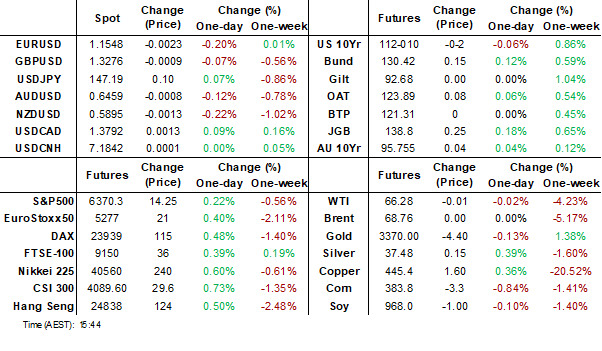

MNI EUROPEAN MARKETS ANALYSIS: Strong Day For Equities

- Major bourses enjoyed a strong day as markets look through US data and increased rate cut pricing.

- Japan turning positive on the trade deal with the US.

- China's inflationary decline is forecast to continue.

- Bond yields move lower across the region following US moves.

- Day ahead sees French Industrial Production and Regional PMIs.

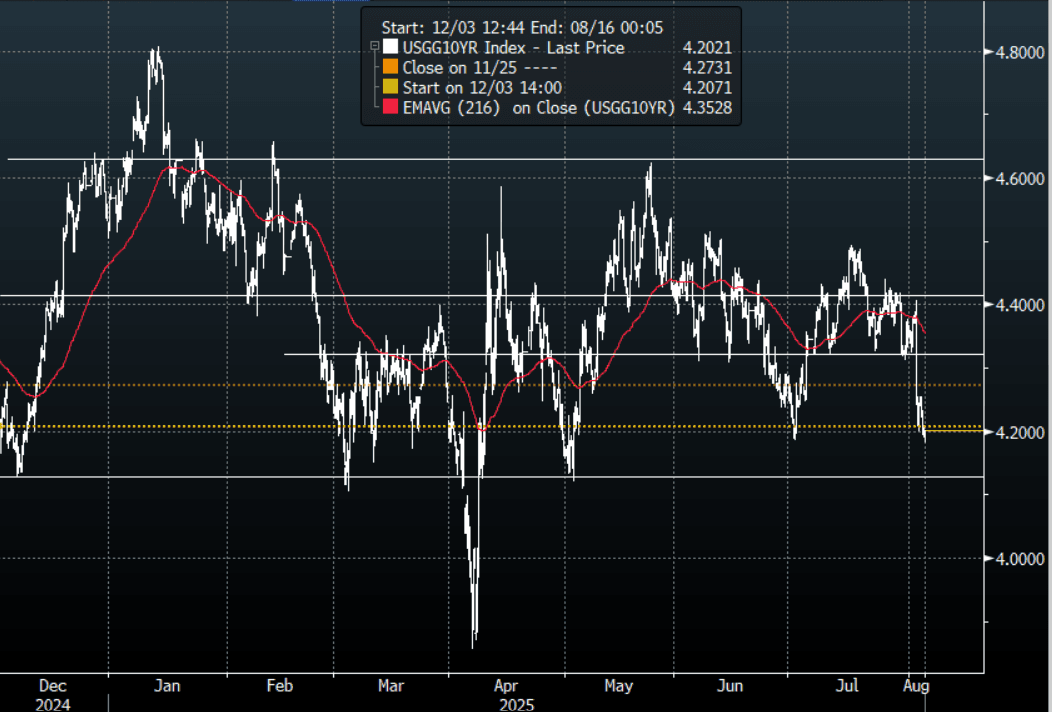

US TSYS: Asia Wrap - Yields End A Little Higher, Led By The Front-End

The TYU5 range has been 112-10 to 112-15+ during the Asia-Pacific session. It last changed hands at 112-11, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading around 3.696%, up 0.02 from its close.

- The US 10-year yield has moved higher trading around 4.20%, up 0.01 from its close.

- US TSY FLOWS BLOCK: 4000 of FVU5 traded at 109-03+. The contract is currently trading at 109-03, -0-01+ from closing levels.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Bloomberg - “The Fed may need more than two rate cuts this year, Mary Daly told Reuters. “I was willing to wait another cycle, but I can’t wait forever,” she said.”

