MNI EUROPEAN MARKETS ANALYSIS: Strong Weekly Gains for Stocks

- Stocks surged into the end of the week as the ceasefire pleased markets, even as oil price gains continued from Wednesday's lows.

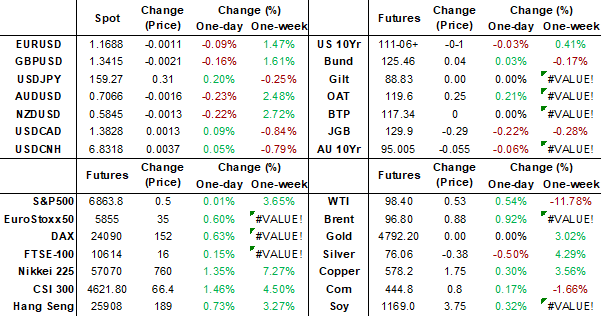

- US treasury yields have inched higher again, with the 10-YR retesting 4.30% along with oil.

- WIth the momentum coming out of the USD, most regional currencies have performed strongly with some well off recent highs.

- Looking ahead there is various European CPIs, Italian Industrial Production ahead of the key release: US CPI for March.

US TSYS: 10-Yr Eyes 4.30%; CPI Could Support the Move Higher

Yields are moved higher in the Friday afternoon as oil prices rise as uncertainty around the ceasefire grows. UST yields are up around 1.5 - 2.5bps across the curve in a low volume day to end the week. The 10-Yr US bond future is up +01 at 111-08 to remain just north of the 20-day EMA of 111-05+ which it has tracked in recent sessions.

- The 2-Yr is up +1.8bps at 3.793%

- The 5-yr is up +2.1bps at 3.92%

- The 10-Yr is up +2.2bps at 4.299%

- The 30-Yr is up +1.6bps at 4.90%

A consolidated break above 4.30% in the US Friday could suggest a resumption of the move higher in yields. The CPI release could provide some impetus there in a week where on balance, the Fed Speakers rhetoric has been hawkish.

Friday Data Calendar: CPI, UofM Sentiment, Durables/Cap Goods

US Data/Speaker Calendar (prior, estimate). All times ET

04/10 0830 Real Avg Wkly Earnings YoY (1.7%, --). Hourly Earning YoY (1.4%, --)

04/10 0830 CPI MoM (0.3%, 0.9%), YoY (2.4%, 3.4%)

04/10 0830 Core CPI MoM (0.2%, 0.3%), YoY (2.5%, 2.7%)Table of Contents

JGBS: Futures-Linked 7Y Leads Market Cheaper

JGB futures are weaker and session cheaps, -34 compared to settlement levels.

- Japan's corporate goods price index rose 2.6% y/y in March, accelerating from February's 2.1%, while import prices rose for a fourth straight month, data released by the Bank of Japan showed on Friday.

- [MNI EXCLUSIVE] The BOJ's former chief economist shares his policy rate outlook. On MNI Policy MainWire now.

- Bank of Japan Deputy Governor Ryozo Himino said on Friday that the BOJ will manage monetary policy appropriately while remaining mindful of the risk of stagflation, with a focus on achieving its 2% price target. He said Japan is not currently in stagflation, noting that CPI is moving close to the 2% target and GDP is growing above its potential rate. However, he added that the BOJ must remain alert to the risk of stagflation if the Middle East conflict is prolonged.

- Cash US tsys are ~2bps in today's Asia-Pac session after yesterday's modest bull-flattener.

- Cash JGBs are 0.5bp richer (40-year) to 5bps cheaper (7-year) across benchmarks. The benchmark 10-year yield is 4bps higher at 2.432% versus the cycle high of 2.441%.

- Swap rates are flat to 2bps higher.

Source: Bloomberg Finance LP

AUSSIE BONDS: Grinds Cheaper Through The Session, US CPI Data Due

ACGBs (YM -4.0 & XM -4.5) are cheaper with US tsys.

- Cash US tsys are ~2bps in today’s Asia-Pac session after yesterday's modest bull-flattener.

- Friday US Data Calendar: CPI, UofM Sentiment, Durables/Cap Goods.

