AUSSIE BONDS: Grinds Cheaper Through The Session, US CPI Data Due

ACGBs (YM -4.0 & XM -4.5) are cheaper with US tsys.

- Cash US tsys are ~2bps in today’s Asia-Pac session after yesterday's modest bull-flattener.

- Friday US Data Calendar: CPI, UofM Sentiment, Durables/Cap Goods.

- "US, Iran Prepare for Talks With Lebanon Conflict Unresolved" - BBG

- Zerohedge on X: "If this ceasefire breaks and the US resumes its military campaign, that would be the beginning of a 'worst case scenario' where civilian infra is targeted..., WTI makes new highs and Equities make new lows. The feel of a binary outcome is likely to paralyze investors"- JPMorgan

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +66bps.

- The bills strip has bear-steepened, with pricing +1 to -3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 67% for May to 160% by August and 232% by December 2026.

- On Monday, the local calendar will be empty, ahead of Consumer and Business Confidence on Tuesday and March’s Employment Report on Thursday.

- Next week, the AOFM plans to sell A$1000mn of the 4.25% 21 October 2036 bond on Wednesday and A$1000mn of the 1.50% 21 June 2031 bond on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Asia Stocks Rebound as Oil Relief Eases Energy Shock Fears

Major Asian equity markets rallied today on cooling oil prices as reports of a historic IEA emergency reserve release eased fears of a global energy shock. The AI / tech heavy bourses led the way with the NIKKEI up +2.6%, KOSPI +3.5% and the TAIEX +4.3% following a positive lead in overnight after US firm Oracle posted better-than-expected results for its infrastructure business. Oracle Corp. shares gained almost 10% in extended trading after the company posted strong results and gave an outlook that suggested there is little letup in demand for AI computing. This saw Japan's Softbank rally over +9%, Korea's SK Hynix over +4% and Taiwan's TSMC over +5% today.

In Japan, those stocks hit hard due to the spike in oil prices performed Wednesday with Energy and Chemical companies up strongly.

China's bourses lagged regional losses as the oil price spiked on account of the Iran war and are lagging the rally again today. The Hang Seng is barely positive, despite the positive lead in for tech. Onshore media reports are now suggesting that following the significant jump in February exports, expectations for monetary policy are pushed out with May now likely.

Whilst SE Asian peers were quiet Wednesday, the SE Thai is up +1.2% with oil related stocks driving the gains. Markets had feared a rampant oil price would squeeze manufacturers in Thailand and the decline in prices help alleviate that immediate concern.

India remains volatility giving back most of yesterday's gains in the first part of the trading day as the Rupee opens weaker Wednesday.

JGBS: Little Changed As Market Takes Breather After Recent Volatility

JGB futures are stronger, +5 compared to settlement levels, after spending much of the session in the red.

- Japan's Feb PPI was weaker than forecast, falling 0.1%m/m (versus 0.2% forecast and 0.2% prior). In y/y terms we eased to 2.0%, against a 2.2% forecast and prior 2.3% outcome. The Feb print may be discounted to some extent, given the surge in energy prices since the end of Feb due to the Iran conflict.

- The spike in oil prices, if sustained, is likely to feed through into higher Japan imports in coming months. We observed the sharp rises seen in 2022, following the Russian invasion of Ukraine and the spill over to higher energy prices then.

- "JAPAN'S AKAZAWA: JAPAN CAN RELEASE OIL RESERVES ON ITS OWN, WILL TAKE NECESSARY MEASURES TO RESPOND TO OIL PRICES" – BBG

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's bear-steepener.

- Cash JGBs are little changed across benchmarks. The benchmark 2-year yield is 2bps richer after today’s solid auction.

- Swap rates are ~1bp higher.

- Tomorrow, the local calendar will see the results of the BSI Industry Survey, Weekly International Investment Flows and Tokyo Office vacancies.

