CHINA: 10-Yr CGB Resets Near Term Range to 1.70-1.80%

- CGB bond yields have moved lower Thursday, following another day of sizeable liquidity injections. With injections tipped to be significant this week ahead of the lunar new year holiday, we noted in recent posts that the risks were skewed to the downside for 10-yr bond yields. https://cms.mnimarkets.com/news/edit/story/317098, especially given the CPI miss.

- Week to date the PBOC has injected over CNY1tn of liquidity, utilizing a variety of maturities and with equity markets mixed currently, we anticipated some found find its way into the 10-Yr CGB.

- The 10-Yr is down -1.8bps to 1.781% its lowest since September 2025. Back in September expectations for for GDP growth was 4.5-4.7%, in line with the 2026 forecast of 4.5%.

- As we approach the March NPC meeting, expectations are growing for monetary action with RRR cuts favoured, whilst some suggest a rate cut could be forthcoming.

- Either will provide good support for bonds and could see the 10-Yr range shift down to 1.70-1.80% in the near term.

- Bond futures are only up modestly Thursday with the 10-Yr up +.04 at 108.605 - but taking it to overbought on the RSI. Whilst China bond futures may not react necessarily to tech levels, it is important to note the change in momentum.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Leading Labour Market Expert On RBA's 2026 Strategy

JGBS: Bear-Steeper Holding At Lunch But Long-End Yields Off Highs

At the Tokyo lunch break, JGB futures are weaker but above lows, -36 compared to settlement levels, as trading resumes after the long weekend.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s modest sell-off.

- Cash JGBs has bear-steepened across benchmarks, with yields 2-5bps higher. Long-end yields are, however, off session highs.

- (Bloomberg) “The 30-year government bond yield surges as much as 12 basis points to 3.52% on Tuesday, as speculation that Prime Minister Sanae Takaichi might dissolve the parliament as soon as next month grows following local media reports.”

- Nonetheless, today’s current move leaves the 2/10 curve around a fresh cycle, steepest since 2011.

- The benchmark 10-year yield is 4.4bps higher at 2.141% versus today’s fresh cycle high of 2.162%.

- Swap rates are mixed but little changed.