- "US, Iran Prepare for Talks With Lebanon Conflict Unresolved" - BBG

- Zerohedge on X: "If this ceasefire breaks and the US resumes its military campaign, that would be the beginning of a 'worst case scenario' where civilian infra is targeted..., WTI makes new highs and Equities make new lows. The feel of a binary outcome is likely to paralyze investors"- JPMorgan

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +66bps.

- The bills strip has bear-steepened, with pricing +1 to -3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 67% for May to 160% by August and 232% by December 2026.

- On Monday, the local calendar will be empty, ahead of Consumer and Business Confidence on Tuesday and March’s Employment Report on Thursday.

- Next week, the AOFM plans to sell A$1000mn of the 4.25% 21 October 2036 bond on Wednesday and A$1000mn of the 1.50% 21 June 2031 bond on Friday.

BONDS: NZGBS: Closed Little Changed After A Relatively Subdued Session

NZGBs closed little changed, with benchmark yields flat to 1bp higher, after giving up early gains.

- Bloomberg "RBNZ to Wait for Second-Quarter Data Before Rate Hike: Kiwibank. "The RBNZ is not going to make any moves until they have data in front of them. Q2 data, where the true impact of the oil crisis on the kiwi economy will really start to show, won't be available until June/July."

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest bull-flattener.

- The NZ-US 10-year yield differential hovers just below recent highs at +41bps.

- RBNZ-dated OIS pricing is little changed across meetings today but remains 5-26bps firmer than Wednesday’s pre-RBNZ levels.

- Interest-rate expectations across the $-bloc through December 2026 were mixed over the past two weeks, amidst ongoing uncertainty around the Middle East conflict and its implications for oil prices.

- Markets in the US and Canada softened by 22bps and 32bps, respectively, while Australia (-5bps) and New Zealand (+2bps) were relatively little changed.

- Nevertheless, relative to late February, December 2026 pricing remains 28-50bps firmer across the $-bloc, with the US leading and Australia lagging.

- On Monday, the local calendar will see Performance Services Index, ahead of Net Migration on Tuesday.

Bloomberg Finance LP

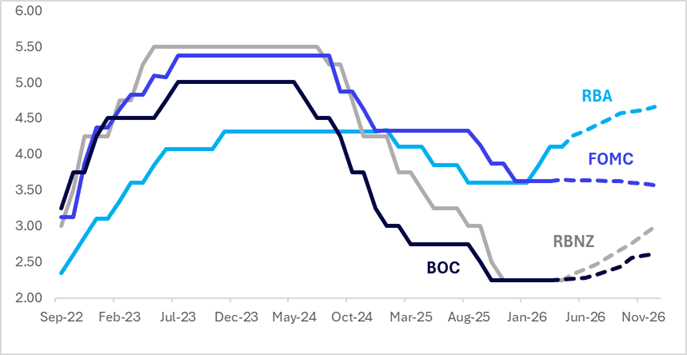

STIR: $-Bloc Year-End Pricing Mostly Softer Over Past Two Weeks

Interest-rate expectations across the $-bloc through December 2026 were mixed over the past two weeks, amidst ongoing uncertainty around the Middle East conflict and its implications for oil prices.

- Markets in the US and Canada softened by 22bps and 32bps, respectively, while Australia (-5bps) and New Zealand (+2bps) were relatively little changed.

- Nevertheless, relative to late February, December 2026 pricing remains 28-50bps firmer across the $-bloc, with the US leading and Australia lagging.

- In terms of recent events in the $-bloc, April 8th’s RBNZ policy meeting highlighted.

- In a unanimous decision, the RBNZ kept rates at 2.25% but warned that it is prepared to hike if inflation is not expected to return to the 2% band mid-point over the medium term. If core and wage inflation as well as inflation expectations aren’t contained “decisive and timely increases in the OCR would be required”.

- The MPC discussed whether to hike rates to pre-emptively act against rising inflation but the discussion was balanced looking at the risks to the already soft recovery from higher fuel prices.

- The next major regional policy events are the FOMC and BOC policy meetings on 29 April. Currently, the market attaches little chance of movement by either central bank.

