OIL: Oil Range Bound; Eyes Turn to Negotiations

- A massive capitulation of the war premium occured when Trump announced the ceasefire earlier this week. After peaking early in the week due to fears of a total energy blockade, prices have stabilized significantly lower.

- Whilst WTI is up +0.36% today at US$98.22 bbl, for the week it remains down almost 12%, having hit the high of $117.63

- Brent has had moderate gains of +0.55% today to be at US$96.47 bbl but remains lower by -11.50%, after an high earlier in the week of $111.89.

- Doubts about the two-week truce are growing as both the US and Iran exchange accusations of violations. Israeli strikes in Lebanon are a primary flashpoint, with Tehran claiming Lebanon is covered under the agreement-a stance Washington disputes.

- The Strait of Hormuz remains effectively closed. Reports indicate Tehran still requires military approval for vessel passage, with a limited number of ships transiting with ongoing fear of naval mines and a potential re-closure by the IRGC in response to Lebanese strikes. Some reports suggest Iran is seeking to formalize a $2 million per ship transit fee for the Strait, which risks becoming a permanent structural cost for global oil.

- The Chinese government has given state refiners the green light to tap commercial reserves of oil due to a global energy crunch caused by a six-week war in the Middle East.

- High-stakes direct negotiations between the United States and Iran are scheduled to begin today in Islamabad, Pakistan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Little Changed As Market Takes Breather After Recent Volatility

JGB futures are stronger, +5 compared to settlement levels, after spending much of the session in the red.

- Japan's Feb PPI was weaker than forecast, falling 0.1%m/m (versus 0.2% forecast and 0.2% prior). In y/y terms we eased to 2.0%, against a 2.2% forecast and prior 2.3% outcome. The Feb print may be discounted to some extent, given the surge in energy prices since the end of Feb due to the Iran conflict.

- The spike in oil prices, if sustained, is likely to feed through into higher Japan imports in coming months. We observed the sharp rises seen in 2022, following the Russian invasion of Ukraine and the spill over to higher energy prices then.

- "JAPAN'S AKAZAWA: JAPAN CAN RELEASE OIL RESERVES ON ITS OWN, WILL TAKE NECESSARY MEASURES TO RESPOND TO OIL PRICES" – BBG

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's bear-steepener.

- Cash JGBs are little changed across benchmarks. The benchmark 2-year yield is 2bps richer after today’s solid auction.

- Swap rates are ~1bp higher.

- Tomorrow, the local calendar will see the results of the BSI Industry Survey, Weekly International Investment Flows and Tokyo Office vacancies.

FOREX: USD - BBDXY Drifts Back Below 1200, Destiny Tied To Oil For Now

The BBDXY has had a range today of 1198.12 - 1200.93 in the Asia-Pac session; it is currently trading around 1198, -0.15%. The BBDXY was rejected above the 1210 area and is now very quickly back to testing its support as the market pounces on any reason to sell USD’s again. The stock market continues to look at things through rose tinted glasses and is hoping a sale of global strategic reserves is able to cap Oil long enough for the conflict to end. I am not so optimistic but you can’t ignore the price action. On the day, I suspect the USD will remain under pressure initially as the market tries to be positive. I suspect though that we might see buyers fade this 1188-1195 area first up, so for now a messy 1187-1213 range will probably cover it as the world looks for more clarity around the conflict and its potential impact on supply lines.

- EUR/USD - Asian range 1.1603-1.1632, Asia is currently trading 1.1630. The pair stalled above 1.1650 overnight, but risk is on the front foot in Asia as the market reacts to the potential Global Oil Reserve release. The pivotal 1.1400-1.1500 area proved to be solid first up and I suspect the USD will remain under pressure in the short-term. Going forward does this really change much unless we get a quick cessation in Iran and the Straits open up again, none of which look imminent. On the day, the first sell-zone is back toward 1.1670-1.1700 and then the 1.1750-1.1800 area, looking for another test of the pivotal 1.1400-1.1500 support at some point.

