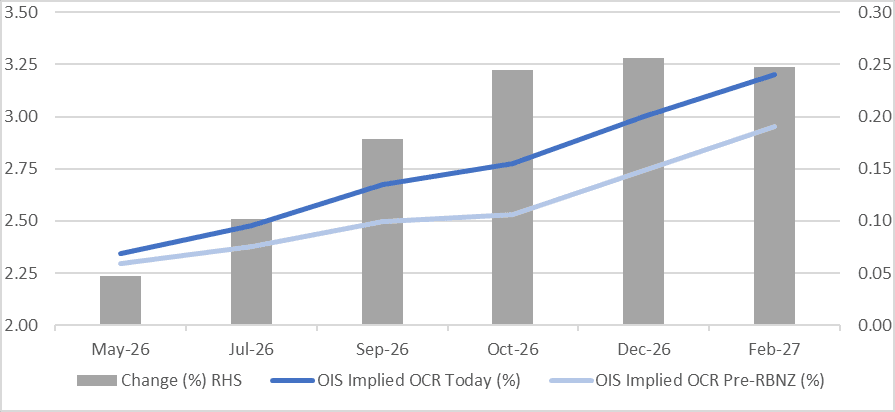

STIR: RBNZ-Dated OIS Pricing Little Changed But Firmer Than Pre-RBNZ

RBNZ-dated OIS pricing is little changed across meetings today, but remains 5-26bps firmer than Wednesday’s pre-RBNZ levels.

- In a unanimous decision, the RBNZ kept rates at 2.25% but warned that it is prepared to hike if inflation is not expected to return to the 2% band mid-point over the medium term. If core and wage inflation as well as inflation expectations aren’t contained “decisive and timely increases in the OCR would be required”.

- RBNZ Governor Anna Breman signalled expectations for somewhat weaker economic growth in New Zealand, with firms likely to act more cautiously in the near term. While the outlook has softened, she noted the Bank does not currently expect the economy to contract. The RBNZ remains focused on returning inflation to the 2% midpoint and is closely monitoring any signs that core inflation could rise.

- Pricing is now 4-21bps firmer than yesterday’s pre-RBNZ levels.

- 9bps of tightening is priced for May, while February 2027 assigns 95bps.

Figure 1: RBNZ Dated OIS Current vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Above Tuesday Highs, 0.7200 Next Focus Pt, As Local Banks See March Hike

AUD/USD is at 0.7160/75, just off session highs of 0.7175, which was through Tuesday session highs for the pair. This is fresh highs back to mid 2022. A close above 0.7200 and technically you would have to start considering another leg higher, CTA's and momentum funds will not be holding back. A growing number of local banks, NAB, ANZ and Westpac are now calling for a hike from the RBA next week. Close to 18bps worth of a hike next week is priced in. On Monday this stood at close to 6.5bps.

CHINA: Expected RRR Cut Delayed, CGB 10-Yr Higher

- Local press are suggesting that on the back of the very strong export numbers for February, any intended monetary policy changes in China may now be delayed until May.

- This has seen a modest move higher in yields with the CGB touching 1.82% - having reached 1.78% last week.

- Futures are off modestly with the 10-Yr down -.045 to 108.255

- The 2-YR is down -.01 to 102.456.

- During the 2026 National People's Congress, China's central bank governor Pan confirmed that the PBOC will maintain a "moderately loose" monetary policy throughout 2026. The primary goal is to provide a supportive financial environment for the start of the 15th Five-Year Plan while guiding prices toward a "reasonable recovery" to combat deflationary pressures.

- Expectations have shifted in recent days around policy changes. Leading into the NPC expectations were for an imminent RRR cut following the conclusion of the NPC.

- A delay could see the CGB 10-Yr re-establish itself in the 1.80-1.90% range again.

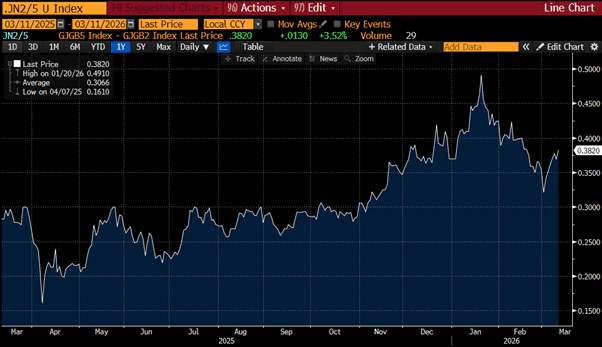

JGBS: Twist-Flattening Ahead Of 5Y Supply

At the Tokyo lunch break, JGB futures are weaker, -9compared to settlement levels.

- Japan's Feb PPI was weaker than forecast, falling 0.1%m/m (versus 0.2% forecast and 0.2% prior). In y/y terms we eased to 2.0%, against a 2.2% forecast and prior 2.3% outcome.

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday’s bear-steepener.

- Cash JGBs have twist-flattened across benchmarks, with yields 2bps higher to 1bp lower. The benchmark 5-year yield is 1.8bps higher at 1.642% ahead of today’s supply.

- The yield on today’s 5-year offering is similar to last month’s level and sits 10bps below its cycle high.

- The 2s/5s curve is slightly flatter than last month’s outing, 10-15bps below its cycle high (steepest since late 2009).

- From late last year, the steepening of the yield curve had been most pronounced in the 2/5 segment, with the 5-year sector seen as relatively unattractive. Rising market expectations for BOJ rate hikes had been placing upward pressure on the 5-year yield.

- Those expectations had moderated from late January until last week. However, with BOJ hike expectations higher again on the back of the recent oil price surge, the 2/5 curve has moved away its flattest level since November.

- Swap rates are ~2bps higher.

Source: Bloomberg Finance LP