- Looking ahead to December 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.57%, +6bps; Canada (BOC): 2.61%, +36bps; Australia (RBA): 4.41%, +31bps; and New Zealand (RBNZ): 2.99%, +74bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

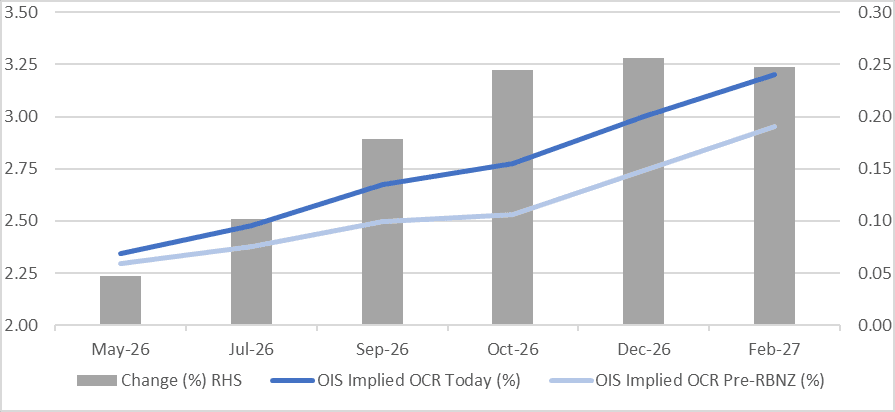

STIR: RBNZ-Dated OIS Pricing Little Changed But Firmer Than Pre-RBNZ

RBNZ-dated OIS pricing is little changed across meetings today, but remains 5-26bps firmer than Wednesday’s pre-RBNZ levels.

- In a unanimous decision, the RBNZ kept rates at 2.25% but warned that it is prepared to hike if inflation is not expected to return to the 2% band mid-point over the medium term. If core and wage inflation as well as inflation expectations aren’t contained “decisive and timely increases in the OCR would be required”.

- RBNZ Governor Anna Breman signalled expectations for somewhat weaker economic growth in New Zealand, with firms likely to act more cautiously in the near term. While the outlook has softened, she noted the Bank does not currently expect the economy to contract. The RBNZ remains focused on returning inflation to the 2% midpoint and is closely monitoring any signs that core inflation could rise.

- Pricing is now 4-21bps firmer than yesterday’s pre-RBNZ levels.

- 9bps of tightening is priced for May, while February 2027 assigns 95bps.

Figure 1: RBNZ Dated OIS Current vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

FOREX: USD - BBDXY Move Lower Stalls Below 1200 As Peace Talks Loom

The BBDXY has had a range today of 1199.56 - 1200.89 in the Asia-Pac session; it is currently trading around 1200. The USD continues to find demand just below 1198 ahead of the weekend talks. The price action continues to highlight how bearish the market is on the USD and are very quickly to re-enter the trade. The USD bears will probably hold off trying to add to their positions until we hear news out of the talks this weekend, this leaves us probably chopping around in no-man's land until then. On the day, I suspect a rally back towards 1205-1208 could now find sellers initially and we will probably trade 1195-1210 until we get some clarity. I continue to see the two countries' objectives for these talks to be poles apart and unless there is some serious coercion from China I struggle to see how a deal is made. The market prefers to have a more positive take with some like Robin Brooks believing the pressure from US midterms will be enough to get a deal done, let's see how this weekend plays out.

- EUR/USD - Asian range 1.1686-1.1704, Asia is currently trading 1.1695. The pair topped out again above 1.1700 overnight as the market looks toward the weekend peace talks for direction. The market's optimism for a deal should keep the EUR supported for now on dips, let's see what the outcome brings us. On the day, I suspect the market will chop around into the weekend, with participants loathe to add any fresh risk until we get clues as to the possibility of a clear resolution and what it looks like. So a wide and choppy 1.1600-1.1800 should cover it.