- “The rally in US government debt was muted, as investors braced for heavy supply this week of $125 billion in new three-, 10- and 30-year bonds. ” - BBG

- David Rosenberg on X: “The virtual stalling-out in payroll growth in the past three months has been a recession predictor with 100% accuracy over the past six decades. Score a win for Bowman and Waller, whose crystal balls are clearer than the rest of the FOMC pack.”

- Data/Events: Trade Balance, S&P Global PMI’s, ISM Services

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Richer Despite Poor 10Y Auction

JGB futures are holding stronger, +26 compared to settlement levels, despite today’s poor 10-year auction.

- (MNI) A few Bank of Japan board members said they would consider resuming interest rate hikes if trade tensions were expected to ease without further escalation, according to minutes of the June 16-17 meeting released on Tuesday. However, the minutes offered no indication on the timing or pace of future rate increases.

- Bloomberg - "MUFG CEO Hironori Kamezawa called on the BOJ to raise its policy rate as early as the next meeting to combat strong inflation."

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally.

- Cash JGBs are 1-4bps richer across benchmarks, led by the 10-year. The benchmark 10-year yield is 4.1bps lower at 1.475% after today's supply.

- The 10-year JGB auction delivered weak results, with the low price failing to meet expectations at 100.21, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.0592x from 3.5070x, and the tail lengthened to 0.14 from 0.03.

- Swap rates are flat to slightly lower. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Cash Earnings data.

AUSSIE BONDS: Richer But Off Bests, Mar-36 Supply Tomorrow

ACGBs (YM flat & XM +4.0) are holding richer but well off session bests.

- June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today's US calendar will be the US ISM services index for July.

- Cash ACGBs are 11bps richer after being closed for a bank holiday yesterday, with the AU-US 10-year yield differential at +1bp.

- The bills strip is richer, with pricing flat to +1.

- RBA-dated OIS pricing is giving a 25bp rate cut in August a 100% probability, with a cumulative 65bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$900mn of the 4.25% 21 March 2036 bond. A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.

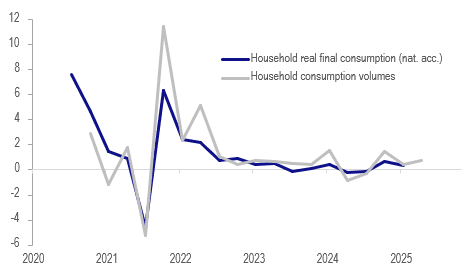

AUSTRALIA DATA: Q2 Spending Volumes Suggest Slight Pickup In Consumption Growth

June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

Australia real household consumption q/q%

- Q2 real spending saw strength from recreation (+1.8% q/q), hotels & restaurants (+1.6%), transport (+1.5%), household goods (+1.5%), health (+1.0%) and food (+1.0%), while alcohol and tobacco fell for the 14th straight quarter and clothing & footwear was down 2.0% q/q.

- The 1.3% m/m increase in goods consumption was in line with ABS comments that retail sales were boosted in June by discounting. On the other hand, services expenditure fell 0.5% m/m but is still up 6.6% y/y outperforming goods growth at 3.4% y/y.

- Both discretionary and non-discretionary spending rose 0.5% m/m to be up 4.3% y/y and 5.8% respectively. Stronger consumer confidence is likely needed for discretionary growth to catch up.

- From the July release only household spending data will be published as retail sales has now been discontinued.

Australia household consumption y/y% (monthly)

BONDS: NZGBS: Richer & At Session Bests, Q2 Employment Data Tomorrow

NZGBs closed at session bests, 4-5bps richer.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today’s US calendar will be the US ISM services index for July.

- ANZ commodity export prices fell 1.8% m/m in July versus a revised -2.4% in June.

- Tomorrow, the local calendar will see Q2 labour market data. It is expected to show that it weakened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ's 5.2% May projection. If the data print is as weak as or weaker than the Bloomberg consensus, then a rate cut on August 20 is likely.

