ASIA STOCKS: Ceasefire Led Gains Sees AI Stocks Dominance Continue

Major bourses across the region have delivered strong returns after a ceasefire induced bounceback mid week. AI / tech led indexes like the NIKKEI and KOSPI are leading the returns as their flagship names deliver very strong weekly gains. Korea's SK Hynix continues to stand out with gains of over 18%, Japan's Advantest +16% whilst Chinese AI stocks started to play catch up posting some solid gains. Tech is seen as less exposed to Middle East logistics than manufacturing and hence a place to invest.

The KOSPI gained over 500 points this week, seemingly bullet proof to global tensions; despite the countries reliance on oil imports. The KOSPI P/E is touching 20.85x at week's end against a full year estimate of 8.55x for 2026, and a dividend yield of just 1.12% (KTB 10-Yr 3.68%)

The Bank of Korea’s decision to hold rates at 2.50% on Thursday signaled that the regional inflation panic is being contained, encouraging a return to domestic banking stocks with Japanese banks performing strongly for the week, underpinned by moves lower in bond yields. If a permanent deal framework emerges, the Nikkei could consolidate above the 57,000 psychological resistance.

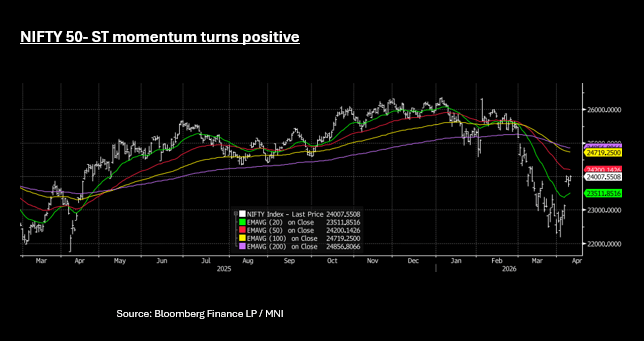

The NIFTY 50 is finishing the week strongly, surging Friday above 24,000 and is up now wedged between the 50-day EMA of 24,201 and the 20-day EMA of 23,514. Short term momentum indicators are turning more positive for the index suggesting further upside should the ceasefire hold.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: 10-Yr Auction Key Test as Yields Hover Near 4.15%

USTs held on to early gains Wednesday as declining oil prices suggest rampant inflation may be avoided. Yields were lower by 1-2bps early on and are looking set to finish that way as the Asia trading day nears end.

- The 2-Yr is down -1.8bps at 3.578%

- The 5-Yr is down -2.1bps at 3.722%

- The 10-Yr is down -1.6bps at 4.144%

- The 30-yr is down -1.1bps at 4.782%

The pattern in recent days has been modestly lower yields in the Asia trading day before moves higher again in the US trading day. This suggests profit taking from Asia based investors on overnight positioning as the driving force in the region. The weakness in the 3-Yr auction overnight raises short term concerns for UST yields as the trend appear for higher and the FEB CPI is likely to be looked past.

Whilst a very weak CPI print may bring forward rate cut expectations normally, in the current environment the February CPI is likely to be viewed as stale given expectations for sharp rise in inflation going forward on the back of oil's ascent.

The key test for Wednesday will be a US$39bn 10-Yr auction. Given the weakness in the overnight 3-Yr investors will watch for signs that demand is teetering further.

The last three 10-Yr auctions were February 2026: bid to cover 2.39; January 2026: bid to cover 2.55 and December 2025: bid to cover 2.51 - against a six-month average of 2.53x.

ASIA STOCKS: Asia Stocks Rebound as Oil Relief Eases Energy Shock Fears

Major Asian equity markets rallied today on cooling oil prices as reports of a historic IEA emergency reserve release eased fears of a global energy shock. The AI / tech heavy bourses led the way with the NIKKEI up +2.6%, KOSPI +3.5% and the TAIEX +4.3% following a positive lead in overnight after US firm Oracle posted better-than-expected results for its infrastructure business. Oracle Corp. shares gained almost 10% in extended trading after the company posted strong results and gave an outlook that suggested there is little letup in demand for AI computing. This saw Japan's Softbank rally over +9%, Korea's SK Hynix over +4% and Taiwan's TSMC over +5% today.

In Japan, those stocks hit hard due to the spike in oil prices performed Wednesday with Energy and Chemical companies up strongly.

China's bourses lagged regional losses as the oil price spiked on account of the Iran war and are lagging the rally again today. The Hang Seng is barely positive, despite the positive lead in for tech. Onshore media reports are now suggesting that following the significant jump in February exports, expectations for monetary policy are pushed out with May now likely.

Whilst SE Asian peers were quiet Wednesday, the SE Thai is up +1.2% with oil related stocks driving the gains. Markets had feared a rampant oil price would squeeze manufacturers in Thailand and the decline in prices help alleviate that immediate concern.

India remains volatility giving back most of yesterday's gains in the first part of the trading day as the Rupee opens weaker Wednesday.

JGBS: Little Changed As Market Takes Breather After Recent Volatility

JGB futures are stronger, +5 compared to settlement levels, after spending much of the session in the red.

- Japan's Feb PPI was weaker than forecast, falling 0.1%m/m (versus 0.2% forecast and 0.2% prior). In y/y terms we eased to 2.0%, against a 2.2% forecast and prior 2.3% outcome. The Feb print may be discounted to some extent, given the surge in energy prices since the end of Feb due to the Iran conflict.

- The spike in oil prices, if sustained, is likely to feed through into higher Japan imports in coming months. We observed the sharp rises seen in 2022, following the Russian invasion of Ukraine and the spill over to higher energy prices then.

- "JAPAN'S AKAZAWA: JAPAN CAN RELEASE OIL RESERVES ON ITS OWN, WILL TAKE NECESSARY MEASURES TO RESPOND TO OIL PRICES" – BBG

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's bear-steepener.

- Cash JGBs are little changed across benchmarks. The benchmark 2-year yield is 2bps richer after today’s solid auction.

- Swap rates are ~1bp higher.

- Tomorrow, the local calendar will see the results of the BSI Industry Survey, Weekly International Investment Flows and Tokyo Office vacancies.