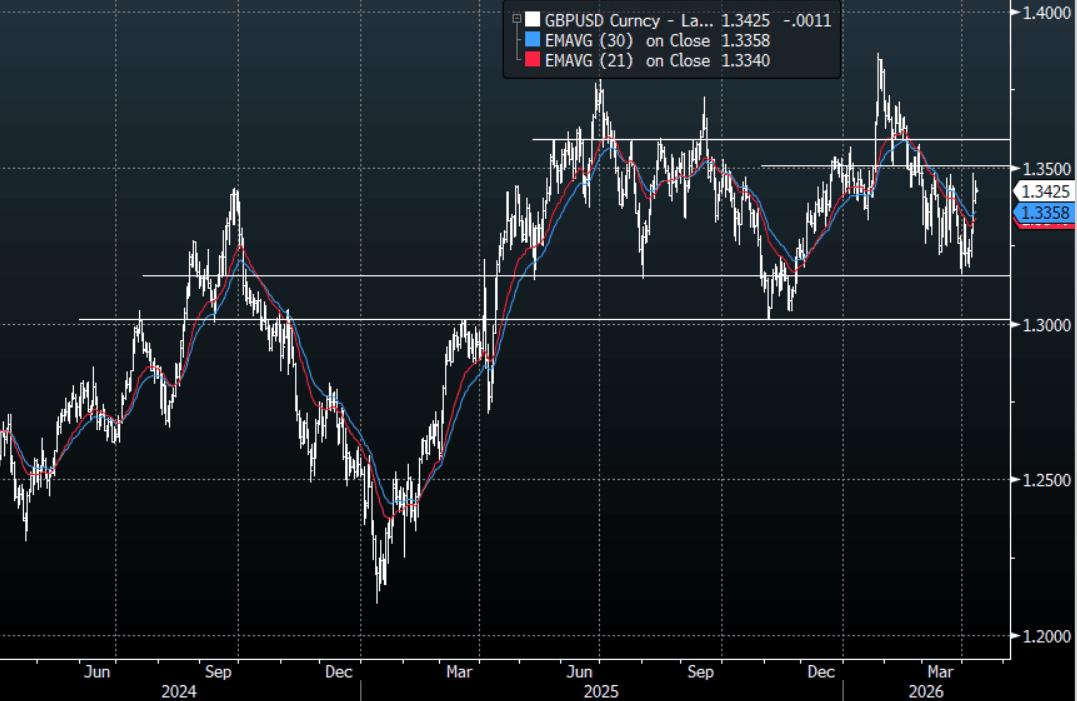

- GBP/USD - Asian range 1.3420-1.3437, Asia is currently dealing around 1.3425. The pair’s move higher continues to stall just ahead of 1.3500 for now. On the day, the pair remains within its recent 1.3200-1.3500 range with the bears hoping the 1.3500-13600 area holds or we could see some further paring back of shorts and the potential medium top would fade into memory.

- Data: ECB’s Guindos Speaks, US March CPI, US April University of Michigan Sentiment