- RBNZ dated OIS pricing closed showing 23bps of easing is priced for August, with a cumulative 42bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

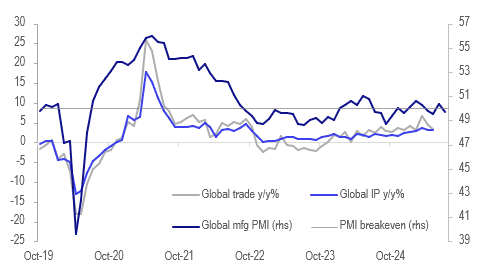

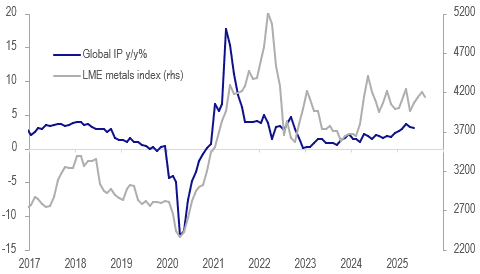

GLOBAL MACRO: Global PMI Suggests Weaker IP Growth In Q3

The JP Morgan global manufacturing PMI has been oscillating around the breakeven-50 mark since November as uncertainty remained high. In July it dipped below 50 at 49.7 after June’s 50.4. Recently it has been consistent with low but steady IP growth of 1.5-3%. The PMI is suggesting that after this event, industrial production growth is likely to slow back to within that range.

Global growth %

- CPB Global IP rose 0.3% m/m in May, the fourth consecutive increase, to hold annual growth at 3.1% y/y. It peaked in March at 3.6% y/y in line with the high in global export growth as shipments were frontloaded ahead of initial US tariff deadlines.

- The dip in the July manufacturing PMI was driven by output, orders and future output. The decline in orders was due to the exports contracting at a sharper rate with the index at 48.2 after 49.2, but still above both April and May.

- Growth in future output is still expect to be positive just less so than in June at 58.9 after 60.2 but is still above 2025’s low of 57.1 in April.

- Production was down in July in consumer, intermediate and capex goods sectors.

- Employment contracted at a slightly stronger rate in July but was close to unchanged with the PMI at 49.4 in July down from 49.7, but the 12th consecutive cut in staffing.

- Both input and output inflation in the PMI were little changed.

- Emerging Asia continued to outperform with India’s PMI showing the fastest growth followed by Vietnam and Thailand, according to JP Morgan/S&P Global. At the other end, Taiwan saw the worst contraction.

- Metal and wool prices as well as the Baltic Freight Index signal that global IP growth should remain close to recent rates around mid-year even if it does moderate after frontloading of exports.

