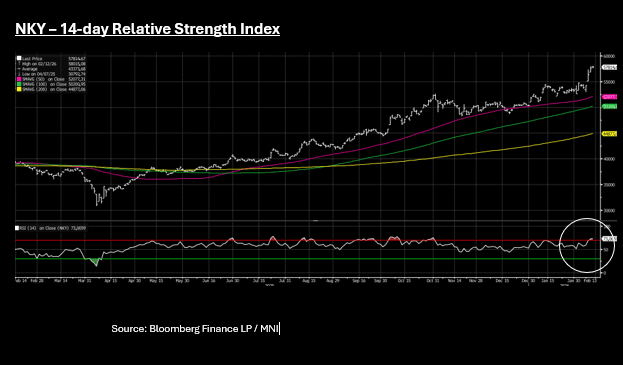

ASIA STOCKS: KOSPI & NKY Hit New Highs; NKY Reaches Overbought on 14RSI

The Nikkei returned from holiday today but couldn't replicate the gains from earlier in the week. Up just +0.25% today it takes the index to over 6% higher for the week on a day when the long end of the JGB curve rallied strongly, retracing losses from January February. Currently at 57,800 the NKY has reached yet another new high, having delivered year to date gains over 10%. The gains have seen the NKY reach Overbought on the 14RSI - which could dampen near term further gains.

News that a potential rescue package could be announced by the Shenzhen government to the tune of CNY80bn did little to impact China's major equity markets Thursday with the HSI down -0.85 and onshore bourses posting only modest gains. Other key real estate names in HK did however receive a boost with Sun Hung Kai Properties one of the main gainers for the index.

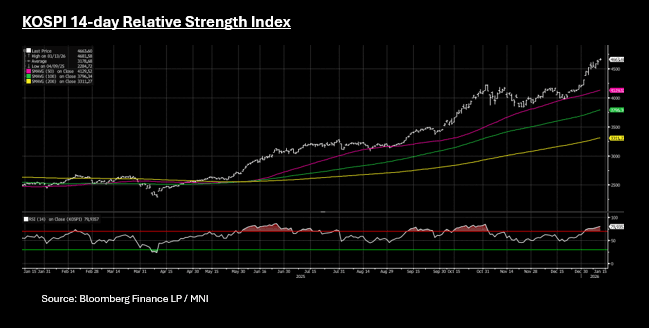

Ongoing strength of inflows is a fundamental support for the TAIEX in Taiwan with gains of +1.6% today ahead of LNY, as TSMC rose over 2% to a new record of TWD1,915. The KOSPI had a strong day also with key AI names SK Hynix up +2.5% and Samsung up +6.00% contributing to the KOSPI's gain of +2.6%. Earlier the KOSPI hit a new high of 5,515 only to moderate back to 5,498

The JCI sits on gains of over 4% for the week despite modest falls Thursday, as President Prabowo's heads to the US where it is intended he signs the US trade deal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Marginally Higher, Awaiting CPI Release

US bond futures were stable today with only modest gains across most maturities. The 10-Yr is up +01 at 112-05+ to maintain its position near the mid point of the 20-day EMA of 112-13+ and the downside resistance from the 200-day EMA at 112-00+.

Cash was quiet as yields were marginally higher across the curve.

- The 2-Yr is up +0.6bps at 3.543%

- The 5-Yr is up +0.5bps at 3.762%

- The 10-Yr is up +0.4bps at 4.183%

- The 30-Yr is up +0.3bps at 4.832%

The upcoming CPI will be the last major data report ahead of the Fed's end-January meeting, but is very unlikely to sway the FOMC away from holding rates as is heavily priced (only about 1bp of cuts implied by futures), yet a strong reading will unlikely be taken as an early warning given data quality questions remain.

Tonight there is a US$75bn 6-week auction and a US$22bn 30-Year reopening.

ASIA STOCKS: NKY at New High as Yen Weakens, KOSPI Overbought on RSI

- The NIKKEI is up over 3.2% to a new record of 53,639 as USDJPY nears 158.76 in afternoon trade, giving Japan exporters a boost.

- The KOSPI is up +0.90% for a seventh successive day of gains. At 4,666 the KOSPI is just 7% below the South Korean presidents stated target of 5,000. Reaching overbought on the 14-day relative strength index at the start of the new year and today's move consolidates the index further above.

- China's bourses were mixed with the Hang Seng leading the way, gaining 1% whilst the CSI is flat and Shanghai and Shenzhen down modestly. More news from China Vanke and a potential further extension request didn't help sentiment.

- India's NIFTY 50 is down -0.12% having staged a rally into the close Monday to deliver its first (modest gains of the year).

- SE Asia's bourses are mixed with the SE Thai down -0.40%, FTSE Malay up +0.5% and JCI flat.

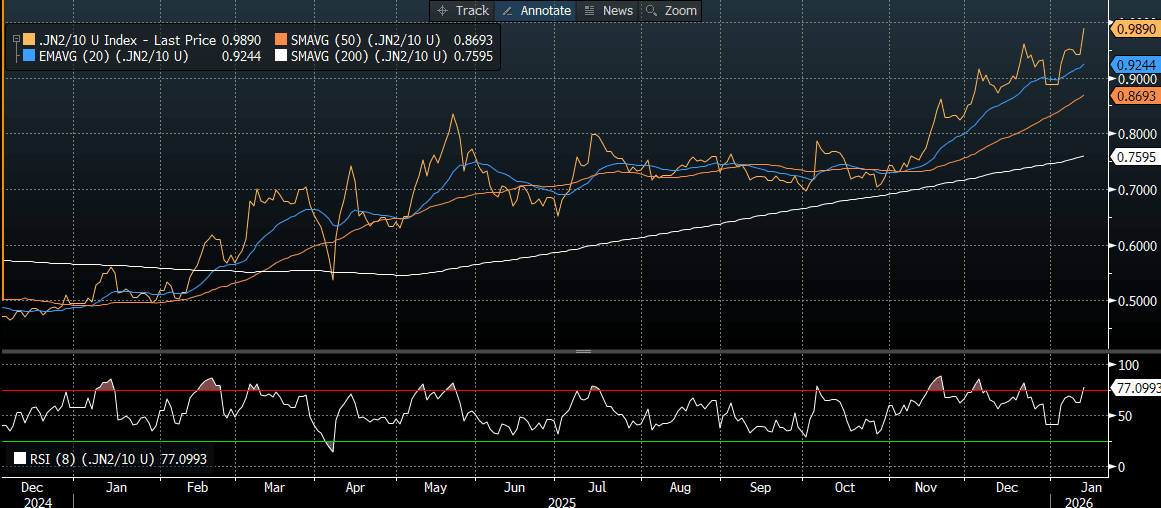

JGBS: Bear-Steeper Tied To Election Fears, 5Y Supply Tomorrow

JGB futures are weaker but above lows, -39 compared to settlement levels, as trading resumed after the long weekend.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday's modest sell-off.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 5bps higher. Long-end yields are, however, off session highs.

- Longer-dated bond yields have been pressured by speculation that Prime Minister Sanae Takaichi might dissolve the parliament as soon as next month following local media reports.

- Consistent with today’s move, Bloomberg reported that “Japanese investors sold the most UK sovereign bonds in 14 years in November, with concern over Britain’s fiscal outlook and higher yields in the domestic market sapping demand for gilts.”

- Today's current move leaves the 2/10 curve at a fresh cycle, steepest since 2011 (see chart).

- Swap rates are mixed but little changed.

- Tomorrow, the local calendar will see Money Stock and Machine Tool Orders alongside 5-year supply.

Source: Bloomberg Finance LP