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

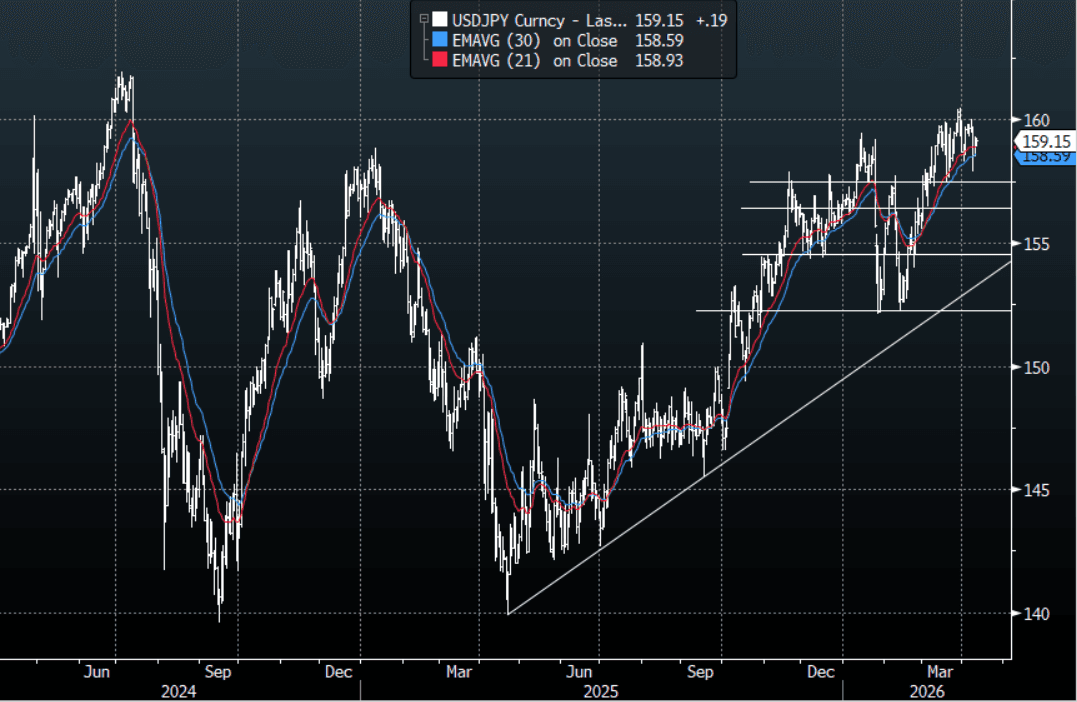

JPY: USD/JPY - Chops Around 159.00 As Peace Talks Loom

The USD/JPY range today has been 158.95-159.24 in the Asia-Pac session, it is currently trading around 159.15, +0.10%. The pair continued to chop around the 159.00 area in our session with no clear direction. Some more Jaw-boning today from Japanese officials but the market is not reacting. The market is very quick to jump back on the sell the USD train, but it looks until we get some clearer feedback from the weekend talks the market might have to sit on its hands. On the day, the first support is toward 158.00-158.50 and rallies toward 159.50 should see sellers initially. I suspect we could be stuck in a wider choppy 158.00-160.00 range until we see what magic JD Vance can bring to the table.

- MNI BRIEF: Japan March CGPI Rises 2.6% Y/Y; Import Price Rises. Japan's corporate goods price index rose 2.6% y/y in March, accelerating from February’s 2.1%, while import prices rose for a fourth straight month.

- MNI BRIEF: BOJ To Manage Policy Timely On Stagflation - Mimino. Bank of Japan Deputy Governor Ryozo Himino said on Friday that the BOJ will manage monetary policy appropriately while remaining mindful of the risk of stagflation, with a focus on achieving its 2% price target.

- “KATAYAMA: REFRAIN FROM COMMENTING ON FX LEVELS, WILL TAKE COMPREHENSIVE MEASURES IN ALL AREAS ON FX. HAVE LONG MENTIONED POSSIBLE BOLD ACTIONS ON FX, HEARING OF INCREASING SPECULATIVE MOVES IN FX MARKET” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 158.00($1.89b), 159.50($780m), 160.00($1.12b). Upcoming Close Strikes : 158.00($1.07b April 15), 158.85($1.23b April 15) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 80 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