Global IP y/y% vs LME metal prices

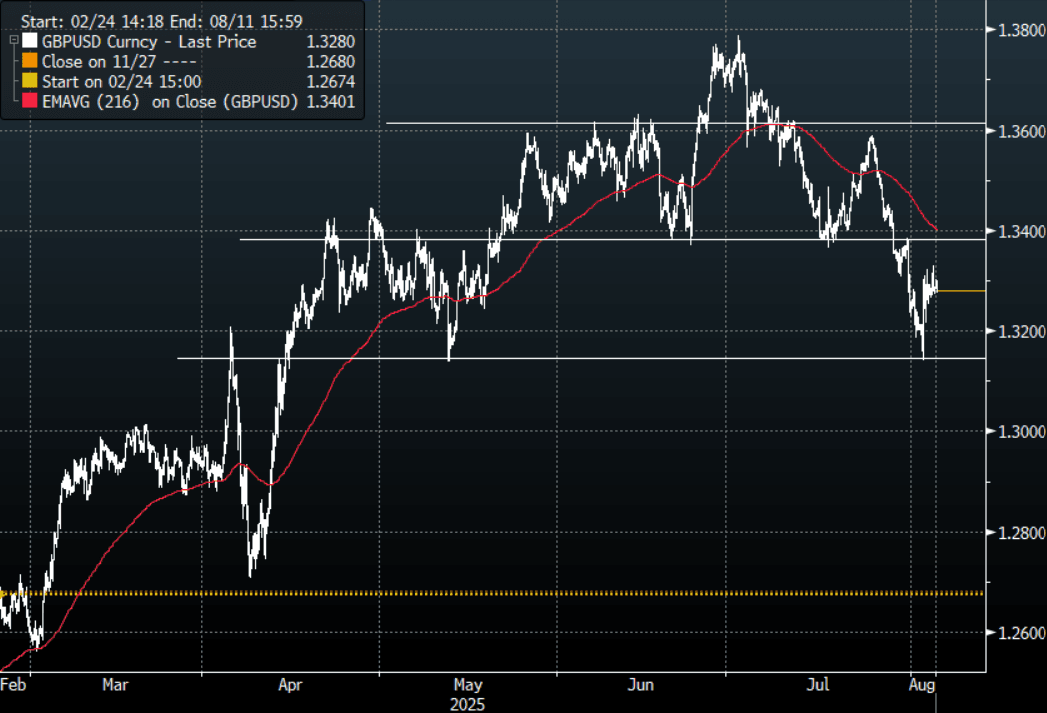

FOREX: Asia FX Wrap - BBDXY Finds Demand Sub 1210

The BBDXY has had a range of 1208.49 - 1211.50 in the Asia-Pac session, it is currently trading around 1211, +0.04%. The USD, with a huge rejection of the 1220/1230 area on Friday, had a knee-jerk reaction lower to the outsized move in US rates as the market's view on growth and interest rate cuts is re-evaluated. The USD is consolidating just above its 1205 support, with very little reaction to either rates extending lower or Equities bouncing strongly.

- EUR/USD - Asian range 1.1554 - 1.1588, Asia is currently trading 1.1560. The pair has bounced nicely off the important 1.1300/1.1400 area. The market is consolidating just ahead of its first resistance towards 1.1650/1.1700.

- GBP/USD - Asian range 1.3278 - 1.3303, Asia is currently dealing around 1.3280. This pair bounced nicely off the 1.3100/1.3200 support area. I would suspect sellers would be around on a bounce back towards 1.3400 initially.

- USD/CNH - Asian range 7.1774 - 7.1843, the USD/CNY fix printed 7.1366, Asia is currently dealing around 7.1830. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3372, US 10-Year 4.20%, BBDXY 1211, Crude Oil $66.16

- Data/Events : France Industrial/Manufacturing Production/HCOB PMI’s, Spain Homes Sales/Industrial Production/HCOM PMI’s, Italy HCOM PMI’s, Germany HCOB PMI’s, EZ HCOM PMI’s/PPI

