GLOBAL POLITICAL RISK: Viewpoint on Peace Talks

Danny Citrinowicz a Middle-East national security and intelligence expert gave his views via a thread on X advising the President on how he thinks Iran views the upcoming talks.

- "I hope those advising the U.S. President are making the following points clear:"

- "Iran sees itself as having achieved a significant strategic gain. From its perspective, if its terms are not met, there will be no meeting in Islamabad, even at the cost of renewed escalation."

- "Iran is unlikely to reopen the straits without a full ceasefire, which it believes was promised, even under pressure or threats."

- "Tehran has no intention of offering new concessions beyond what has already been discussed with the U.S. It views itself as negotiating from a position of strength, so why concede more?"

- "The “Axis of Resistance” operates as an interconnected system. As long as fighting continues in Lebanon, Shiite militias in Iraq and potentially the Houthis, are likely to remain engaged."

- "Iran does not see itself as having been defeated. It did not seek these negotiations, and it is unrealistic to expect concessions at the table if, in its own assessment, it has not conceded on the battlefield."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: US Yields to Look Through CPI as Inflation Pressures Build

US yields are lower in Asia today by 1-2bps with the short end out performing as the 2s10s curve steepens +1bps. Equity markets are responding positively to news of a potential strategic oil reserve release from the IEA with oil prices down moderately and equities strong.

The 10-yr has oscillated around the 4.15% yield level with momentum indicators suggesting it could test 4.20% in the next few sessions.

- The 2-Yr is down -1.6bps at 3.58%

- The 5-Yr is down -1.9bps at 3.724%

- The 10-Yr is down -1.6bps at 4.144%

- The 30-yr is down -1.1bps at 4.782%

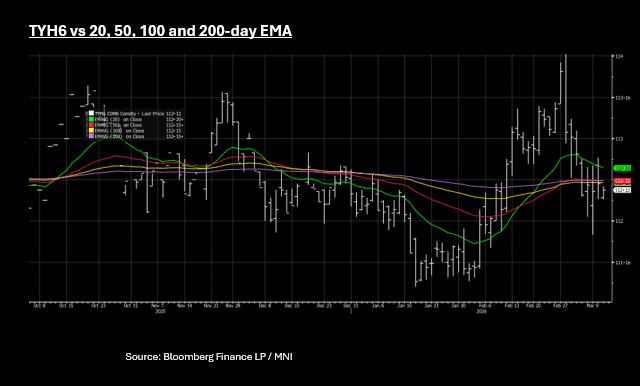

US bond futures are down moderately also with the 10-Yr down -02+ to 112-12. The move lower sees TYH6 move south of the 100-day EMA of 112-15+ which it had drawn near to though volumes today have been very low. 50, 100 and 200-day EMAs have converged which suggests pressure is building for a breakout.

The next focus for US rates will be the Feb CPI out later. Whilst a very weak CPI print may bring forward rate cut expectations normally, in the current environment the February CPI is likely to be viewed as stale given expectations for sharp rise in inflation going forward on the back of oil's ascent.

The pattern in recent days has been modestly lower yields in the Asia trading day before moves higher again in the US trading day. This suggests profit taking from Asia based investors on overnight positioning as the driving force in the region.

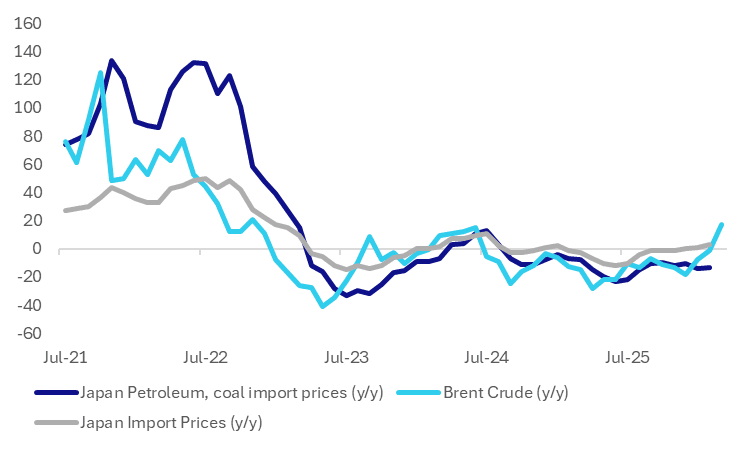

JAPAN DATA: Import Price Pressures May Build Given Oil Spike, Weaker Yen

The spike in oil prices, if sustained, is likely to feed through into higher Japan imports in coming months. The first chart below overlays Brent crude y/y changes (which are extended to end March based off current spot prices), against petroleum, coal import prices y/y, along with aggregate import prices y/y. We can observe the sharp rises seen in 2022, following the Russian invasion of Ukraine and spill over to higher energy prices then.