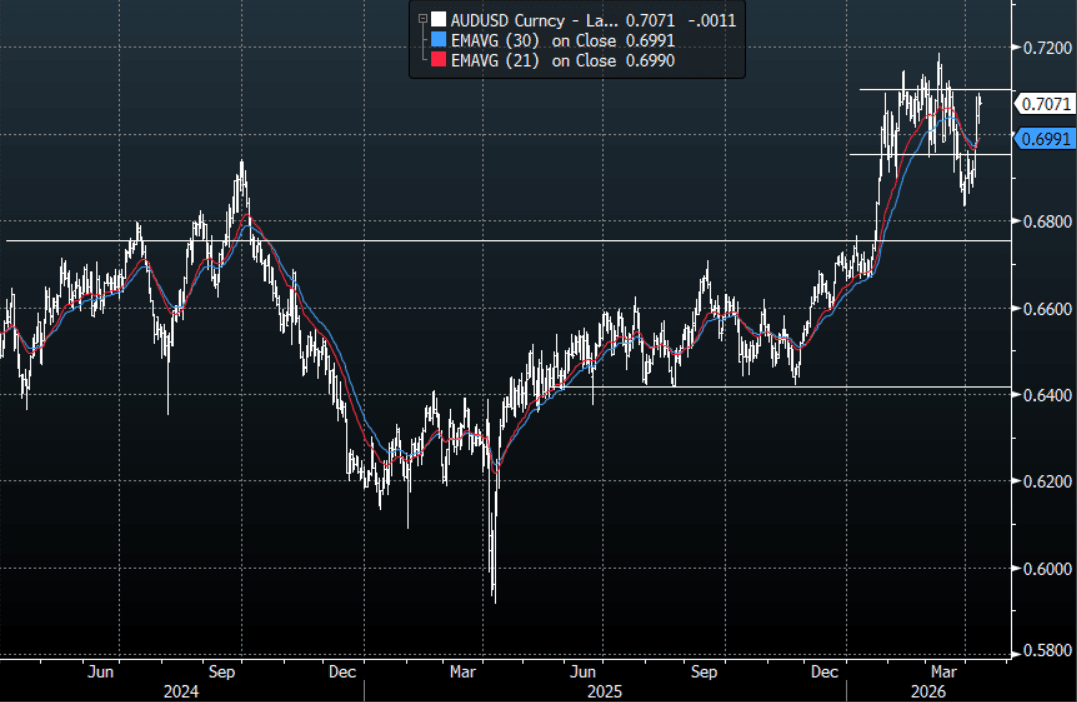

AUD/USD - Drifts Lower In A Quiet Asian Session

The AUD/USD has had a range today of 0.7067-0.7087 in the Asia- Pac session, it is currently trading around 0.7070,-0.15%. The AUD has drifted lower in a quiet Asian session after stalling toward 0.7100 overnight. I suspect until we see what those talks over the weekend bring we could be sitting in limbo as this market could really go either way from here. On the day, the first support is back toward 0.7020-0.7050, AUD bulls will be looking for this to hold for another test of the 0.7100 area, though I suspect a sustained break higher might be a lot to ask for with the event risk to come. I suspect we trade 0.6950-0.7150 until we get clarity from the talks, should make it a lively Asian open next week.

- "US, Iran Prepare for Talks With Lebanon Conflict Unresolved" - BBG

- Zerohedge on X: "If this ceasefire breaks and the US resumes its military campaign, that would be the beginning of a ‘worst case scenario’ where civilian infra is targeted..., WTI makes new highs and Equities make new lows. The feel of a binary outcome is likely to paralyze investors"- JPMorgan

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6900(AUD393m). Upcoming Close Strikes : 0.6900(AUD1.57b April 15), 0.6965(AUD966m April 14), 0.7125(AUD1.35b April 15) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 65 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

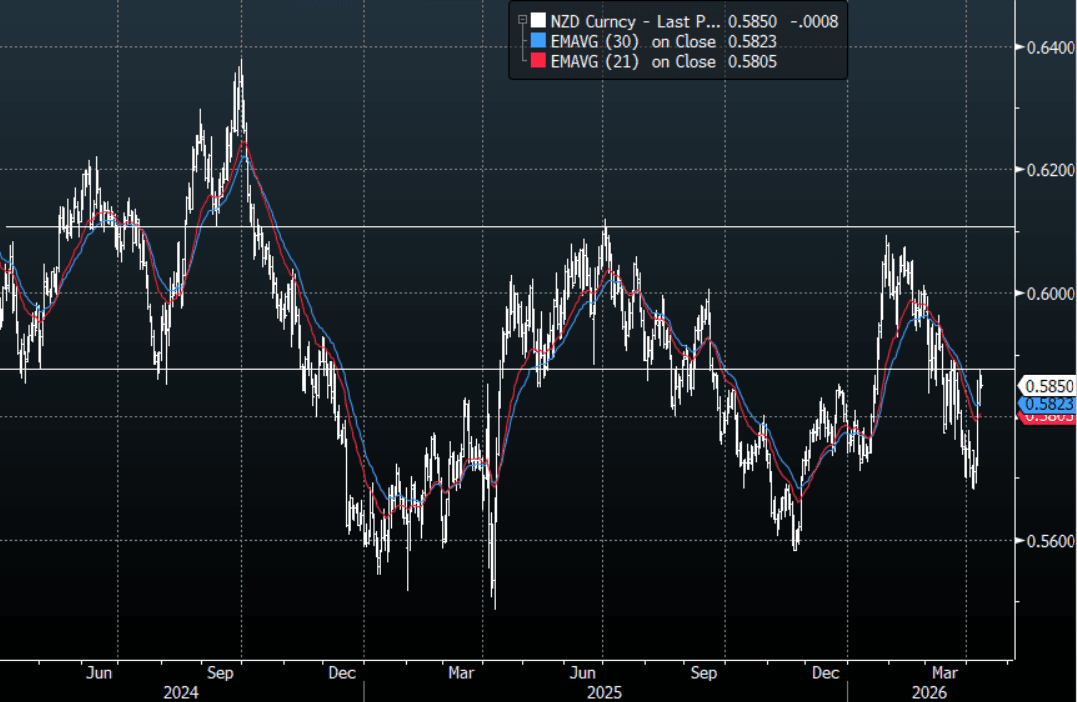

NZD/USD - Drifts Lower In A Quiet Asian Session Ahead Of Talks

The NZD/USD had a range today of 0.5845-0.5866 in the Asia-Pac session, it is currently trading around 0.5850, -0.15%. The NZD has drifted a little lower in a quiet Asian session. I suspect until we see what the weekend talks bring we could be sitting in limbo as this market could really go either way from here. On the day, the first support is back toward 0.5800-0.5830, the longs will be looking for this to hold for another test of the 0.5900 area, though I suspect a sustained break higher might be a lot to ask for with the event risk to come over the weekend. I suspect we trade 0.5750-0.5900 until we get clarity from the talks this weekend.