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

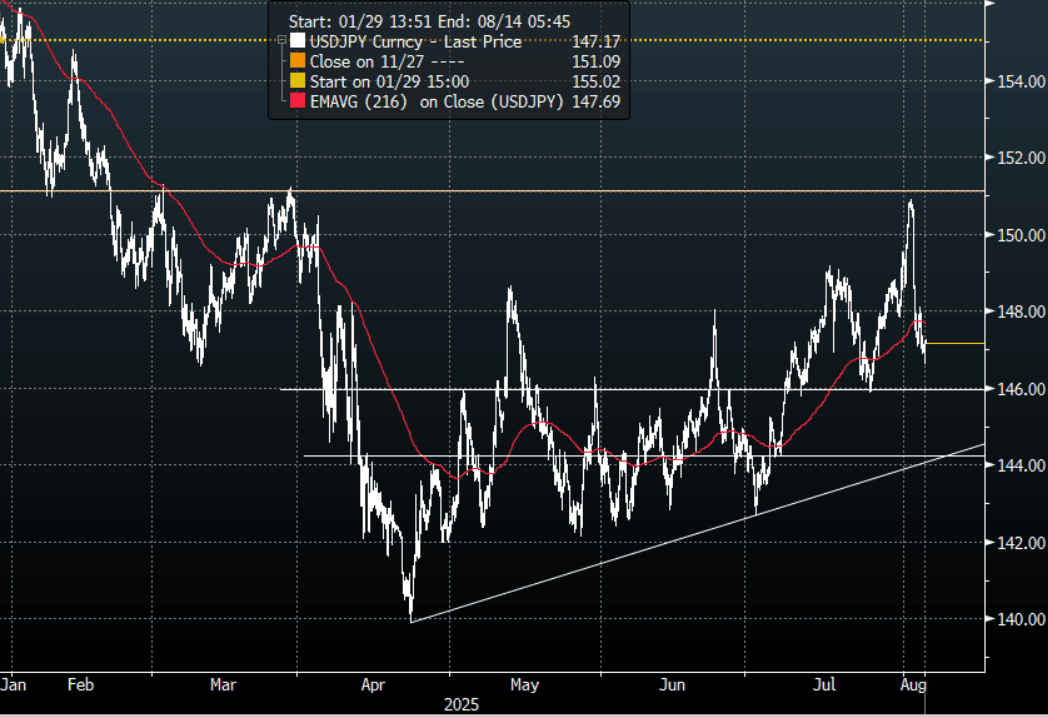

JPY: USD/JPY - Finds Some Demand Sub 147.00

The Asia-Pac USD/JPY range has been 146.62 - 147.26, Asia is currently trading around 147.20, +0.05%. USD/JPY was capped by decent supply around 148.00 overnight and traded heavy into our open ignoring the big bounce in US Equities. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional JPY longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. Price is tested the first support area around 146.50/147.00 where it found good demand this morning, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- "AKAZAWA: WILL MULL COLLABORATION WITH US ON PHARMA SUPPLY, WILL WORK CLOSELY WITH US ON CHIP MANUFACTURING. CHIP, PHARMA ARE IMPORTANT FOR ECONOMIC SECURITY. WILL ALSO AIM TO BOOST INWARD DIRECT INVESTMENT" - BBG - BBG

- "ISHIBA: BELIEVE TRADE DEAL DAMAGE TO AUTO INDUSTRY MINIMAL, DEAL IS WIN-WIN BASED ON JAPAN'S TECH, US LABOR AND MKT. LIMITING IMPACT OF TRADE DEAL ON JAPAN FARMERS CRITICAL, TRADE DEAL DOESN'T AFFECT JAPAN'S RICE FARMERS" - BBG

- Bloomberg - “MUFG CEO Hironori Kamezawa called on the BOJ to raise its policy rate as early as the next meeting to combat strong inflation.”

- “Japan is set to shift its policy on rice to focus on boosting production, moving away from adjusting output to maintain price stability, Nikkei reported.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($1.13b).Upcoming Close Strikes : 147.00($1.31b Aug 6), 148.50($1.24b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

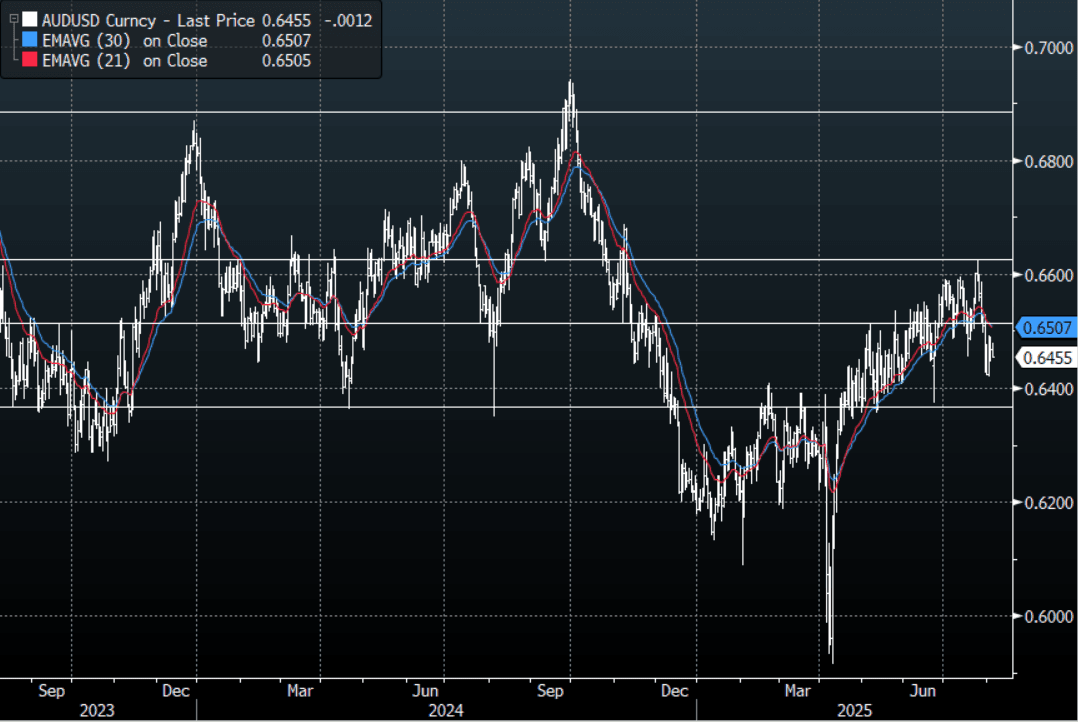

AUD/USD - Drifts Lower, Even With Risk Trading Well

The AUD/USD has had a range of 0.6454 - 0.6480 in the Asia- Pac session, it is currently trading around 0.6455, -0.17%. The AUD has traded heavy for most of our session even with risk trading positively. The AUD bounced nicely off the 0.6400 area but I suspect sellers might return back towards 0.6500/50 initially, though the bounce in equities overnight might suggest the correction I was looking for might not be as imminent as first thought.

