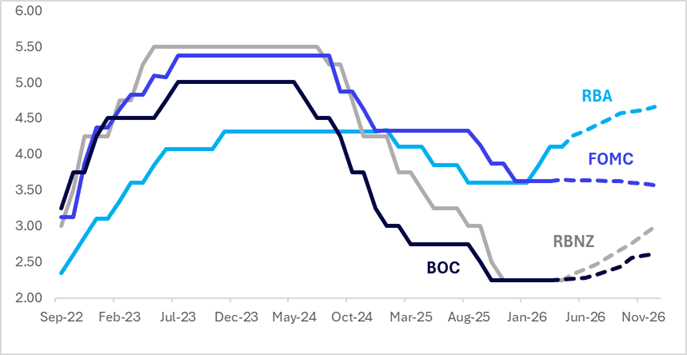

STIR: $-Bloc Year-End Pricing Mostly Softer Over Past Two Weeks

Interest-rate expectations across the $-bloc through December 2026 were mixed over the past two weeks, amidst ongoing uncertainty around the Middle East conflict and its implications for oil prices.

- Markets in the US and Canada softened by 22bps and 32bps, respectively, while Australia (-5bps) and New Zealand (+2bps) were relatively little changed.

- Nevertheless, relative to late February, December 2026 pricing remains 28-50bps firmer across the $-bloc, with the US leading and Australia lagging.

- In terms of recent events in the $-bloc, April 8th’s RBNZ policy meeting highlighted.

- In a unanimous decision, the RBNZ kept rates at 2.25% but warned that it is prepared to hike if inflation is not expected to return to the 2% band mid-point over the medium term. If core and wage inflation as well as inflation expectations aren’t contained “decisive and timely increases in the OCR would be required”.

- The MPC discussed whether to hike rates to pre-emptively act against rising inflation but the discussion was balanced looking at the risks to the already soft recovery from higher fuel prices.

- The next major regional policy events are the FOMC and BOC policy meetings on 29 April. Currently, the market attaches little chance of movement by either central bank.

- Looking ahead to December 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.57%, +6bps; Canada (BOC): 2.61%, +36bps; Australia (RBA): 4.41%, +31bps; and New Zealand (RBNZ): 2.99%, +74bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD: EUR/USD - Drifts Higher As Risk Rebounds Thanks To Oil