- Bloomberg - “RBNZ to Wait for Second-Quarter Data Before Rate Hike: Kiwibank. “The RBNZ is not going to make any moves until they have data in front of them. Q2 data, where the true impact of the oil crisis on the kiwi economy will really start to show, won’t be available until June/July.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5800(NZD503m). Upcoming Close Strikes : 0.5650(NZD310m April 15), 0.5725(NZD349m April 15), 0.5810(NZD605m April 14) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 58 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Ceasefire Led Gains Sees AI Stocks Dominance Continue

Major bourses across the region have delivered strong returns after a ceasefire induced bounceback mid week. AI / tech led indexes like the NIKKEI and KOSPI are leading the returns as their flagship names deliver very strong weekly gains. Korea's SK Hynix continues to stand out with gains of over 18%, Japan's Advantest +16% whilst Chinese AI stocks started to play catch up posting some solid gains. Tech is seen as less exposed to Middle East logistics than manufacturing and hence a place to invest.

The KOSPI gained over 500 points this week, seemingly bullet proof to global tensions; despite the countries reliance on oil imports. The KOSPI P/E is touching 20.85x at week's end against a full year estimate of 8.55x for 2026, and a dividend yield of just 1.12% (KTB 10-Yr 3.68%)

The Bank of Korea’s decision to hold rates at 2.50% on Thursday signaled that the regional inflation panic is being contained, encouraging a return to domestic banking stocks with Japanese banks performing strongly for the week, underpinned by moves lower in bond yields. If a permanent deal framework emerges, the Nikkei could consolidate above the 57,000 psychological resistance.

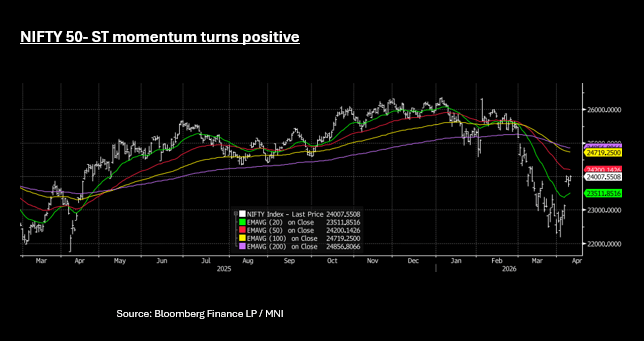

The NIFTY 50 is finishing the week strongly, surging Friday above 24,000 and is up now wedged between the 50-day EMA of 24,201 and the 20-day EMA of 23,514. Short term momentum indicators are turning more positive for the index suggesting further upside should the ceasefire hold.

Oil Range Bound; Eyes Turn to Negotiations

- A massive capitulation of the war premium occured when Trump announced the ceasefire earlier this week. After peaking early in the week due to fears of a total energy blockade, prices have stabilized significantly lower.

- Whilst WTI is up +0.36% today at US$98.22 bbl, for the week it remains down almost 12%, having hit the high of $117.63

- Brent has had moderate gains of +0.55% today to be at US$96.47 bbl but remains lower by -11.50%, after an high earlier in the week of $111.89.

- Doubts about the two-week truce are growing as both the US and Iran exchange accusations of violations. Israeli strikes in Lebanon are a primary flashpoint, with Tehran claiming Lebanon is covered under the agreement-a stance Washington disputes.

- The Strait of Hormuz remains effectively closed. Reports indicate Tehran still requires military approval for vessel passage, with a limited number of ships transiting with ongoing fear of naval mines and a potential re-closure by the IRGC in response to Lebanese strikes. Some reports suggest Iran is seeking to formalize a $2 million per ship transit fee for the Strait, which risks becoming a permanent structural cost for global oil.