FOREX: USD - BBDXY Drifts Back Below 1200, Destiny Tied To Oil For Now

The BBDXY has had a range today of 1198.12 - 1200.93 in the Asia-Pac session; it is currently trading around 1198, -0.15%. The BBDXY was rejected above the 1210 area and is now very quickly back to testing its support as the market pounces on any reason to sell USD’s again. The stock market continues to look at things through rose tinted glasses and is hoping a sale of global strategic reserves is able to cap Oil long enough for the conflict to end. I am not so optimistic but you can’t ignore the price action. On the day, I suspect the USD will remain under pressure initially as the market tries to be positive. I suspect though that we might see buyers fade this 1188-1195 area first up, so for now a messy 1187-1213 range will probably cover it as the world looks for more clarity around the conflict and its potential impact on supply lines.

- EUR/USD - Asian range 1.1603-1.1632, Asia is currently trading 1.1630. The pair stalled above 1.1650 overnight, but risk is on the front foot in Asia as the market reacts to the potential Global Oil Reserve release. The pivotal 1.1400-1.1500 area proved to be solid first up and I suspect the USD will remain under pressure in the short-term. Going forward does this really change much unless we get a quick cessation in Iran and the Straits open up again, none of which look imminent. On the day, the first sell-zone is back toward 1.1670-1.1700 and then the 1.1750-1.1800 area, looking for another test of the pivotal 1.1400-1.1500 support at some point.

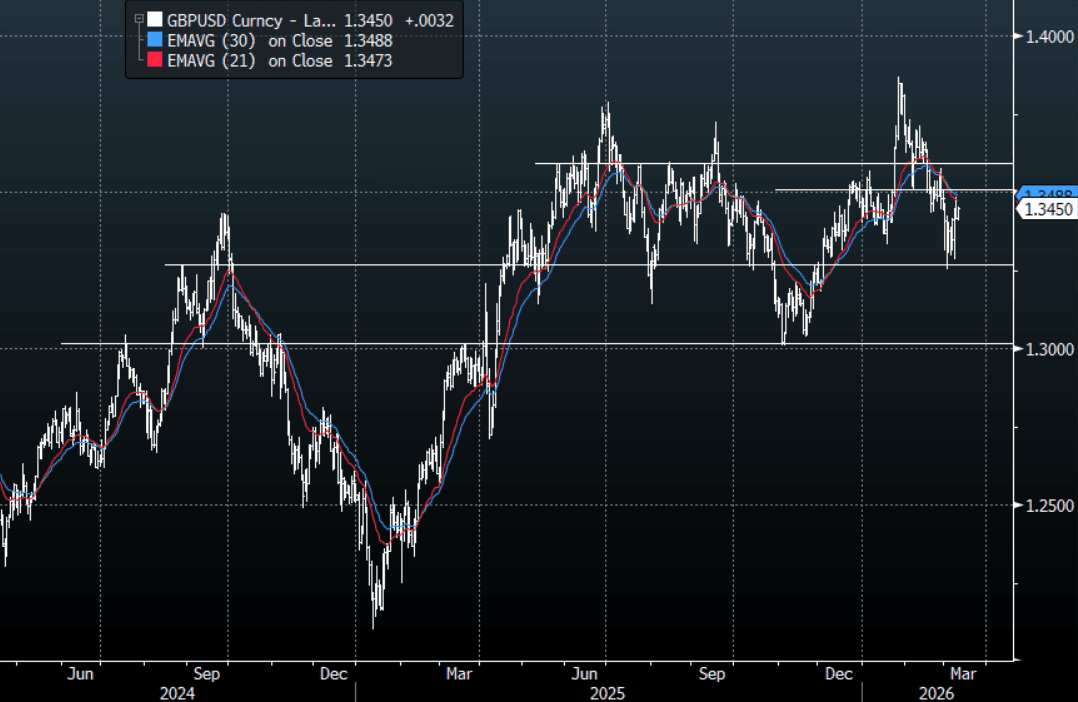

- GBP/USD - Asian range 1.3410-1.3453, Asia is currently dealing around 1.3450. GBP could not sustain a break below 1.3300 and is now bouncing as the move in oil dominates markets. On the day, look for resistance toward 1.3480-1.3520 and then the more important 1.3600 to be faded as the USD comes back under pressure. Sellers will be looking for the 1.3300 area to give way at some point.

- Germany Feb. (F) CPI, ECB’s Guindos speaks, BOE’s Breeden speaks, US Feb. CPI, Fed’s Bowman speaks, ECB’s Schnabel speaks, US Feb. Federal Budget Balance, OPEC monthly oil market report

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P