- AUSTRALIA DATA: Q2 Spending Volumes Suggest Slight Pickup In Consumption Growth. June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

- "The ANZ-Roy Morgan Australian consumer confidence rose 3.9 points to 90.6 points in the week of July 28 to Aug. 3, its highest since May 2022, driven by an increase across all the subindices, ANZ reported Tuesday." - MTN

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD831m), 0.6600(AUD847m). Upcoming Close Strikes : 0.6500(AUD4.16b Aug 8), 0.6600(AUD1.97b Aug 7), 0.6800(AUD1.72b Aug 7) - BBG

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 94.95 - 95.29, Asia is trading around 95.00. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support toward the 95.00 area. Like the rest of the crosses the price action stands out in that it has not benefited at all from the strong bounce in risk overnight. There should be sellers around the 96.00/96.50 area initially.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

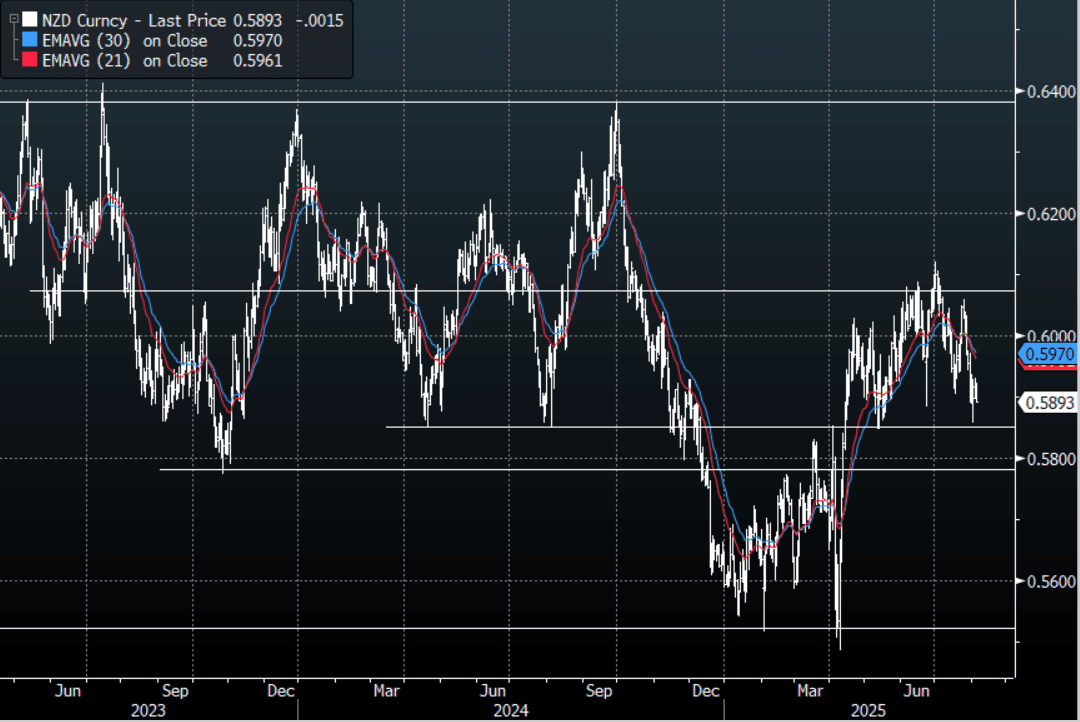

NZD/USD - Trades Heavy Even With Risk Extending Higher

The NZD/USD had a range of 0.5891 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5895, -0.25%. US Yields slipped lower again overnight, but stocks came roaring back and the USD went nowhere. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000, it looks like we might consolidate within the 0.5850-0.6100 range while we wait for clearer direction. It has traded heavy in our session after initially trying higher, ignoring the move higher in risk.

- (Bloomberg) -- New Zealand's commodity export prices fell 1.8% m/m in July versus revised -2.4% in June, according to ANZ Bank.