- The Chinese government has given state refiners the green light to tap commercial reserves of oil due to a global energy crunch caused by a six-week war in the Middle East.

- High-stakes direct negotiations between the United States and Iran are scheduled to begin today in Islamabad, Pakistan.

- Gold is flat at US$4,764 Friday and holding onto around 2% gains for the week.

- For the week gold has traded in a $4,600 - $4,856 range and is on track for its third consecutive weekly gain, recovering from a volatile March that saw the sharpest monthly decline since 2013.

- The Strait of Hormuz closure and erratic ceasefire reports have caused sharp swings, though the overall weekly structure remains bullish as investors eye diplomatic talks in Islamabad.

- Strong support has formed around $4,650–$4,680, while $4,800 persists as a psychological and technical barrier for further upside. Bullion however is caught in tight ranges Friday, wedged between the 50-day EMA of $4,781 and the 20-day EMA at 4,729.

- The 20-day EMA and 50-day EMA have converged, signalling a period of consolidation and a potential volatility breakout. Because EMAs react faster to recent price changes than simple moving averages (SMAs), their convergence suggests that the short-term trend is losing its distinct direction and aligning with the medium-term trend

- A story on BBG shows the shifting reserves globally with gold now eclipsing adjusted USD reserves, supported by global central bank buying.

US: Viewpoint On Anthropic's Mythos Model

A follow-up on the earlier bullet, this time by EndGame Macro on X, giving his take on why Washington would be treating Anthropic's model like it is a market risk. https://x.com/onechancefreedm/status/2042419691772158013?s=20

- "What They Are Probably Trying To Do: In my opinion Bessent and Powell would be trying to do three things at once. First, warn the largest institutions that the offense and defense balance in cyber may be shifting faster than normal patch cycles can handle. Second, force immediate coordination across the firms that matter most to payments, clearing, custody, and market functioning. Third, send a quiet signal that this is now being treated as a national security and financial stability problem, not just a private sector technology issue. That is why a joint move from Treasury and the Fed would make sense. Treasury handles critical infrastructure coordination. The Fed worries about systemic transmission. Put together, that is not a panic meeting. It is what responsible officials would do if they believed the next systemic shock might begin with code instead of credit."

- "My Take: The dominant motive here is genuine defensive coordination. There may also be a secondary layer of regulatory signaling and political optics, because Washington rarely does only one thing at a time. But the core logic is still the same. In a stronger economy, this would be serious. In a slowing economy with hotter inflation expectations and geopolitical stress, it becomes urgent. The real message is not that officials suddenly became AI alarmists. It is that they seem to believe the next confidence shock to the financial system may not start with bad loans, leverage, or a bank run. It may start with an AI model that collapses the time between discovering a vulnerability and exploiting it."

GLOBAL POLITICAL RISK: Viewpoint on Peace Talks

Danny Citrinowicz a Middle-East national security and intelligence expert gave his views via a thread on X advising the President on how he thinks Iran views the upcoming talks.

- "I hope those advising the U.S. President are making the following points clear:"

- "Iran sees itself as having achieved a significant strategic gain. From its perspective, if its terms are not met, there will be no meeting in Islamabad, even at the cost of renewed escalation."

- "Iran is unlikely to reopen the straits without a full ceasefire, which it believes was promised, even under pressure or threats."

- "Tehran has no intention of offering new concessions beyond what has already been discussed with the U.S. It views itself as negotiating from a position of strength, so why concede more?"

- "The “Axis of Resistance” operates as an interconnected system. As long as fighting continues in Lebanon, Shiite militias in Iraq and potentially the Houthis, are likely to remain engaged."

- "Iran does not see itself as having been defeated. It did not seek these negotiations, and it is unrealistic to expect concessions at the table if, in its own assessment, it has not conceded on the battlefield."

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2026 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/04/2026 | 0600/0800 | *** | CPI Norway | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0800/1000 | * | Industrial Production | |

| 10/04/2026 | 1000/1200 | ECB de Guindos Remarks at Development Event | ||

| 10/04/2026 | - | *** | New Loans | |

| 10/04/2026 | - | *** | Money Supply | |

| 10/04/2026 | - | *** | Social Financing | |

| 10/04/2026 | 1200/0800 | ** | Brazil Final CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1800/1400 | ** | Treasury Budget |