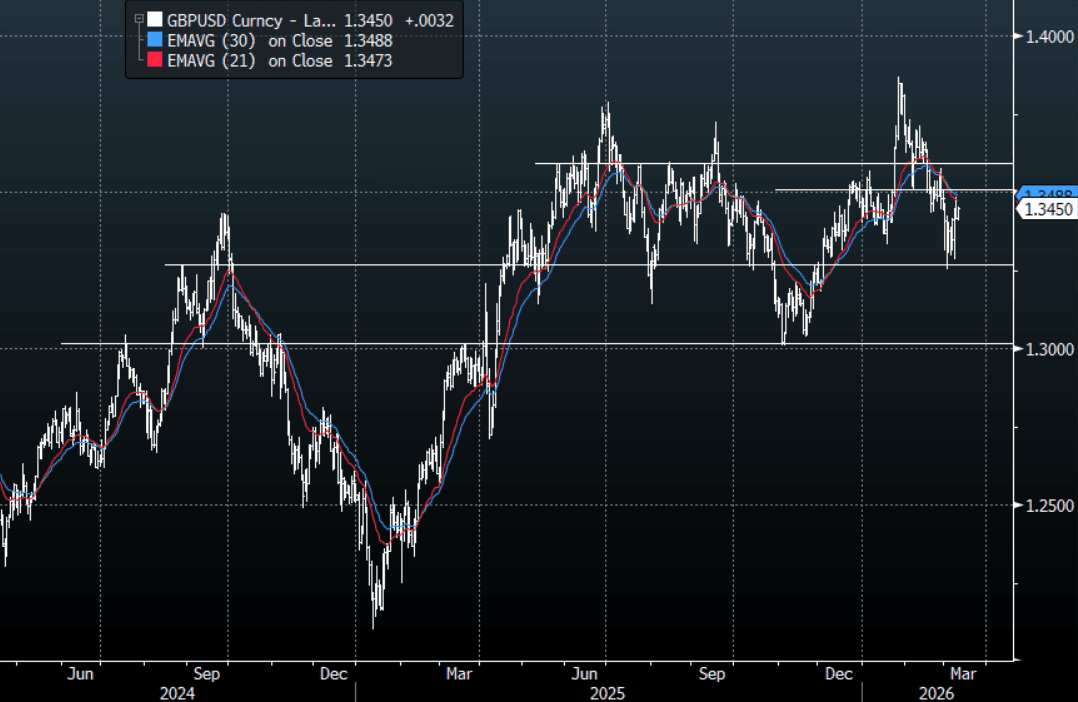

- GBP/USD - Asian range 1.3410-1.3453, Asia is currently dealing around 1.3450. GBP could not sustain a break below 1.3300 and is now bouncing as the move in oil dominates markets. On the day, look for resistance toward 1.3480-1.3520 and then the more important 1.3600 to be faded as the USD comes back under pressure. Sellers will be looking for the 1.3300 area to give way at some point.

- Germany Feb. (F) CPI, ECB’s Guindos speaks, BOE’s Breeden speaks, US Feb. CPI, Fed’s Bowman speaks, ECB’s Schnabel speaks, US Feb. Federal Budget Balance, OPEC monthly oil market report

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Subdued Session Despite Lifting Chances Of A March Hike

ACGBs (YM +1.0 & XM -0.5) are little changed after a relatively subdued data-light session. The market’s attention continues to focus on the US/Iran conflict and its resultant impact on the price of oil.

- The WSJ reported that the IEA has proposed the largest release of oil reserves in its history to bring down crude prices that have soared during the U.S.-Israel war with Iran.

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's bear-steepener.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +71bps.

- Ahead of next Tuesday’s RBA meeting, Deputy Governor Hauser said yesterday further inflationary pressure from the war in Iran would be unhelpful. Hauser stated that inflation is headed "higher than the projection we published in February" and that it's "so important actually that we do take the steps needed to bring inflation back to target from its too high level at the moment".”

- The bills strip has twist-flattened, with pricing -7 to +4 across contracts.

- RBA-dated OIS pricing has firmed sharply, with the probability of a 25bp hike rising from 69% for March to 155% by June and 244% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectations.

Bloomberg Finance LP