- CHINA PMI Services Records Large Gains: China's S&P Global China PMI (formerly CAIXIN) came in ahead of expectations in July. Up at 52.6, it was a material increase from June's result of +50.6 and estimates of +50.4. The result was the best since May 2024 with the employment index up to +50.9, from June's contraction.

- “The US is exploring ways to equip AI chips with location tracking to curtail exports to China and other restricted countries.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD315m). Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.6140(NZD364m Aug 7). - BBG

- AUD/NZD range for the session has been 1.0938 - 1.0960, currently trading 1.0955. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Strong Day for Most Bourses

Major Asian bourses continued in a positive mood today on hopes that US rate cuts might be forthcoming. With earnings strong thus far markets continue to be bought on dips despite high valuations.

- The NIkkei had a strong day rising +0.58% after yesterday's falls.

- China's bourses were all up with the Hang Seng by +0.59%, CSI 300 +0.55%, Shanghai up +0.70% and Shenzhen up +0.50%.

- The TAIEX in Taiwan is up strongly by +1.05%

- The KOSPI rallied +1.50% after weak CPI brought rate cuts back on the table.

- The FTSE Malay KLCI is up +0.35% and the Jakarta Composite up strongly by +0.96%.

- The Straits Times rose +0.44% and the PSEi in the Philippines just +0.14%.

- The NIFTY 50 is not following regional trends, down -0.45% at the open.

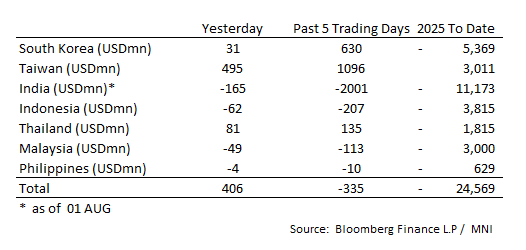

ASIA STOCKS: Big Inflow yesterday for Taiwan as India Sees Outflows

- South Korea: Recorded inflows of +$31m yesterday, bringing the 5-day total to +$630m. 2025 to date flows are -$5,369. The 5-day average is +$126m, the 20-day average is +$191m and the 100-day average of -$10m.

- Taiwan: Had inflows of +$495m yesterday, with total inflows of +$1,096 m over the past 5 days. YTD flows are positive at +$3,011. The 5-day average is +$219m, the 20-day average of +$312m and the 100-day average of +$150m.

- India: Had outflows of -$165m as of the 1st, with total outflows of -$2,001m over the past 5 days. YTD flows are negative -$11,173m. The 5-day average is -$400m, the 20-day average of -$142m and the 100-day average of +$35m.

- Indonesia: Had outflows of -$62m yesterday, with total outflows of -$207m over the prior five days. YTD flows are negative -$3,815m. The 5-day average is -$41m, the 20-day average -$20m and the 100-day average -$31m.

- Thailand: Recorded inflows of +$81m yesterday, with inflows totaling +$135m over the past 5 days. YTD flows are negative at -$1,815m. The 5-day average is +$27m, the 20-day average of +$28m and the 100-day average of -$12m.

- Malaysia: Recorded outflows as of -$49m yesterday, totaling -$113m over the past 5 days. YTD flows are negative at -$3,000m. The 5-day average is -$23m, the 20-day average of -$13m and the 100-day average of -$17m.

- Philippines: Recorded outflows of -$4m yesterday, with net outflows of -$10m over the past 5 days. YTD flows are negative at -$629m. The 5-day average is -$2m, the 20-day average of -$4m the 100-day average of -$4m.

OIL: Crude Stabilizes, Watching Outcome Of US Threats On Russian Oil Purchasers

Oil prices are only slightly lower today after falling over 5% since last Wednesday. WTI is 0.15% lower at $66.19/bbl off its intraday low of $66.02. Brent is down 0.1% to $67.37/bbl after falling to $67.22, trading below the 50-day EMA at $67.95. The USD index is little changed.

- Oil is finding support from the August 8 deadline for Russia and Ukraine to agree on a truce otherwise the US will increase tariffs on not only Russia but also those who purchase its oil. He has been targeting India and PM Modi has responded that India is not going to stop buying Russian fossil fuels. If measures are imposed and are effective in reducing Russian exports, then global supply could be materially impacted as other sources are sought but currently markets see that scenario as unlikely.

- Before Russia’s invasion of Ukraine, India didn’t import oil from there but now around a third comes from Russia driven by its lower prices, according to Bloomberg. China is also a major importer of Russian crude but has not yet been named specifically.