Source: Bloomberg Finance LP

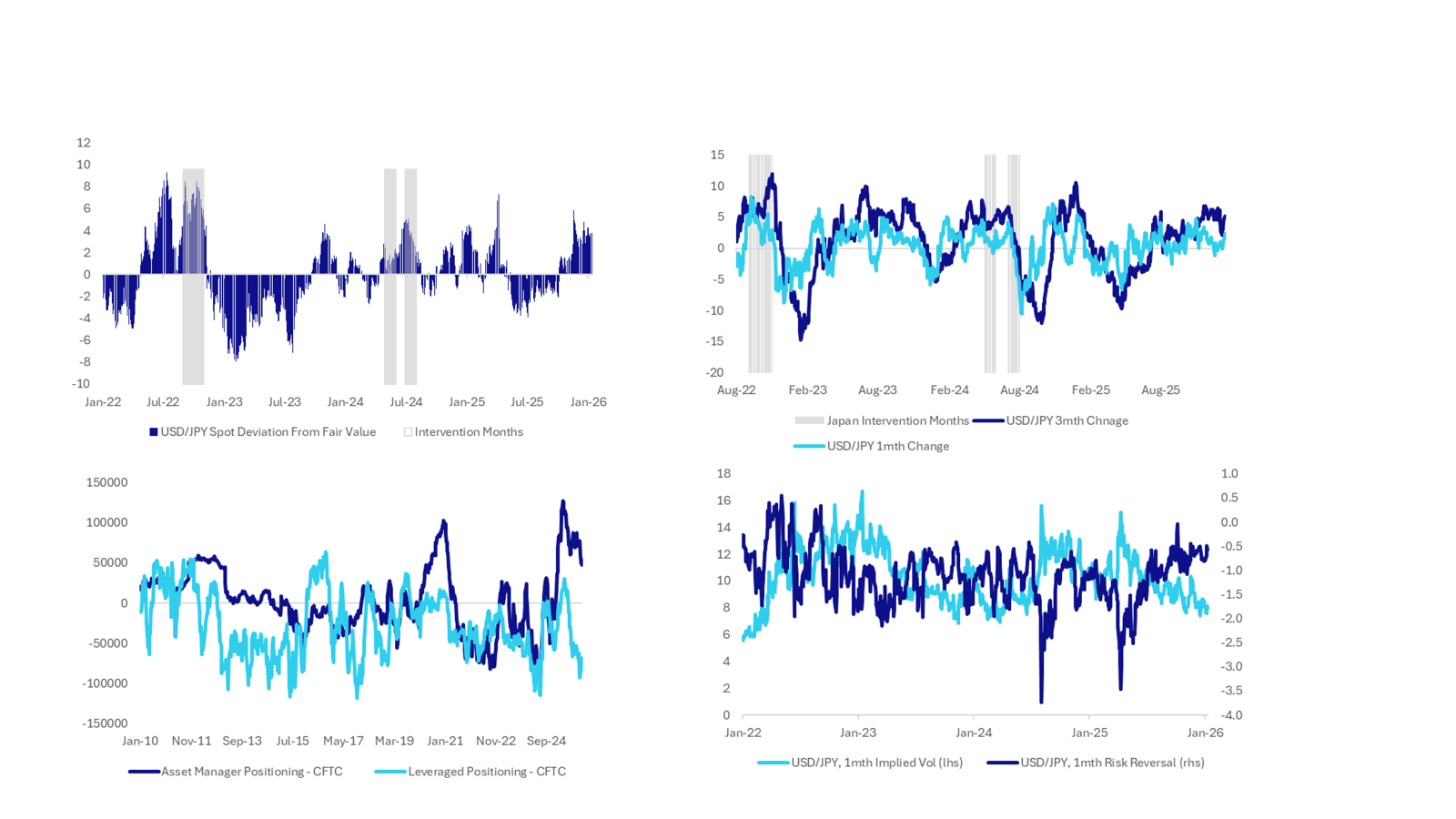

JPY: USD/JPY Breaks Higher, Intervention Threat Returns

The clear break above 158.00 in USD/JPY has seen fresh jawboning emerge from Japan officials, although net market impact remains minimal at this stage. Earlier FinMin Katayama stated concern around one-sided FX moves, which she shared with US Tsy Bessent in recent talks (who also agreed with the FinMins concern) . The Deputy Chief Cabinet Secretary Ozaki has reiterated concern this around one-sided, sharp FX moves and stated the government is ready to take steps to tackle excess volatility, including speculative moves. Broadly the market, for now at least, is taking these comments in its stride, and appears comfortable to continue to test the authorities resolve. We were last at fresh highs of 158.65/70. Below is a series of charts that we monitor, they arguably show intervention risks are heightened, but no more so than they were in late 2025.

- USD/JPY spot remains comfortably above our simple fair value estimate (see top left hand panel), which is written off US-JP 2y swap spreads and global equities. The differential between the two is back around 4% amidst a resilient global equity backdrop (fair value around 152.4). The wedge did close close to 6% in Nov last year.

- The 1month and 3 months rate of change are trending back up, but also remain sub late 2025 highs, top right hand panel chart.

- Market positioning shows leveraged contracts short, per CFTC, but asset managers still long, see the bottom left hand panel chart. The authorities will tend to focus more on speculative positioning (proxied by leveraged contracts), but aggregate positioning (leveraged + asset manager) is not as short as it was in 2022 or 2024 (close to -150k in 2022, -200k at its trough point in 2024, current is around -20k).

- The bottom right hand panel is the 1 month risk reversal and 1 month implied vol. Risk reversals are sub late 2025 highs, while implied vols are painting a fairly benign backdrop, which fits with a still supportive carry back drop for USD/JPY from a broader risk standpoint.

Fig 1: USD/JPY - Various Metrics Compared To Prior Intervention Episodes

Source: Bloomberg Finance L.P./MNI