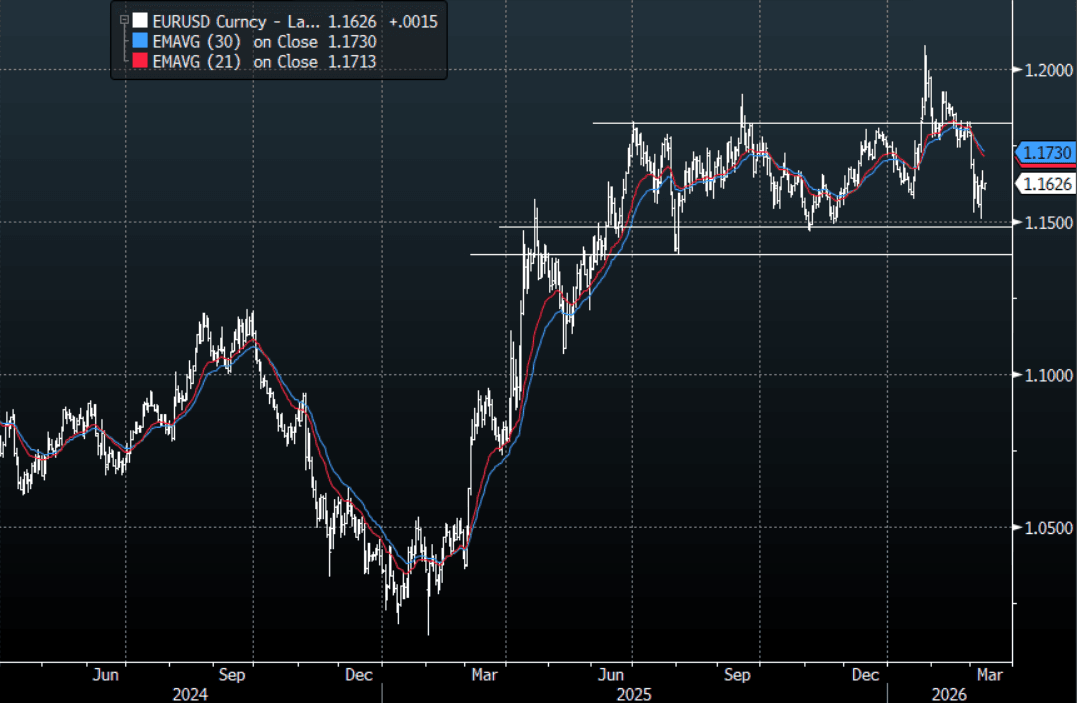

The EUR/USD range overnight was 1.1608-1.1667, Asia is currently trading around 1.1625. The pair stalled above 1.1650 overnight, but risk is on the frontfoot in Asia as the market reacts to the potential Global Oil Reserve release. The pivotal 1.1400-1.1500 area proved to be solid first up and I suspect the USD will remain under pressure in the short-term. Going forward does this really change much unless we get a quick cessation in Iran and the Straits open up again, none of which look imminent. On the day, the first sell-zone is back toward 1.1670-1.1700 and then the 1.1750-1.1800 area, looking for another test of the pivotal 1.1400-1.1500 support at some point. .

- “We’re concerned at the apparent lack of a joint plan on how this war can quickly be brought to a convincing conclusion,” German Chancellor Friedrich Merz told reporters.” - BBG

- Oguz Erkan on X: "Most countries in Europe have less than 100 days of oil stocks. If the war continues, Iran's goal is to keep the Hormuz under pressure as long as possible, since they know that European economies will start to crumble after two months as their oil stocks deplete. I think Trump will end the war before this happens."

- MNI - Italy Asked For EU Fiscal Escape Clause - Source. Italy and Slovenia asked for the activation of the General Escape Clause from the EU’s fiscal rules at Monday's meeting of euro area finance ministers.

- CFTC Data up to 03/03/26 shows the Leveraged community quickly building a short EUR exposure having just exited their previous very brief short long, -21992(Last -404). Shows conviction has been low on direction recently as positions chop quickly from long to short.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.1650(EU1.55b), 1.1675(EU781m), 1.1700(EU2.3b). Upcoming Close Strikes : 1.1670(EU1.8b Mar 13), 1.1700(EU2.3b March 13), 1.1800(EU1.67b March 12) - BBG

- The EUR/USD Average True Range for the last 10 Trading days: 76 Points

Fig 1 : EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBA: Westpac Now Forecasting +25Bps In March & May

Local bank Westpac is now penciling in +25bps moves at the March and May policy meetings, taking the peak cash rate to 4.35%, see below for their viewpoint. NAB is also forecasting the RBA to hike in March and May, while late yesterday BoFA penciled in a March hike, while earlier today UBS did the same. This follows some hawkish remarks from RBA Deputy Governor Hauser in a podcast late yesterday, while Governor Bullock also stressed recently the March meeting was live. As Westpac notes below, the key shift has been the surge in oil prices, along with the RBA view of limited spare capacity.

- Westpac: "The RBA is now expected to hike rates 25bp in both March and May; this is a change from our previous view of a single hike in May with further hikes as a risk only. The expected peak cash rate is now 4.35%. The effect of higher oil prices on headline inflation is large but temporary. The RBA Monetary Policy Board will nevertheless feel compelled to react, especially given the hit to confidence and financial markets has so far not been severe. Key information shifting our view is RBA communication revealing it has not changed its pessimistic view of growth in supply capacity following the national accounts, even though data revisions, consumption and unit labour costs paint a more benign picture."

CHINA PRESS: A-shares To Trend Upward Aimd Market Resilience

The A-share market will likely trend upward despite significant fluctuations in the oil and gas sector, supported by recovering investor sentiment and increased market resilience, according to an article published on Yicai.com by Qin Huanmei, a researcher at the Institute of Chinese Modernization at Shanghai University of Finance and Economics. Authorities should strengthen support for the listing of hard technology companies and enrich the index system of the Science and Technology Innovation Board. It is also necessary to improve the information disclosure system, enhance regulatory transparency, refine the stock pricing mechanism and promote mergers and acquisitions to strengthen market resilience, the article said.