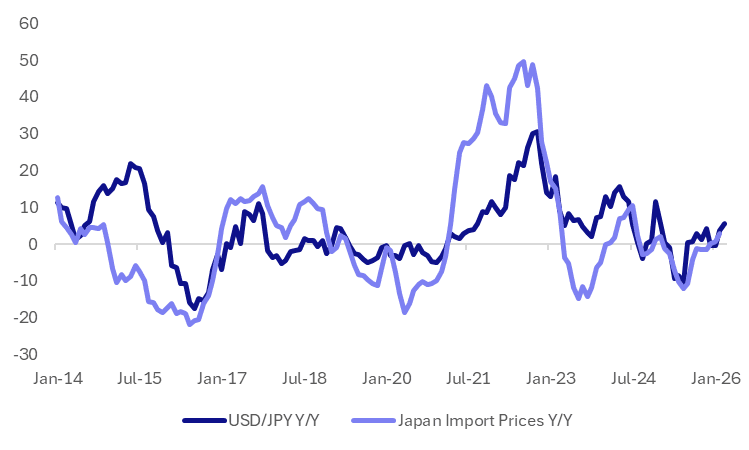

- At this stage, there is also no offset from the yen, with USD/JPY remaining elevated and rising in y/y terms. Without a sharp turn around in yen, y/y changes in USD/JPY are likely to remain positive in the first half of the year. The second chart below plots USD/JPY y/y changes against import prices y/y.

- This could in turn feed into stronger CPI pressures and impact the market outlook from a BoJ standpoint. For next week's meeting little is priced in terms of tightening risks, with a full hike not priced until the July meeting.

- The caveat is the government response to higher oil prices, while our policy team noted recently: The Bank of Japan is weighing upside risks to prices from higher crude oil costs against downside risks to growth from a deterioration in the terms of trade, a dynamic likely to reinforce caution and keep the 0.75% policy rate unchanged at the March meeting, while potentially delaying further normalisation, MNI understands.

Fig 1: Brent Crude Spike To Drive Higher Import Costs

Source: Bloomberg Finance L.P./MNI

Fig 2: USD/JPY Y/Y and Japan Import Prices Y/Y

Source: Bloomberg Finance L.P./MNI

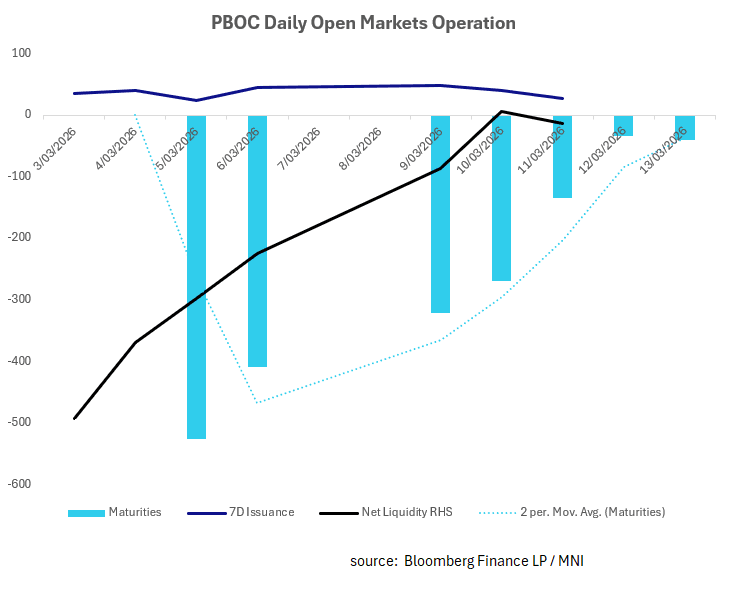

CHINA: Central Bank Withdraws CNY14bn via OMO

During the 2026 National People’s Congress, China’s central bank governor Pan confirmed that the PBOC will maintain a "moderately loose" monetary policy throughout 2026. The primary goal is to provide a supportive financial environment for the start of the 15th Five-Year Plan while guiding prices toward a "reasonable recovery" to combat deflationary pressures.

Expectations have shifted in recent days around policy changes. Leading into the NPC expectations were for an imminent RRR cut following the conclusion of the NPC.

Following the exceptionally strong February export data, these expectations have been pushed out now to May.

- The PBOC issued CNY26.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY40.5bn of 7-day reverse repo

- Net liquidity withdrawal CNY14bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.45%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.37%, from the prior close of 1.31%.

- The China 7-day interbank repo rate is at 1.45%, from the prior close of 1.43%.