- Assuming uninterrupted Russian oil shipments, global excess supply is widely expected with OPEC ramping up production. Supply indicators will therefore be monitored closely. Later on Tuesday industry-based US inventory data is released.

- Later June US trade, final July S&P Global services/composite PMIs and services ISM print. In Europe, there are July services/composite PMIs and June euro area PPI.

GOLD: Bullion Off Today’s High But Holding Onto Post-Payroll Gains

Gold prices are slightly lower in today’s APAC session after rising sharply following the disappointing US July payrolls data and increased pricing of Fed rate cuts. They peaked at $3382.40/oz before trending lower to $3371.33 and are around $3372.0. The higher US dollar and yields put downward pressure on non-interest bearing bullion.

- Silver is down 0.1% to $37.384 after a high of $37.494. It reached a low of $37.371 earlier.

- Equities have followed the US higher with the Nikkei up 0.6%, Hang Seng +0.3%, KOSPI +1.4% and S&P e-mini +0.1%. Oil prices are lower with WTI -0.2% to $66.16/bbl. Copper is up 0.3%.

- Later June US trade, final July S&P Global services/composite PMIs and services ISM print. In Europe, there are July services/composite PMIs and June euro area PPI.

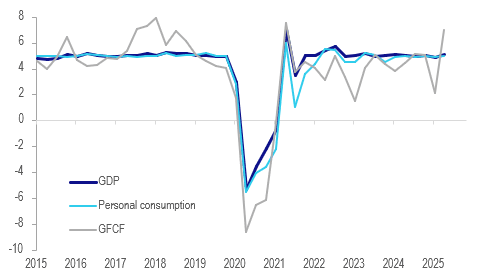

INDONESIA: Q2 GDP Growth Rises, Stronger Than Expected

Q2 Indonesia GDP was stronger than expected rising 5.1% y/y up from 4.9% in Q1 and stronger than Bloomberg consensus at 4.8%. This result was back in line with Q4 after Q1’s dip and was driven by improvements across components. Bank Indonesia cut rates 25bp in July to 5.25% which brought the total easing this cycle to 100bp, which may now be providing some support to growth. Fiscal policy has also been stimulatory.

Indonesia GDP y/y%

- Risks to the growth outlook persist, especially from global factors and their impact on confidence. Indonesia’s government reduced its 2025 growth forecast to 4.7-5% from 5.2%. New fiscal measures are due to be announced on August 15.

- Private consumption growth picked up to 5.0% y/y from 4.9% and was stronger than implied by Q2 consumer confidence but this may weigh on spending in Q3.

- Private investment grew by 7% y/y, the highest in four years and up from Q1’s 2.1%.

- Government spending continued to contract in Q2 but at a slower rate of -0.3% y/y after -1.4%.

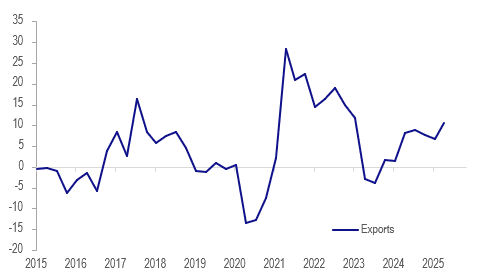

- Exports growth jumped to 10.7% y/y from 6.8% as shipments to the US continued to be frontloaded ahead of the revised early July deadline. Originally a “reciprocal” tariff of 32% was to be imposed on Indonesia but that has been negotiated down to 19%. With exports to the US concentrated in H1, there is likely to be payback in H2.

- USDIDR is little changed today at around 16385 but is still 0.7% higher than it was when BI last met.

Indonesia exports y/y%

Source: MNI - Market News/LSEG

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/08/2025 | 0645/0845 | * | Industrial Production | |

| 05/08/2025 | 0700/0900 | ** | Industrial Production | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 05/08/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/08/2025 | 0900/1100 | ** | PPI | |

| 05/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 05/08/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/08/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/08/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 05/08/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/08/2025 | 2330/0830 | ** | average wages (p) | |

| 06/08/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 06/08/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/08/2025 | 0800/1000 | * | Industrial Production | |

| 06/08/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/08/2025 | 0900/1100 | ** | Retail Sales | |

| 06/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index |